Facts-Analysis: Who Are Largest Berkshire Hathaway Owners? Biggest Institutional Investors? Insights from Chairman Buffett-Other Major Conglomerate Interests in Manufactured Housing; Apple Tease

This report with analysis will take you deeper into facts and finances in the world of Warren Buffett led Berkshire Hathaway. For the detail-oriented industry professional, you should walk away with a better insight into the money trail, methods, thinking and behavior of Buffett. Meaning, this is a proverbial trip into the man’s mind based on corporate and other financial facts, his statements, patterns of behaviors, their investments and insights from others. According to the annual Berkshire Hathaway (BRK) letter by Warren Buffett on Feb 24, 2024 — “Berkshire has more than three million shareholder accounts.” While that may be true, much of Berkshire is owned by insiders and institutional investors. Some of the most significant companies in their respective area of operation in manufactured housing are owned by Berkshire Hathway. So, it is perhaps no surprise that those firms like Clayton Homes, 21st Mortgage Corporation, Vanderbilt Mortgage and Finance (VMF) have long held sway – along with others of similar orientation – at the Manufactured Housing Institute (MHI) for about two decades. Investopedia noted that at the time of the Buffett annual letter that the “The top three individual shareholders [at BRK] are Warren Buffett, Susan Buffett, and Ronald Olson” and that “The company’s [i.e.: BRK] top three institutional shareholders are Vanguard, BlackRock, and State Street.” Before diving deeper into the details behind who owns Berkshire, some thoughts from Chairman Buffett are warranted (sorry, a play on his first name). More on Olson and MHVille at this link here.

What Part IV of this report will provide are insights from Berkshire that are generally ignored or are overlooked by others in MHVille trade media beyond MHProNews and ourMHLivingNews sister site.

To understand Berkshire, one certainly must understand “the moat.”

But there is more, much more, because the patient and long-term thinkers will draw keen and useful insights from the mind and worldview of Buffett. That is arguably true even if someone disagrees with Buffett’s worldview, ethics, politics, and purportedly dubious business practices. Meaning, you don’t have to agree with Buffett to learn how his mind and methods seem to work. This interlaced deeper dive could help your understanding of why he and others do what they do. It is arguably also an insight into the current state of new manufactured housing production and performance. Career and investment benefits could follow for focused, fact-driven, analytical thinkers.

To even better grasp what Berkshire considers significant are facts found in Part III of this report, which are straight from the data published by Berkshire Hathaway. The tease related to Apple will also appear there.

Buffett fans, Buffett foes, Buffett team members, Buffett’s allies and critics are accurately quoted. While this information is driven by facts and evidence, as a news analysis, it is also involving expert opinions by MHProNews and others.

Part I

Per Warren Buffett’s annual letter, linked here, are the following thoughts by Chairman Buffett. Readers are advised to keep in mind the analysis of Michael Lebowitz, plus and the statements made by Barrons, among others.

“Berkshire has more than three million shareholder accounts. I am charged with writing a letter every year that will be useful to this diverse and ever-changing group of owners, many of whom wish to learn more about their investment.

Charlie Munger, for decades my partner in managing Berkshire, viewed this obligation identically and would expect me to communicate with you this year in the regular manner. He and I were of one mind regarding our responsibilities to Berkshire shareholders.”

In part of Buffett’s reflection on his late, over half-century partnership with Charlie Munger, J.D., Buffett said: “Berkshire has become a great company. Though I have long been in charge of the construction crew; Charlie should forever be credited with being the architect.”

“In what I next relate, bear in mind that Charlie and his family did not have a dime invested in the small investing partnership that I was then managing and whose money I had used for the Berkshire purchase. Moreover, neither of us expected that Charlie would ever own a share of Berkshire stock.

Nevertheless, Charlie, in 1965, promptly advised me: “Warren, forget about ever buying another company like Berkshire. But now that you control Berkshire, add to it wonderful businesses purchased at fair prices and give up buying fair businesses at wonderful prices. In other words, abandon everything you learned from your hero, Ben Graham. It works but only when practiced at small scale.” With much back-sliding I subsequently followed his instructions.”

Also from his 2023 annual letter: “Our goal at Berkshire is simple: We want to own either all or a portion of businesses that enjoy good economics that are fundamental and enduring. Within capitalism, some businesses will flourish for a very long time while others will prove to be sinkholes. It’s harder than you would think to predict which will be the winners and losers. And those who tell you they know the answer are usually either self-delusional or snake-oil salesmen. ”

In 1863, Hugh McCulloch, the first Comptroller of the United States, sent a letter to all national banks. His instructions included this warning: “Never deal with a rascal under the expectation that you can prevent him from cheating you.” Many bankers who thought they could “manage” the rascal problem have learned the wisdom of Mr. McCulloch’s advice – and I have as well. People are not that easy to read. Sincerity and empathy can easily be faked. That is as true now as it was in 1863.”

Some more pull Buffett letter quotes:

For whatever reasons, markets now exhibit far more casino-like behavior than they did when I was young.

One fact of financial life should never be forgotten. Wall Street – to use the term in its

figurative sense – would like its customers to make money, but what truly causes its denizens’

juices to flow is feverish activity. At such times, whatever foolishness can be marketed will be

vigorously marketed – not by everyone but always by someone.

Occasionally, the scene turns ugly. The politicians then become enraged; the most flagrant

perpetrators of misdeeds slip away, rich and unpunished; and your friend next door becomes

bewildered, poorer and sometimes vengeful. Money, he learns, has trumped morality.

Your company also holds a cash and U.S. Treasury bill position far in excess of what

conventional wisdom deems necessary. During the 2008 panic, Berkshire generated cash from

operations and did not rely in any manner on commercial paper, bank lines or debt markets. We

did not predict the time of an economic paralysis but we were always prepared for one.

The lesson from Coke and AMEX? When you find a truly wonderful business, stick with

it. Patience pays, and one wonderful business can offset the many mediocre decisions that

are inevitable. …

At yearend, Berkshire owned 27.8% of Occidental Petroleum’s common shares and also

owned warrants that, for more than five years, give us the option to materially increase our

ownership at a fixed price. Though we very much like our ownership, as well as the option,

Berkshire has no interest in purchasing or managing Occidental. We particularly like its vast oil

and gas holdings in the United States, as well as its leadership in carbon-capture initiatives, though

the economic feasibility of this technique has yet to be proven. Both of these activities are very

much in our country’s interest. …

And then – Hallelujah! – shale economics became feasible in 2011, and our energy

dependency ended. Now, U.S. production is more than 13 million BOEPD, and OPEC no longer

has the upper hand. Occidental itself has annual U.S. oil production that each year comes close to

matching the entire inventory of the SPR. Our country would be very – very – nervous today if

domestic production had remained at five million BOEPD, and it found itself hugely dependent

on non-U.S. sources. At that level, the SPR would have been emptied within months if foreign oil

became unavailable.

Part II

According to Yahoo Finance on 8.1.2024 is the following information as of about 12:03 PM ET.

652,774.00-6,437.00 (-0.98%)

As of 12:03 PM EDT.

Major Holders

Breakdown

37.50%

% of Shares Held by All Insiders

18.25%

% of Shares Held by Institutions

29.19%

% of Float Held by Institutions

1,184

Number of Institutions Holding Shares

Top Institutional Holders

Holder

Shares

Date Reported

% Out

Value

FMR, LLC

33.43k

Mar 31, 2024

5.94%

21,819,245,336

First Manhattan Company

15.31k

Mar 31, 2024

2.72%

9,994,504,146

Corient Private Wealth LLC

13.55k

Mar 31, 2024

2.41%

8,844,405,118

Cidel Asset Management, Inc.

9.77k

Jun 30, 2024

1.74%

6,376,457,092

Vista Capital Partners, Inc.

5.53k

Mar 31, 2024

0.98%

3,608,256,199

Norges Bank Investment Management

5.29k

Dec 31, 2023

0.94%

3,451,602,529

Gardner Russo & Quinn, LLC

2.13k

Mar 31, 2024

0.38%

1,391,606,768

Pflug Koory, LLC

1.9k

Mar 31, 2024

0.34%

1,240,174,887

HighTower Advisors, LLC

1.89k

Mar 31, 2024

0.34%

1,232,342,204

Davis Selected Advisers, LP

1.85k

Mar 31, 2024

0.33%

1,206,233,2

Top Mutual Fund Holders

Holder

Shares

Date Reported

% Out

Value

Fidelity Contrafund Inc

18.76k

May 31, 2024

3.34%

12,247,706,099

Fidelity Contrafund K6 Fund

3.94k

May 31, 2024

0.70%

2,570,425,635

Fidelity Advisor New Insights Fund

1.59k

May 31, 2024

0.28%

1,035,219,669

Vanguard Total Stock Market Index Fund

1.05k

Mar 31, 2024

0.19%

686,012,529

Fidelity Series Opportunistic Insights Fund

1k

May 31, 2024

0.18%

655,334,519

SRH Total Return Fund, Inc.

1.03k

May 31, 2024

0.18%

670,999,886

Davis New York Venture Fund

895

Apr 30, 2024

0.16%

584,187,644

First Eagle Global Fund

675

Apr 30, 2024

0.12%

440,588,446

Legg Mason Clearbridge Appreciation Fd

504

Apr 30, 2024

0.09%

328,972,707

Tweedy Browne Global Value Fund

418

Mar 31, 2024

0.07%

272,838,475

Also per Yahoo Finance is the following. The yellow highlighting below is added by MHProNews.

NYSE – Nasdaq Real Time Price•USD

Berkshire Hathaway Inc. (BRK-B)

435.59-2.91(-0.66%)

As of 12:07 PM EDT. Market Open.

Major Holders

Breakdown

0.39%

% of Shares Held by All Insider

65.96%

% of Shares Held by Institutions

66.22%

% of Float Held by Institutions

4,786

Number of Institutions Holding Shares

Top Institutional Holders

Holder

Shares

Date Reported

% Out

Value

Vanguard Group Inc.

146.55M

Mar 31, 2024

11.18%

63,837,065,599

Blackrock Inc.

107.51M

Mar 31, 2024

8.20%

46,829,082,198

State Street Corporation

69.51M

Mar 31, 2024

5.30%

30,279,514,145

Geode Capital Management, LLC

35.33M

Mar 31, 2024

2.69%

15,387,575,546

Morgan Stanley

24.32M

Mar 31, 2024

1.85%

10,591,515,812

Bill & Melinda Gates Foundation Trust

17.3M

Mar 31, 2024

1.32%

7,537,055,958

Northern Trust Corporation

15.71M

Mar 31, 2024

1.20%

6,844,696,113

Bank Of New York Mellon Corporation

12.79M

Jun 30, 2024

0.98%

5,569,750,329

Norges Bank Investment Management

11.48M

Dec 31, 2023

0.88%

5,001,903,885

Price (T.Rowe) Associates Inc

10.81M

Mar 31, 2024

0.82%

4,709,325,489

Top Mutual Fund Holders

Holder

Shares

Date Reported

% Out

Value

Vanguard Total Stock Market Index Fund

55.74M

Mar 31, 2024

4.25%

24,281,247,800

Vanguard 500 Index Fund

45.85M

Mar 31, 2024

3.50%

19,972,387,636

Fidelity 500 Index Fund

22.15M

May 31, 2024

1.69%

9,647,807,471

SPDR S&P 500 ETF Trust

21.56M

Jun 30, 2024

1.64%

9,391,528,968

iShares Core S&P 500 ETF

19.32M

Jun 30, 2024

1.47%

8,416,082,234

Vanguard Index-Value Index Fund

15.1M

Mar 31, 2024

1.15%

6,578,729,653

Select Sector SPDR Fund-Financial

12.35M

Jun 30, 2024

0.94%

5,378,531,548

Vanguard Institutional Index Fund-Institutional Index Fund

11.96M

Mar 31, 2024

0.91%

5,211,717,132

iShares Russell 1000 Value ETF

4.39M

Jun 30, 2024

0.33%

1,913,031,550

Schwab Capital Trust-Schwab S&P 500 Index Fund

3.79M

Apr 30, 2024

0.29%

1,650,668,291

Part III About Clayton Homes From K-16 of Berkshire Annual Report and Beyond Clayton, Forest River Recreational Vehicles (RVs), Berkshire Hathaway’s HomeServices

1)

Building Products

Clayton

Clayton Homes, Inc. (“Clayton”), headquartered near Knoxville, Tennessee, is a vertically integrated housing company offering traditional site-built homes and off-site (factory) built housing, including modular, manufactured, CrossMod™ and tiny homes. In 2023, Clayton delivered approximately 43,000 off-site built and approximately 10,000 site-built homes. Clayton also offers home financing and other financial services and competes on price, service, location and delivery capabilities.

All Clayton Built® off-site built homes are designed, engineered and assembled in the U.S. As of December 2023, offsite backlog was $799 million, up over 200% from the prior year end. Clayton sells off-site built homes through independent and company-owned home centers, realtors and subdivision channels. Clayton considers its ability to offer financing to retail purchasers a factor affecting the marketplace acceptance of its off-site built homes. Clayton’s financing programs utilize proprietary loan underwriting guidelines to evaluate loan applicants.

Since 2015, Clayton’s site-built division, Clayton Properties Group, has expanded through the acquisition of nine builders across 18 states with over 290 subdivisions, supplementing the portfolio of housing products offered to customers. Clayton’s site-builders currently own and control approximately 67,000 homesites, with a home order backlog of approximately $1.6 billion as of December 2023.

Historically, access to key housing inputs such as lumber, steel and resin products has been adequate. During 2021 and the first half of 2022, the availability and pricing of these and other inputs was volatile. Input shortages coupled with reduced labor and subcontractor availability increased the time needed to construct a home, increasing the levels of work-in-process inventory. These constraints began to lessen in the latter half of 2022 due to improved availability and pricing of key inputs, increased order cancellations and lower overall demand for new home construction.

Clayton’s building products business benefited in recent years from the low interest rate environment and the strong residential construction market. However, the effects of significant increases in home mortgage interest rates in the U.S. over the past year has slowed demand for new home construction, partially mitigated by low supplies of pre-existing homes for sale. Clayton’s home building business regularly makes capital and non-capital expenditures with respect to compliance with federal, state and local environmental regulations, primarily related to erosion control, permitting and stormwater protection for site-built home subdivisions. The financing business originates and services loans which are federally regulated by the Consumer Financial Protection Bureau, various state regulatory agencies and reviewed by the U.S. Department of Housing and Urban Development, the Government National Mortgage Association and government-sponsored enterprises.”

Forest River, Inc. (“Forest River”), headquartered in Elkhart, Indiana, is a manufacturer of recreational vehicles (“RV”), utility cargo trailers, buses and pontoon boats with products sold in the U.S. and Canada through an independent dealer network. Forest River has numerous manufacturing facilities located in six states and is a leading manufacturer of RVs with numerous brand names, including Forest River, Coachmen RV and Prime Time. Utility cargo trailers are sold under a variety of brand names. Buses are sold under several brand names, including Starcraft Bus. Pontoon boats are sold under the Berkshire, South Bay and Trifecta brand names.

The RV industry is highly competitive. Competition is based primarily on price, design, quality and service. The industry has consolidated over the past several years and is currently concentrated in a few companies, the largest of which had a market share of approximately 42% based on industry data as of September 2023. Forest River held a market share of approximately 33% at that time. Forest River is subject to regulations of the National Traffic and Motor Vehicle Safety Act, the safety standards for recreational vehicles established by the U.S. Department of Transportation and similar laws and regulations issued by the Canadian government. Forest River is a member of the Recreational Vehicle Industry Association, a voluntary association of RV manufacturers which promotes safety standards for RVs. Forest River believes its products comply in all material respects with the standards that govern its products.

MiTek Industries, Inc. (“MiTek”), based in Chesterfield, Missouri, operates in two separate building markets: residential and commercial. MiTek operates worldwide with sales in over 60 countries and with manufacturing facilities and/or sales/engineering offices located in 20 countries.

In the residential building market, MiTek is a leading supplier of engineered connector products, construction hardware, engineering software and services, and computer-driven manufacturing machinery to the truss component market of the building components industry. MiTek’s primary customers are component manufacturers who manufacture prefabricated roof and floor trusses and wall panels for the residential building market. MiTek also sells construction hardware to commercial distributors and retail stores for do-it-yourself customers.

A significant raw material used by MiTek is hot dipped galvanized sheet steel. While supplies are presently adequate, variations in supply have historically occurred, producing significant variations in cost and availability.

According to page K149 Mitek employed 5,783 employees as of the reporting date.

HomeServices of America, Inc. (“HomeServices”) is a residential real estate brokerage firm in the U.S. In addition to providing traditional residential real estate brokerage services, HomeServices offers other integrated real estate services, including mortgage originations and mortgage banking, title and closing services, insurance, home warranties, relocation services and other home-related services. It operates under 50 brand names with approximately 41,000 real estate agents in nearly 900 brokerage offices in 34 states and the District of Columbia.

HomeServices’ franchise network currently includes approximately 300 franchisees and over 1,500 brokerage offices with nearly 48,000 real estate agents under two brand names, primarily in the U.S. In exchange for certain fees, HomeServices provides the right to use the Berkshire Hathaway HomeServices or Real Living brand names and other related service marks, as well as providing orientation programs, training and consultation services, advertising programs and other services.

HomeServices’ principal sources of revenue are dependent on residential real estate transaction volumes, which are generally higher in the second and third quarters of each year. This business is highly competitive and subject to general real estate market conditions.

Per page K149 HomeServices of America has 5,803 employees.

According to Barron’s: “Transaction volumes tanked as many brokers couldn’t close deals for months. HomeServices is not immune. According to Berkshire, the revenue from its real-estate business fell 30% from $6.2 billion in 2021 to $4.3 billion in 2023.”

Per the HomeServices website on 8.1.2024.

Headquartered in Minneapolis MN, HomeServices of America, a Berkshire Hathaway affiliate, is, through its operating companies, one of the country’s premier providers of homeownership services, including brokerage, mortgage, franchising, title, escrow, insurance, and relocation services.

ABOUT BERKSHIRE HATHAWAY HOMESERVICES

…With approximately 50,000 real estate professionals and more than 1,500 offices across 4 continents and 13 countries and territories including the U.S., Canada, Mexico, Europe, the Middle East, The Caribbean and India, the network completed more than USD$126.9 billion in real estate sales in 2023. Among the few organizations entrusted to use the world-renowned Berkshire Hathaway name, the network brings to the real estate market a definitive mark of trust, integrity, stability and longevity.”

Prosperity Home Mortgage Recognized for Overall Customer Satisfaction by J.D. Power

Fairfax, Virginia (January 24, 2024) — Prosperity Home Mortgage, LLC (“Prosperity”), one of the nation’s leading full-service mortgage bankers specializing in residential and refinance loans…”

Beyond the above, Berkshire has interests in Acme Brick, Shaw, John Manville, and numerous other firms.

Part IV – Additional Information with More MHProNews Analysis and Commentary

In journalism, a tease can have multiple meanings. Among them is a promise of something that is upcoming. To keep this already information packed article manageable, there will be a planned follow up report with analysis on the development at Berkshire Hathaway (BRK) about their sale of a large percentage of Apple stocks. But for now, it is useful to keep in mind this flashback report.

Why? Because like him or not, Buffett in his later years has a reputation for normally not doing something without deliberation. Buffett got involved with Apple as an investment for specific reasons, and it apparently paid.

1) More recently, his sale of shares in 2024 may prove to be a signal, perhaps on multiple levels. Per the Guardian on August 3, 2024 is the following snippet to support the tease.

Berkshire sold about 390m Apple shares in the second quarter, on top of 115m shares from January to March, as Apple’s stock price rose 23%. It still owned about 400m shares worth $84.2bn as of 30 June.

That’s a big move. According to Live Mint on 8.16.2024 is the following.

As a result of the Apple sale, Berkshire Hathaway’s cash and cash equivalents surged by $88 billion, reaching a record high of $277 billion in Q2 2024.

Again, more is planned on this Apple move and its possible implications in a follow up report that may include antitrust aspects to the situation.

But for now, to illustrate how much cash and cash equivalents Berkshire now has, consider the following valuations of well-known companies in manufactured housing and what their valuations were as of the close of the markets on Friday 8.23.2024, per Yahoo Finance.

Equity LifeStyle Properties (ELS)

13.764B

Sun Communities (SUI)

17.244B

Cavco Industries (CVCO)

3.377B

Skyline Champion (SKY)

5.327B

That’s a total of about $39.712 billion dollars combined valuations at that time for those four firms. So, the value of what Buffett led Berkshire sold in Apple stock (about $88 billion) is more than double the value of 4 of the largest firms in the manufactured housing industry.

2) For objective analysts that want to better understand the dynamics at play in manufactured housing, among the takeaways from Part III should be this. When comparing Clayton Homes and their related lending, 21st Mortgage Corporation and Vanderbilt Mortgage and Finance (VMF), they are relatively modest compared to BRK’s conventional housing interests. Additionally, the RV business is important to Berkshire.

That noted, let’s briefly focus a bit more on HomeServices, which reportedly “the network completed more than USD$126.9 billion in real estate sales in 2023.” According to BRK-B.com:

Clayton Homes has demonstrated remarkable financial performance in the first quarter of 2024, showcasing its robust financial health and strategic prowess. The company’s revenues increased by 9.1% to $2.7 billion in Q1 2024 compared to the same period in 2023 1.

Meaning, the conventional housing business interests of Berkshire Hathaway dwarfs what Clayton Homes produces. Furthermore, the site-built housing interests of Clayton Homes has also grown. Toss in Mitek, and it becomes clear that while Berkshire owns Clayton, and Clayton has long held a powerful influence over the Manufactured Housing Institute and the diminished MHVille market more broadly, and it becomes clear that Clayton’s manufactured housing interests take a proverbial back seat to conventional housing.

If Buffett thought manufactured homes would hurt his conventional housing interests, which is he going to pick?

It was noted in Part I that institutional investors have a serious stake in Berkshire. As MHProNews previously reported, some of those same institutional investors have a notable stakes in other manufactured home industry companies.

While it won’t be the focus of this report, it should be noted that those same institutional investors also have interests in conventional housing.

Among the possible implications? Manufactured homes may well produce some profits for Berkshire and others. But it can also be seen as a kind of defensive move. Throttling manufactured housing growth, for example, could be seen as shrewd by Buffett and others like him in those rarified air orbit of giants that have combined assets under management that rival the gross domestic product of the United States of America (USA).

3) To further illustrate that point #2 above, consider this. Buffett and Berkshire have said that they want to make money from each of their business interests. But Buffett has admitted that in certain situations, they are willing to sacrifice profits for the sake of a bigger picture.

“Lose money for the firm, and I will be understanding. Lose a shred of reputation for the firm, and I will be ruthless.”

4) Buffett is not beyond evidence-based criticism. Investopedia has a post Updated September 21, 2023. By posting this, or other items, should not be construed as endorsing every aspect of what follows. The observations are those of the publication and its writer/editor(s).

Warren Buffett Controversies That Have Threatened His Reputation

Even the beloved Oracle of Omaha isn’t beyond criticism

Stephen Simpson, CFA, has 15+ years of experience in financial publishing and editing. He is the operator of the Kratisto Investing blog.

Buffalo Evening News

Buffett found himself the target of antitrust charges when he acquired the Buffalo Evening News for a reported $33 million in 1977, again through Blue Chip Stamps.23

Buffett and the Buffalo Evening News prevailed in the legal proceedings. Moreover, the antitrust action seemed to some observers a desperate attempt by the rival Buffalo Courier-Express to use the courts to take out its competition.

It was a stressful time all around, and Buffett was accused of failing to respect prior gentlemen’s agreements.

Berkshire Hathaway ultimately sold the Buffalo paper and 30 others it owned to Lee Enterprises in 2020.4

The Middle Period

Salomon Brothers

One of the most serious controversies involving Warren Buffett occurred in 1990. In 1987, Berkshire Hathaway had acquired a 12% interest in the investment banking firm of Salomon Brothers.

In 1990, the news came out that a rogue trader had submitted bids in excess of Treasury rules and CEO John Gutfreund had failed to take disciplinary action.

The U.S. government threatened to hold Salomon accountable. Buffett stepped into the breach. He directly intervened with the U.S. Treasury to reverse a ban on Salomon bidding in government bond auctions. Such a ban would have crippled the investment bank.

Buffett also stepped in to run Salomon Brothers for a time. Despite a $290 million fine levied on Salomon in 1992, Berkshire Hathaway ultimately saw its stake more than double when Travelers Group bought Salomon in 1997.5

Berkshire Hathaway’s Charitable Giving

Berkshire Hathaway has experienced controversy due to its former charitable giving practices. Buffett believed that it was inappropriate for a company to direct its charitable giving to the pet causes of the board of directors.

Instead, he decided that shareholders of the company could allocate their proportionate share of the company’s giving to the charitable organizations that they deemed worthy. Some shareholders elected to contribute to various pro-choice organizations.

This inflamed some conservatives who, in turn, organized negative public relations campaigns and boycotts against certain Berkshire Hathaway businesses. Most notable of these was The Pampered Chef, which relied on a direct sales business model akin to Avon.

In response to the controversy, Buffett ended Berkshire Hathaway’s shareholder-designated contributions program.6

Buffett expressed a view of controversial behavior in a 1991 congressional hearing concerning troubled investment banking firm Solomon Brothers, in which Berkshire Hathaway was invested. Buffett said “Lose money for the firm, and I will be understanding. Lose a shred of reputation for the firm, and I will be ruthless.”7

More Recent Controversies

General Re

The charges in 2006 against Berkshire Hathaway subsidiary General Reinsurance Corporation, or General Re, were serious. It was claimed that General Re cooperated with insurance giant AIG to engage in finite reinsurance.

Finite reinsurance was not insurance per se (with a corresponding transfer of risk). It was more of an accounting gimmick that allowed a company such as AIG to buff the appearance of its financial reports for a period of time.

The government aggressively pursued AIG and its then-chair, Hank Greenberg. Berkshire Hathaway did not escape unscathed. General Re agreed to pay $60.5 million through a civil class action settlement to AIG shareholders, $19.5 million to the U.S. Postal Inspection Service Consumer Fraud Fund, and another $12.2 million to settle the SEC charges.8

Goldman Sachs

Berkshire Hathaway invested $5 billion in Goldman Sachs preferred stock during the 2008 financial crisis.9

Buffett believed that the stock purchase not only signaled confidence in the country’s financial institutions but demonstrated that the U.S. business community would take crucial action when the U.S. government wouldn’t.9

When the investment bank redeemed those shares in 2011, Berkshire made $3.7 billion.9

However, Buffett’s association with Goldman Sachs—a company famously described by the writer Matt Taibbi as “a great vampire squid wrapped around the face of humanity, relentlessly jamming its blood funnel into anything that smells like money”10—did his reputation no favors.

Wells Fargo

This episode is more a cautionary tale than it is a threatening controversy, occurring as it did while Berkshire Hathaway held a major portion of Wells Fargo shares.

In 1989, Berkshire Hathaway began investing in Wells Fargo, spending $12.7 billion and capturing a 10% stake.11 Buffett considered the bank one of his favorite holdings. However, in 2016 Wells Fargo was fined $185 million for illegal business practices. These centered on the bank’s intense drive to cross-sell products and services to customers.

In fact, bank employees had opened millions of accounts fraudulently, charged customers for products and services they never requested, charged other inappropriate fees, and more.12 At first Wells Fargo ignored the unsavory revelations, a move that Buffett condemned.11 The bank paid $3 billion in 2020 to settle various civil and criminal investigations.

As a result of Wells Fargo’s unethical behavior, Berkshire Hathaway had sold almost all of its shares by 2021 and the rest in 2022.13 As of 2023, the bank is still trying to repair its self-inflicted damage.14

A Too-Cozy Board?

One ongoing controversy involves corporate governance and the independence of the board of directors of Berkshire Hathaway. It’s difficult to call it an independent board because many of its members are long-standing friends of Warren Buffett, Charlie Munger, or both men.

Buffett is the majority owner of the company. He wants directors with whom he is comfortable and who have the patient investment outlook that has served him so well for decades. Nevertheless, it does not change the fact that as a public company, Berkshire Hathaway is obligated to shareholders to have a strong, independent board of directors. …”

5) Much of that in #4 is akin to what was previously reported by MHProNews in the articles linked below. A case can be made that the above supports what follows, and what follows supports the above.

6) MHProNews has been reporting on Buffett and the distinction between his words and his deeds numerous times. To say that Buffett has critics is an understatement. But most people do. So what?

What is far more relevant is the answer to this question: are the criticism warranted?

That is what MHProNews has kept in focus, as has our MHLivingNews sister site.

Before proceeding, consider some of Buffett, his later partner Charlie Munger’s, and his fellow investor and strategic ally William “Bill” Gates III’s own statements. Just a few quotes can help paint a picture.

Let’s pause for a moment. Warfare by definition is not pleasant. Per Oxford Languages, warfare means engagement in, or the activities involved, in war or conflict. Collins Dictionary clarifies that definition: “Warfare is sometimes used to refer to any violent struggle or conflict.” Violent. Struggle. Conflict. Buffett said he and his “class” are involved in “warfare.” If you are a competitor of Buffett or one of his brands, expect to be in conflict. Who says? How about Buffett’s CEO of Clayton Homes, Kevin Clayton?

7) Next comes a bit of the ‘folksiness’ of Buffett on display by Kevin Clayton, who was supposedly auditioning to replace him some day at the helm of Berkshire. Give Kevin credit, in this video, he seems to emulate that Buffett aura of a friendly, affable fellow, with no hint of the sinister nature of what “the Moat” represents. Keep in mind that Buffett spoke of class warfare. Then recall that Buffett’s description of the moat included man-eating amphibians – sharks and piranhas and crocodiles. Buffett has also used the example of sharks and allegators. Picture Perfect Portfolios said this:

Buffett underscores the value of a strong, defensible competitive position in business—a metaphorical castle safeguarded by a formidable moat filled with deterrents to competitors. “A good business is like a strong castle with a deep moat around it. I want sharks in the moat to keep away those who would encroach on the castle.”

According to AcquirersMultiple.com, which insightful tees up a quote from a Buffett annual letter on “widening the moat.”

In his 2005 Berkshire Hathaway Annual Letter, Warren Buffett discussed the importance of focusing on long-term sustainability and competitive advantage over short-term gains, highlighting the concept of “widening the moat” as a key strategy for business success. Here’s an excerpt from the letter:

Every day, in countless ways, the competitive position of each of our businesses grows either weaker or stronger. If we are delighting customers, eliminating unnecessary costs and improving our products and services, we gain strength.

But if we treat customers with indifference or tolerate bloat, our businesses will wither. On a daily basis, the effects of our actions are imperceptible; cumulatively, though, their consequences are enormous.

When our long-term competitive position improves as a result of these almost unnoticeable actions, we describe the phenomenon as “widening the moat.” And doing that is essential if we are to have the kind of business we want a decade or two from now. We always, of course, hope to earn more money in the short-term.

But when short-term and long-term conflict, widening the moat must take precedence. If a management makes bad decisions in order to hit short-term earnings targets, and consequently gets behind the eight-ball in terms of costs, customer satisfaction or brand strength, no amount of subsequent brilliance will overcome the damage that has been inflicted.

Take a look at the dilemmas of managers in the auto and airline industries today as they struggle with the huge problems handed them by their predecessors. Charlie is fond of quoting Ben Franklin’s “An ounce of prevention is worth a pound of cure.” But sometimes no amount of cure will overcome the mistakes of the past.

Our managers focus on moat-widening – and are brilliant at it. Quite simply, they are passionate about their businesses. Usually, they were running those long before we came along; our only function since has been to stay out of the way. If you see these heroes – and our four heroines as well – at the annual meeting, thank them for the job they do for you.

With those insights by Buffett about the Moat, or the Castle and Moat, now let’s look again at what Kevin Clayton told Robert Miles in the perhaps too revealing video interview. …Of course, Warren [Buffett] looks for companies that have that enduring competitive advantage. That’s part of our moat, and we intend to deepen and widen that part of our moat… Warren likes to say that there’s two kinds of competition that he doesn’t like, foreign and domestic.

Warren’s very competitive. It’s just amazing, his personality, to be such a genius…he paints such an image in each of our manager’s minds about this moat, this competitive moat, and our job is very simple, and we share this. It’s so fun sharing some of the things that he [Warren] passes along through our organization., and we challenge everyone of our team members, every department. Who is your customer? Deepen and widen your moat to keep out the competition…

But some of our competitors do a good job, but our plans are to make that difficult for them…”

9) “Difficult” is relatively soft language, but Clayton himself told Congress that thousands of independent firms failed since 2005. Keep in mind, Buffett led Berkshire directly entered the manufactured home industry in 2002-2003. He did so after dumping shares in Fannie Mae and Freddie Mac in 2000.

10) Next, keep in mind that Buffett has cultivated a folksy, seemingly jovial manner. That seemingly casual and likeable manner is an apparent tactic used to disarm people and put them at ease with him. Buffett is also projected to be a ‘philanthropist.’ But when someone looks at that philanthropy, that has been criticized by Warren’s own son Peter as being misleading, because those charities don’t tend to move the needle on poverty. “Someone is further locked into a system that will not allow the true flourishing of his or her nature or the opportunity to live a joyful and fulfilled life.” That’s Peter Buffett speaking, Buffett’s son in charge of the left-leaning and Buffett-funded Novo Foundation.

The Institute for Policy Studies (IPS), a left-leaning nonprofit, spotlighted on their website the report by MHLivingNews, which apparently the thought was quality and accurate or they would not have elevated it in that fashion for their audience.

Clayton spoke about charitable giving too. It is part of the apparent ‘cover’ that makes Buffett (and his top management) seem nice and folks, even if they are wolves in sheep’s clothing. Or, as the murdered Malcom X said, a sly fox.

11) It has to be stressed that Buffett is a reader. He thinks. He analyses. He is into history, including the dry-to-some details of corporate and business (industry) histories.

Not long after what is now called MHProNews originally launched approaching 15 years ago, this platform encouraged readers to invest ten to fifteen minutes a day in reading. Fast forward to 2024, and there is evidence that thousands of readers may be spending 30 minutes to an hour or more reading reports and analysis on MHProNews daily. To be able to compete successfully with Buffett and those who follow his moat and other tactics, it is just common sense that the more you know, the better you understand and the more likely you can establish plans that can successfully navigate the threats that are apparently posed by Buffett, his brands, and their allies.

Our regular and longer-term visitors are readers too. We deliver on what our headlines say, and routinely deliver far more than what the headline may say. As Copilot has said several times, our reports on MHProNews and MHLivingNews are factually accurate, based on solid evidence, use clearly cited sources, and our analysis is based on common sense (logic, sound reasoning, etc.). See the recent analysis by Copilot of our reporting at this link here.

The above quotation is huge. As a tip of the hat to our readers/visitors/audience, it should be noted that MHProNews evolved from very short USA Today style one to a few paragraph news articles a decade or ago to ever longer news with analysis articles. This article may require 20 to 30 minutes for someone to read it thoughtfully. Numbers of visitors here, per site data, are spending perhaps an hour or more a day reading MHProNews. That’s still peanuts compared to what Buffett invests in reading time, which is reportedly 5 to 6 hours daily. For years, besides the Buffett quotes on reading, MHProNews has featured the following quote from popular, author, speaker, and consultant Matthew Kelly. “Superficiality is the curse of the modern world.” Buffett doesn’t appear to be superficial in his study. Neither should anyone be superficial who hopes to successfully challenge he or his business interests.

12) Let’s pause and sum up some useful takeaways to this point. Buffett is willing to spend money, ‘give it away,’ and lose money for the right motivations. But his stated goals are to make more money and gain more power. He said so, with he and Charlie Munger on camera with left-leaning CNBC nodding in agreement.

Buffett has described business and America in terms of warfare. Buffett’s class is making war on the rest of America. It isn’t just Buffett who said so.

Remember? Citigroup Plutonomy Memos: Two bombshell memos describing in detail the rule of the first 1% https://t.co/PV01veMmrK

That leaked Citigroup memo is found here. Some pull quotes.

The World is dividing into two blocs – the Plutonomy and the rest. The U.S., UK, and Canada are the key Plutonomies – economies powered by the wealthy.

WELCOME TO THE PLUTONOMY MACHINE

In early September we wrote about the (ir)relevance of oil to equities and introduced the

idea that the U.S.is a Plutonomy

We will posit that: 1) the world is dividing into two blocs – the plutonomies, where economic growth is powered

by and largely consumed by the wealthy few, and the rest. Plutonomies have occurred

before in sixteenth century Spain, in seventeenth century Holland, the Gilded Age and

the Roaring Twenties in the U.S.

2) We project that the plutonomies (the U.S., UK, and Canada) will likely see even more

income inequality, disproportionately feeding off a further rise in the profit share in their

economies, capitalist-friendly governments, more technology-driven productivity, and

globalization.

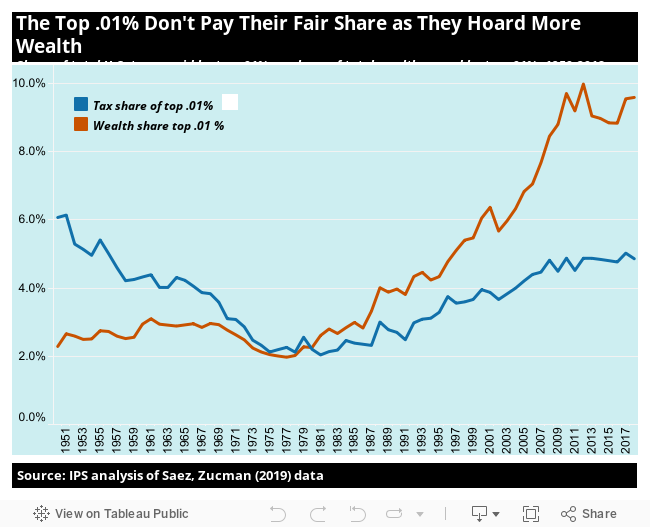

According to Inequality, a site from the left-leaning Institute for Policy Studies (IPS), that point #2 proved largely true.

But something else is notable. During the Trump (R) years, the collective wealth of the 99 percent rose as the wealth of the 1 percent dipped.

It is following the Biden-Harris (D) term of office that the wealth of the uber elites skyrocketed. Quoting.

In 2020, only one U.S. billionaire — Amazon founder Jeff Bezos — had a net worth of $100 billion or more. Today, the entire top 10 are centi-billionaires, bringing their collective wealth to a staggering $1.4 trillion. Overall, the combined wealth of America’s billionaires has grown by 88 percent over the past four years to $5.529 trillion, according to Institute for Policy Studies calculations of Forbes Real Time Billionaire Data.

Then recall this from his longtime buddy and ally, William “Bill” Gates III.

While Buffett is not mentioned by name in George Carlin’s satirical hit video posted below gives several examples of how the ‘game is rigged’ for the insiders and against everyone else. There is a club, said Carlin, and you and I aren’t in it.

Carlin is more from the political left, and while she is not American, some might think of Hanne Nabintu Herland as more of a centrist or from the right. From her perch in Norway, by way of South Africa, Herland has pointed out how billionaires like Buffett and Gates, among others, have manipulated the system in a way that makes them oddly allies of socialism/Marxism/communism/fascism/authoritarianism.

13) Much of this might be construed as making Buffett seem bulletproof or invincible. That is not the informed editorial view of MHProNews. There is years of evidence-based reports that Clayton, 21st, VMF, attorney and board member Ron Olson at Berkshire, and MHI – their board members, president, CEO, attorneys – have repeatedly declined comment on. There are several reasons this platform periodically looks outside the strict boundaries of MHVille in providing news, tips, and views pros can use. Because sometimes, sometimes, what happens outside of MHVille informs what is possible in MHVille. For instance.

Bernie Madoff was once thought of as untouchable. Who would have thought a year ago that Google could face a breakup due to antitrust efforts launched during the Trump Administration? What caused Google to be deemed a monopolist? Evidence said the judge.

MHProNews/MHLivingNews is hardly alone in pointing out the problems that emerged in manufactured housing as a result of what Doug Ryan called Berkshire-Clayton’s monopolistic grasp of the industry. MHProNews has not created an exhaustive look at the subject, but it has arguably been the deepest, most thoroughly researched and reported by any known source in MHVille. Others appear willing to look the other way, while MHProNews/MHLivingNews have lined up the evidence and authorities’ voices and their arguments. So, these are not the mere opinions of this publication’s leadership, these are well evidenced from people that in some cases were Buffett-believers before they turned away to say that Buffett and Berkshire has undermined American capitalism, and perhaps more specifically, manufactured housing.

These examples that span the left, right, independent, etc. niches reflect reality. Reality, not fables or nice sounding narratives, are what people operate in.

Note that some of these sources, such as Bud Labitan, is apparently in the Buffett-Berkshire orbit. Along with Buffett’s own words, actions, and those of his lieutenants in MHVille, Kevin Clayton, Tim Williams, or Tom Hodges, they may be particularly damning evidence should antitrust action be launched against Berkshire and Clayton.

Among the four lawmakers who signed the letter to the Justice Department (DOJ) and the Consumer Financial Protection Bureau (CFPB), two of them are attorneys. Per Copilot:

Copilot points out that those lawmakers who aren’t attorneys often have people with legal experience on their staff. Committees routinely have staff attorneys. Meaning, getting a legal opinion is not difficult for most Congressional lawmakers.

14) It has been MHProNews’ fact-based editorial view that direct evidence exists for Clayton and 21st violating antitrust laws. Note that in the image below, many browsers and devices allow a reader to click on the image, open a dialogue box, and select a larger size for the image, or click here and open the below in a new window. Close that window to return to this page.

15) What does that array of sources and allegations mean? That there is ample evidence for antitrust action. And there is an evidence-based argument to be made that so long as someone isn’t intimidated into thinking that Clayton-21st et al, or the Berkshire parent company, are somehow invulnerable. What is necessary is people with the cojones willing to take them on.

The fact that so much has been said about the moat and apparent antitrust violations in MHVille are reasons why the moat can be breached. The very things that may seem to make them untouchable are precisely why they are vulnerable. The current assistant AG over antitrust, Jonathan Kanter, has specifically mentioned the moat as an area of interest.

16) There has apparently been an increasing level of interest and acceptance of monopolistic/antitrust violations as being an issue of importance for Americans. That too is good news. It isn’t just MHProNews/MHLivingNews that has hammered away at this issue, others in media beyond MHVille have too. As public awareness grows, the opportunity for serious antitrust efforts grows too.

17) While Democrats may seem to be somewhat more antitrust focused, their record in most of the past 12 of the last 16 years indicates that Democratic leaders are closely aligned with the monopolists that they may publicly decry. That notion is supported by several mainstream media reports, and remarks. See examples linked below.

18) The political developments in the last few days may have shifted the electoral winds in favor of a lifelong-Democrat Bobby Kennedy Jr. backing deposed President Donald J. Trump, who has already proven willing to take on the giants of American business. Those who want to see the power of financial giants in and beyond MHVille trimmed should consider supporting Kennedy- and Elon Musk-backed Trump.

Our son has grown quite a bit since this 12.2019 photo. All on Capitol Hill were welcoming and interested in our manufactured housing industry related concerns. But Congressman Al Green’s office was tremendous in their hospitality. Our son’s hand is on a package that included the Constitution of the United States, bottled water, and other goodies.

Tony earned a journalism scholarship and earned numerous awards in history and in manufactured housing.

For example, he earned the prestigious Lottinville Award in history from the University of Oklahoma, where he studied history and business management. He’s a managing member and co-founder of LifeStyle Factory Homes, LLC, the parent company to MHProNews, and MHLivingNews.com.

This article reflects the LLC’s and/or the writer’s position and may or may not reflect the views of sponsors or supporters.

{kind=link}