Legacy Housing (LEGH) is only a fraction of the size of manufactured housing rivals Cavco Industries (CVCO) or Skyline Campion (SKY). Clayton Homes (BRK) is reportedly equal in output to all of the rest of manufactured housing combined, so they clearly dwarf Legacy Housing. But with the recent absorption of The Commodore Corporation (TCC) into Cavco Industries family of once independently owned brands, Legacy is the clear number 4 publicly traded producer of HUD Code manufactured homes in the industry, and near the top of the remaining manufactured home builders. Somewhat like other producers, Legacy builds some non-HUD Code factory built housing product. In that regard, Legacy has touted what they brand as “Tiny Homes.” Legacy has not yet pursued with a similar vigor as their larger rivals more residential style product. Legacy is vertically integrated, as are Clayton, CVCO, or SKY. Each of those four Manufactured Housing Institute (MHI) member firm sells to independently owned communities and/or independently owned ‘street retailers.’ Legacy is developing properties due in part to what Executive Chairman Curt Hodges has dubbed a “place to put” problem that HUD Code builders face.

This report and analysis will include recently released facts from Legacy Housing. It will link to information previously provided or obtained by Clayton Homes (BRK), Skyline Champion (SKY), and Cavco Industries. Unlike the so-called Big Three (Big 3) MHI members Clayton, Cavco, or SKY, Legacy leaders often do not ‘waste time’ attending MHI meetings. Legacy has thus far eschewed consolidation of other brands. They have focused instead on organic growth.

So what makes what follows the latest Legacy data, statements, and some examples of other media statements about Legacy a High Noon analysis and commentary?

Briefly, “High Noon” was a classic Western movie about bad guys vs. a good town Marshall – Will Kane played by Gary Cooper. There are no reported literal bullets flying at MHI meetings. There has been no recent literal wedding between Kane and his bride Amy, a pacifist Quaker woman. There is obvious equivalent to Helen Ramirez (played by Katy Jurado), a Hispanic dame who could mix business with suggested pleasures. There is no literal growing and aspiring town with citizens to compete for their loyalties as the climatic show down approaches. So why High Noon?

You’ll see a movie trailer video clip and the answer to that following the latest from Legacy and others, as shown below, in our Additional Information, More MHProNews Analysis and Commentary will be a keen peek behind the curtains at some High Noon insights.

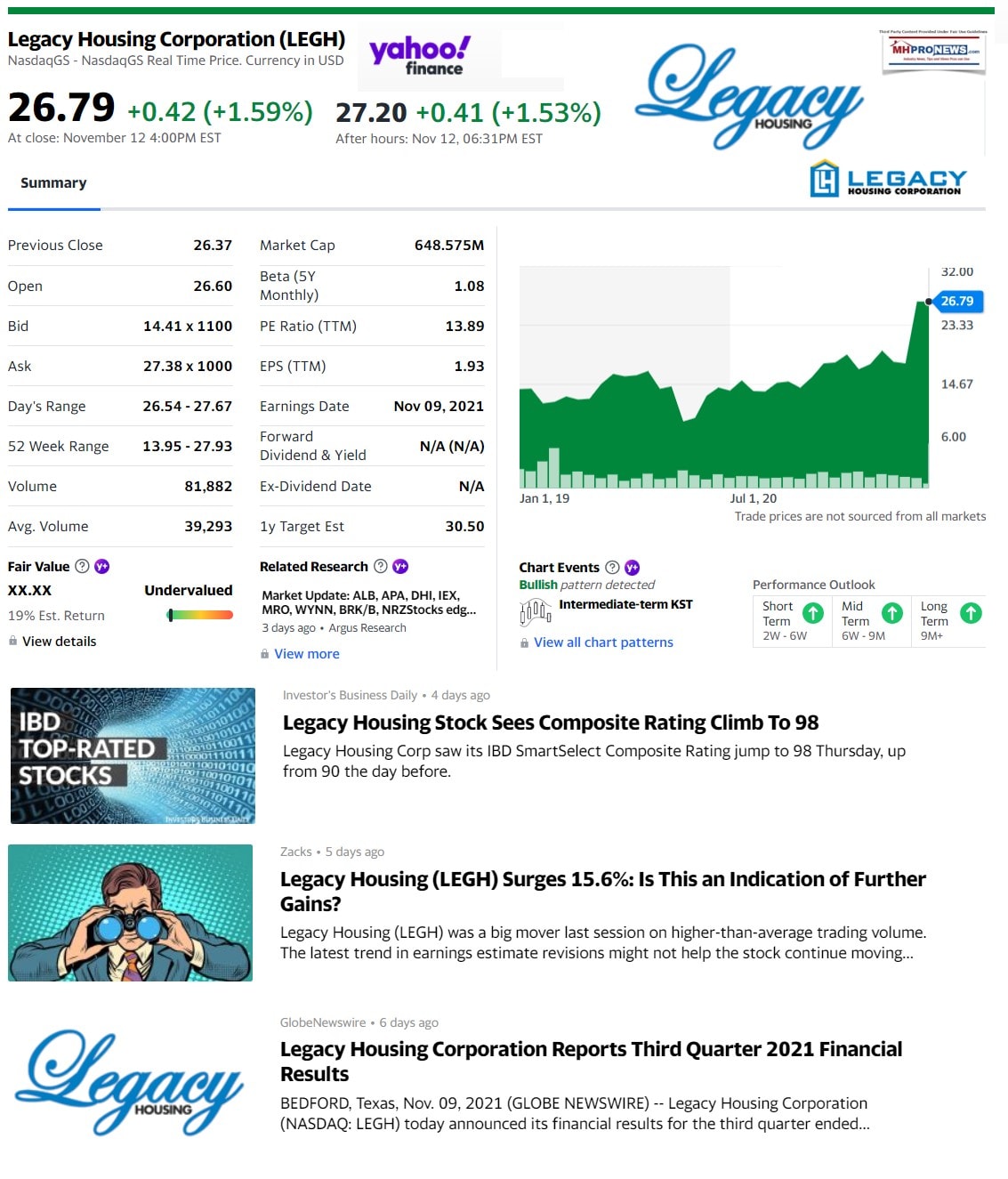

The following items are from MarketScreener.

Financials (USD)

|

|

Consensus

| Sell

Buy |

|

| Mean consensus | BUY |

| Number of Analysts | 2 |

| Last Close Price | 26,79 $ |

| Average target price | 30,50 $ |

| Spread / Average Target | 13,8% |

Managers and Directors

| Kenneth E. Shipley | President, Chief Executive Officer & Director |

| Thomas J. Kerkaert | Chief Financial Officer |

| Curtis Drew Hodgson | Executive Chairman |

| Stephen L. Crawford | Independent Director |

| Robert D. Bates | Independent Director |

Highlighting in these federally filed statements are added by MHProNews.

Via a FORM 8-K filing with the Securities and Exchange Commission (SEC) on November 12, 2021 are the following statements.

Item 2.02. Results of Operations and Financial Condition.

On November 9, 2021, Legacy Housing Corporation (the “Company”) issued a press release disclosing the financial results for its fiscal quarter ended June 30, 2021. A copy of the press release is being furnished as Exhibit 99.1 to this Current Report on Form 8-K and is incorporated into this Item by reference.

The information in Item 2.02 of this Current Report on Form 8-K and Exhibit 99.1 attached hereto is intended to be furnished and shall not be deemed “filed” for purposes of Section 18 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), or otherwise subject to the liabilities of that section. This information shall not be deemed incorporated by reference into any filing under the Securities Act of 1933, as amended, or the Exchange Act, except as expressly set forth by specific reference therein.

Item 9.01 Financial Statements and Exhibits.

- Exhibits

Exhibit No. Description

| 99.1 | Financial Results Press Release issued by Legacy Housing Corporation on November 9, 2021. [Shown above] | |

| 104 | Cover Page Interactive Data File (formatted as Inline XBRL). | |

SIGNATURES

Pursuant to the requirement of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

LEGACY HOUSING CORPORATION

Date: November 12, 2021 By: /s/ Thomas Kerkaert

Name: Thomas Kerkaert

Title: Chief Financial Officer

Legacy Housing Corporation Reports Third Quarter 2021 Financial Results

BEDFORD, Texas, November 9, 2021 (GLOBE NEWSWIRE) — Legacy Housing Corporation (NASDAQ:

LEGH) today announced its financial results for the third quarter ended September 30, 2021.

Financial Highlights:

- Net revenue for the third quarter of 2021 was $56.5 million. This was a 29.1% or $12.7 million increase from the third quarter of 2020.

- Interest revenue from our consumer and mobile home park portfolios for the third quarter of 2021 was $7.3 million. This was a 12.9% or $0.8 million increase from the third quarter of 2020.

- Gross margin for the third quarter of 2021 was $14.9 million or 30.9% of product sales compared to $8.7 million or 23.9% of product sales from the third quarter of 2020.

- Income from operations during the third quarter of 2021 was $17.6 million compared to the $10.8 million recorded in the third quarter of 2020.

- Net income in the third quarter of 2021 was $14.7 million. Compared to the third quarter of 2020, net income increased by $6.3 million. The improvement in net income was the result of stronger gross margins, increased interest revenue, and a lowered effective tax rate.

- Diluted earnings per share for the third quarter of 2021 were $0.61. Compared to the third quarter of 2020, this was an increase of 74.3% or $0.26.

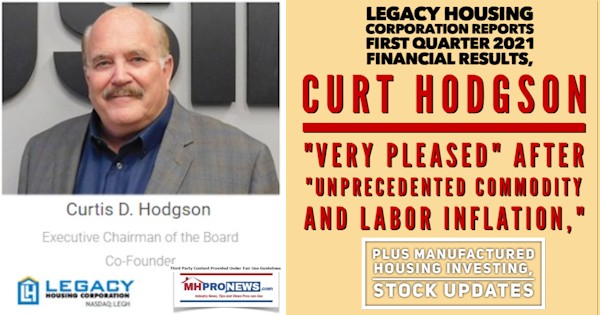

Curtis D. Hodgson, Executive Chairman of the Board, commented, “We are quite pleased with our excellent third quarter results. The growth in our gross margins illustrates how we continue to proactively manage our business in the face of supply chain challenges and inflationary conditions. The demand for our product remains solid and our backlog is very strong. Our future is bright as we move strategically to create long-term value for our shareholders.”

This shall not constitute an offer to sell or the solicitation of an offer to buy, nor shall there be any sale of the Company’s securities in any state or jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such state or jurisdiction.

Management Conference Call – Wednesday, November 10 at 9:30 AM (Central Time)

Senior management will discuss the results of the third quarter of 2021 in a live webcast and conference call on Wednesday, November 10th, 2021 at 9:30 AM Central Time. To register and participate in the webcast, please go to https://edge.media-server.com/mmc/p/ckbfsadk, which will also be accessible via www.legacyhousingusa.com under the Investors link. In order to dial in, please call in at 866-952-6347 and enter Conference ID 5297726 when prompted. Please try to join the webcast or call at least ten minutes prior to the scheduled start time.

About Legacy Housing Corporation

Legacy Housing Corporation builds, sells and finances manufactured homes and “tiny houses” that are distributed through a network of independent retailers and company-owned stores and are sold directly to manufactured housing communities. We are the sixth largest producer of manufactured homes in the United States as ranked by number of homes manufactured based on the information available from the Manufactured Housing Institute. With current operations focused primarily in the southern United States, we offer our customers an array of quality homes ranging in size from approximately 390 to 2,667 square feet consisting of 1 to 5 bedrooms, with 1 to 3 1/2 bathrooms. Our homes range in price, at retail, from approximately $22,000 to $140,000.

Forward Looking Statements

This press release contains forward-looking statements within the meaning of the Securities and Exchange Act of 1934 and the Private Securities Litigation Reform Act of 1995. These forward-looking statements are subject to a number of risks and uncertainties, many of which are beyond our control. As a result, our actual results or performance may differ materially from anticipated results or performance. Legacy Housing undertakes no obligation to update any such forward-looking statements after the date hereof, except as required by law. Investors should not place any reliance on any such forward-looking statements.

Investor Inquiries:

Shane Allred, Director of Financial Reporting, (817) 799-4903 investors@legacyhousingcorp.com

or

Media Inquiries:

Kira Hovancik, (817) 799-4905

pr@legacyhousingcorp.com

From Legacy Housing’s November 9, 10 Q filing with the SEC are the following.

PART I – FINANCIAL INFORMATION

Item 1. Financial Statements

LEGACY HOUSING CORPORATION

CONDENSED BALANCE SHEETS

(in thousands, except share and per share data)

(unaudited)

| September 30, | December 31, | ||||||

| 2021 | 2020 | ||||||

| Assets | |||||||

| Current assets: | |||||||

| Cash and cash equivalents | $ | 853 | $ | 768 | |||

| Accounts receivable, net | 8,226 | 3,867 | |||||

| Current portion of consumer loans | 5,883 | 5,348 | |||||

| Current portion of notes receivable from mobile home parks (“MHP”) | 10,591 | 12,468 | |||||

| Current portion of other notes receivable | 15,128 | 2,054 | |||||

| Inventories | 36,951 | 27,224 | |||||

| Prepaid expenses and other current assets | 5,805 | 3,234 | |||||

| Total current assets | 83,437 | 54,963 | |||||

| Consumer loans, net | 115,754 | 106,572 | |||||

| Notes receivable from mobile home parks (“MHP”) | 89,642 | 123,872 | |||||

| Other notes receivable, net | 19,342 | 13,050 | |||||

| Inventories, net | 3,524 | 8,656 | |||||

| Other assets | 10,862 | 8,887 | |||||

| Property, plant and equipment, net | 26,428 | 22,616 | |||||

| Total assets | $ | 348,989 | $ | 338,616 | |||

| Liabilities and Stockholders’ Equity | |||||||

| Current liabilities: | |||||||

| Accounts payable | $ | 6,170 | $ | 10,197 | |||

| Accrued liabilities | 17,073 | 14,860 | |||||

| Customer deposits | 6,344 | 3,620 | |||||

| Escrow liability | 9,350 | 7,729 | |||||

| Total current liabilities | 38,937 | 36,406 | |||||

| Long‑term liabilities: | |||||||

| Lines of credit | 8,281 | 36,174 | |||||

| Deferred income taxes | 1,971 | 1,971 | |||||

| Accrued liabilities, net of current portion | — | 630 | |||||

| Dealer incentive liability | 4,160 | 4,242 | |||||

| Total liabilities | 53,349 | 79,423 | |||||

| Commitments and contingencies (Note 12) | |||||||

| Stockholders’ equity: | |||||||

| Preferred stock, $.001 par value, 10,000,000 shares authorized: no shares issued or | |||||||

| outstanding | — | — | |||||

| Common stock, $.001 par value, 90,000,000 shares authorized; 24,654,621 and 24,639,125 | |||||||

| issued and 24,209,556 and 24,194,060 outstanding at September 30, 2021 and December 31, | |||||||

| 2020, respectively | 25 | 25 | |||||

| Treasury stock at cost, 445,065 shares at September 30, 2021 and December 31, 2020 | (4,477) | (4,477) | |||||

| Additional paid-in-capital | 175,556 | 175,293 | |||||

| Retained earnings | 124,536 | 88,352 | |||||

| Total stockholders’ equity | 295,640 | 259,193 | |||||

| Total liabilities and stockholders’ equity | $ | 348,989 | $ | 338,616 | |||

See accompanying notes to condensed financial statements.

2

LEGACY HOUSING CORPORATION

CONDENSED STATEMENTS OF OPERATIONS

(in thousands, except share and per share data)

(unaudited)

| Three months ended September 30, | Nine months ended September 30, | |||||||||||||

| 2021 | 2020 | 2021 | 2020 | |||||||||||

| Net revenue: | ||||||||||||||

| Product sales | $ | 48,300 | $ | 36,566 | $ | 121,689 | $ | 106,940 | ||||||

| Consumer and MHP loans interest | 7,259 | 6,428 | 20,631 | 18,919 | ||||||||||

| Other | 911 | 749 | 2,679 | 2,163 | ||||||||||

| Total net revenue | 56,470 | 43,743 | 144,999 | 128,022 | ||||||||||

| Operating expenses: | ||||||||||||||

| Cost of product sales | 33,392 | 27,839 | 86,024 | 78,387 | ||||||||||

| Selling, general and administrative expenses | 5,045 | 4,525 | 15,005 | 14,202 | ||||||||||

| Dealer incentive | 421 | 550 | 998 | 929 | ||||||||||

| Income from operations | 17,612 | 10,829 | 42,972 | 34,504 | ||||||||||

| Other income (expense): | ||||||||||||||

| Non‑operating interest income | 588 | 246 | 1,265 | 697 | ||||||||||

| Miscellaneous, net | 116 | 96 | 354 | 145 | ||||||||||

| Gain on settlement, net | — | — | — | 1,075 | ||||||||||

| Interest expense | (318) | (239) | (827) | (817) | ||||||||||

| Total other | 386 | 103 | 792 | 1,100 | ||||||||||

| Income before income tax expense | 17,998 | 10,932 | 43,764 | 35,604 | ||||||||||

| Income tax expense | (3,265) | (2,486) | (7,581) | (8,097) | ||||||||||

| Net income | $ | 14,733 | $ | 8,446 | $ | 36,183 | $ | 27,507 | ||||||

| Weighted average shares outstanding: | ||||||||||||||

| Basic | 24,204,362 | 24,192,157 | 24,202,053 | 24,237,402 | ||||||||||

| Diluted | 24,283,666 | 24,214,279 | 24,279,846 | 24,243,927 | ||||||||||

| Net income per share: | ||||||||||||||

| Basic | $ | 0.61 | $ | 0.35 | $ | 1.50 | $ | 1.13 | ||||||

| Diluted | $ | 0.61 | $ | 0.35 | $ | 1.49 | $ | 1.13 | ||||||

See accompanying notes to condensed financial statements.

3

LEGACY HOUSING CORPORATION

CONDENSED STATEMENTS OF CASH FLOWS

(unaudited, in thousands)

| Nine months ended September 30, | |||||||

| 2021 | 2020 | ||||||

| Operating activities: | |||||||

| Net income | $ | 36,183 | $ | 27,507 | |||

| Adjustments to reconcile net income to net cash provided by (used in) operating | |||||||

| activities: | |||||||

| Depreciation expense | 1,157 | 874 | |||||

| Amortization of debt discount and issuance costs | (542) | 35 | |||||

| Provision for loan loss—consumer loans | 586 | 586 | |||||

| Share based payment expense | 163 | 177 | |||||

| Changes in operating assets and liabilities: | |||||||

| Accounts receivable | (4,359) | (741) | |||||

| Consumer loans originations | (19,954) | (12,647) | |||||

| Consumer loans principal collections | 9,379 | 7,945 | |||||

| Notes receivable MHP originations | (36,897) | (54,630) | |||||

| Notes receivable MHP principal collections | 72,209 | 17,364 | |||||

| Inventories | (4,595) | 1,166 | |||||

| Prepaid expenses and other current assets | (2,571) | 1,959 | |||||

| Other assets | (2,352) | (2,704) | |||||

| Accounts payable | (4,027) | (405) | |||||

| Accrued liabilities | 1,583 | 3,797 | |||||

| Customer deposits | 2,724 | 902 | |||||

| Escrow liability | 1,621 | 775 | |||||

| Dealer incentive liability | (82) | 467 | |||||

| Net cash provided by (used in) operating activities | 50,226 | (7,573) | |||||

| Investing activities: | |||||||

| Purchases of property, plant and equipment | (4,596) | (2,156) | |||||

| Issuance of notes receivable | (27,127) | (5,430) | |||||

| Notes receivable collections | 7,761 | 3,247 | |||||

| Purchases of loans | — | (317) | |||||

| Collections from purchased loans | 1,614 | 902 | |||||

| Net cash used in investing activities | (22,348) | (3,754) | |||||

| Financing activities: | |||||||

| Proceeds from exercise of stock options | 100 | — | |||||

| Treasury stock purchase | — | (1,417) | |||||

| Proceeds from issuance of note payable | — | 6,546 | |||||

| Principal payments on note payable | — | (6,546) | |||||

| Proceeds from lines of credit | 75,272 | 52,148 | |||||

| Payments on lines of credit | (103,165) | (39,485) | |||||

| Net cash used in financing activities | (27,793) | 11,246 | |||||

| Net increase (decrease) in cash and cash equivalents | 85 | (81) | |||||

| Cash and cash equivalents at beginning of period | 768 | 1,724 | |||||

| Cash and cash equivalents at end of period | $ | 853 | $ | 1,643 | |||

| Supplemental disclosure of cash flow information: | |||||||

| Cash paid for interest | $ | 548 | $ | 770 | |||

| Cash paid for taxes | $ | 8,194 | $ | 6,728 | |||

See accompanying notes to condensed financial statements.

4

LEGACY HOUSING CORPORATION

CONDENSED STATEMENTS OF CHANGES IN STOCKHOLDERS’ EQUITY

(in thousands, except share data)

(unaudited)

| Common Stock | Treasury | Additional | Retained | |||||||||||||||||||||||||||||||

| Shares | Amount | stock | paid-in-capital | earnings | Total | |||||||||||||||||||||||||||||

| Balances, December 31, 2019 | 24,620,079 | $ | 25 | $ (3,060) | $ | 175,067 | $ | 50,357 | $ 222,389 | |||||||||||||||||||||||||

| Share based compensation expense and stock | ||||||||||||||||||||||||||||||||||

| units vested | 17,143 | — | — | 97 | — | 97 | ||||||||||||||||||||||||||||

| Purchase of treasury stock | — | — | (682) | — | — | (682) | ||||||||||||||||||||||||||||

| Net income | — | — | — | — | 9,023 | 9,023 | ||||||||||||||||||||||||||||

| Balances, March 31, 2020 | 24,637,222 | 25 | (3,742) | 175,164 | 59,380 | 230,827 | ||||||||||||||||||||||||||||

| Share based compensation expense and stock | ||||||||||||||||||||||||||||||||||

| units vested | — | — | — | 36 | — | 36 | ||||||||||||||||||||||||||||

| Purchase of treasury stock | — | — | (735) | — | — | (735) | ||||||||||||||||||||||||||||

| Net income | — | — | — | — | 10,040 | 10,040 | ||||||||||||||||||||||||||||

| Balances, June 30, 2020 | 24,637,222 | 25 | (4,477) | 175,200 | 69,420 | 240,168 | ||||||||||||||||||||||||||||

| Share based compensation expense and stock | ||||||||||||||||||||||||||||||||||

| units vested | — | — | — | 44 | — | 44 | ||||||||||||||||||||||||||||

| Net income | — | — | — | — | 8,446 | 8,446 | ||||||||||||||||||||||||||||

| Balances, September 30, 2020 | 24,637,222 | $ | 25 | $ (4,477) | $ | 175,244 | $ | 77,866 | $ 248,658 | |||||||||||||||||||||||||

| Common Stock | Treasury | Additional | Retained | |||||||||||||||||||||||||||||||

| Shares | Amount | stock | paid-in-capital | earnings | Total | |||||||||||||||||||||||||||||

| Balances, December 31, 2020 | 24,639,125 | $ | 25 | $ (4,477)$ | 175,293 | $ | 88,352 | $ 259,193 | ||||||||||||||||||||||||||

| Share based compensation expense and stock | ||||||||||||||||||||||||||||||||||

| units vested | 8,571 | — | — | 44 | — | 44 | ||||||||||||||||||||||||||||

| Net income | — | — | — | — | 9,023 | 9,023 | ||||||||||||||||||||||||||||

| Balances, March 31, 2021 | 24,647,696 | 25 | (4,477) | 175,337 | 97,375 | 268,260 | ||||||||||||||||||||||||||||

| Share based compensation expense and stock | ||||||||||||||||||||||||||||||||||

| units vested | — | — | — | 64 | — | 64 | ||||||||||||||||||||||||||||

| Net income | — | — | — | — | 12,428 | 12,428 | ||||||||||||||||||||||||||||

| Balances, June 30, 2021 | 24,647,696 | 25 | (4,477) | 175,401 | 109,803 | 280,752 | ||||||||||||||||||||||||||||

| Share based compensation expense and stock | ||||||||||||||||||||||||||||||||||

| units vested | — | — | — | 55 | — | 55 | ||||||||||||||||||||||||||||

| Share based compensation expense – stock | ||||||||||||||||||||||||||||||||||

| options exercised | 6,925 | — | — | 100 | — | 100 | ||||||||||||||||||||||||||||

| Net income | — | — | — | — | 14,733 | 14,733 | ||||||||||||||||||||||||||||

| Balances, September 30, 2021 | 24,654,621 | $ | 25 | $ (4,477)$ | 175,556 | $ | 124,536 | $ 295,640 | ||||||||||||||||||||||||||

See accompanying notes to condensed financial statements.

5

LEGACY HOUSING CORPORATION NOTES TO CONDENSED FINANCIAL STATEMENTS (UNAUDITED) (dollars in thousands)

- NATURE OF OPERATIONS

Legacy Housing Corporation (referred herein as ”Legacy”, “we”, “our”, “us”, or the “Company”) was formed on January 1, 2018 as a Delaware corporation through a corporate conversion of Legacy Housing, Ltd. (the “Partnership”), a Texas limited partnership formed in May 2005. Effective December 31, 2019, the Company reincorporated from a Delaware corporation to a Texas corporation. The Company is headquartered in Bedford, Texas.

The Company (1) manufactures and provides for the transport of mobile homes, (2) provides wholesale financing to dealers and mobile home parks, (3) provides retail financing to consumers and (4) is involved in financing and developing new manufactured home communities. The Company manufactures its mobile homes at plants located in Fort Worth, Texas, Commerce, Texas and Eatonton, Georgia. The Company relies on a network of dealers to market and sell its mobile homes. The Company also sells homes directly to dealers and mobile home parks.

In December 2018, the Company sold 4,000,000 shares of its common stock through an initial public offering (“IPO”) at $12.00 per share. Proceeds from the IPO, net of $4,504 of underwriting discounts and offering expenses paid by the Company, were $43,492. In January 2019, the Company sold an additional 600,000 shares of its common stock as part of the IPO at $12.00 per share. Proceeds from the January 2019 issuance, net of $505 of underwriting discounts and offering expenses paid by the Company, were $6,695.

On April 17, 2019, the Company purchased 300,000 shares of its common stock at the price of $10.20 per share, pursuant to the Company’s repurchase program. During the year ended December 31, 2020, the Company purchased 145,065 shares of its common stock at an average price of $9.77 per share, pursuant to the Company’s repurchase program. Under the repurchase program, the Company may purchase up to $10,000 of its common stock. Share purchases may be made from time to time in the open market or through privately negotiated transactions depending on market conditions, share price, trading volume and other factors. Such purchases, if any, will be made in accordance with applicable insider trading and other securities laws and regulations. These repurchases may be commenced or suspended at any time or from time to time without prior notice.

Corporate Conversion

Effective January 1, 2018, the Partnership converted into a Delaware corporation pursuant to a statutory conversion and changed its name to Legacy Housing Corporation. In order to consummate the corporate conversion completed on January 1, 2018, a certificate of conversion was filed with the Secretary of State of the State of Delaware and with the Secretary of State of the State of Texas. Holders of partnership interests in Legacy Housing, Ltd. received an initial allocation, on a proportional basis, of 20,000,000 shares of common stock of Legacy Housing Corporation.

Following the corporate conversion, Legacy Housing Corporation continues to hold all property and assets of Legacy Housing, Ltd. and all of the debts and obligations of Legacy Housing, Ltd. On the effective date of the corporate conversion, the officers of Legacy Housing, Ltd. became the officers of Legacy Housing Corporation. As a result of the corporate conversion, the Company is now a federal corporate taxpayer.

Basis of Presentation

The accompanying unaudited interim condensed financial statements as of September 30, 2021 and for the three and nine months ended September 30, 2021 and 2020, respectively, have been prepared in accordance with accounting principles generally accepted in the United States of America (“GAAP”) for interim financial information and pursuant to the rules and regulations of the U.S. Securities and Exchange Commission (“SEC”) as required by Regulation S-X, Rule 8-03. In the opinion of management, the unaudited interim financial statements have been prepared on the same basis as the audited financial statements, and include all adjustments, consisting only of normal recurring adjustments, necessary for the fair statement of the Company’s financial position for the periods presented. The results for the three and nine months ended September 30, 2021 are not necessarily indicative of the results to be

6

LEGACY HOUSING CORPORATION NOTES TO CONDENSED FINANCIAL STATEMENTS (UNAUDITED) (dollars in thousands)

expected for the year ending December 31, 2021, or any other period. The accompanying balance sheet as of December 31, 2020 was derived from audited financial statements included in the Company’s annual report on Form 10-K for the year ended December 31, 2020 (the “Form 10-K”). The accompanying financial statements do not include all of the information and footnotes required by GAAP for annual financial statements. Accordingly, they should be read in conjunction with the audited financial statements and notes thereto included in the Form 10-K.

Use of Estimates

The preparation of our financial statements in conformity with GAAP requires management to make estimates and assumptions. These estimates and assumptions affect the reported amounts of assets and liabilities and the disclosure of contingent assets and liabilities at the date of the financial statements, as well as the reported amounts of income and expenses during the reporting period. Material estimates that are susceptible to significant change in the near term primarily relate to the determination of accounts receivable, loans to mobile home parks, consumer loans, other notes receivable, inventory obsolescence, income taxes, fair value of financial instruments and contingent liabilities. Actual results could differ from these estimates.

Revenue Recognition

Product sales primarily consist of sales of mobile homes to consumers and mobile home parks through various sales channels, which include Direct Sales, Commercial Sales, Consignment Sales, and Retail Store Sales. Direct Sales include homes sold directly to independent retailers or customers that are not financed by the Company and are not sold under a consignment arrangement. These types of homes are generally paid for prior to shipment. Commercial Sales include homes sold to mobile home parks under commercial loan programs or paid for upfront. The Company provides floor plan financing for independent retailers, which takes the form of a consignment arrangement. Consignment Sales are considered sales of consigned homes from independent dealers to individual customers. Retail Store Sales are homes sold through Company-owned retail locations. Consignment Sales and Retail Sales of homes may be financed by the Company, by a third party, or paid in cash.

Revenue from product sales is recognized at a point in time when the performance obligation under the terms of a contract with our customer is satisfied, which typically occurs upon delivery and transfer of title of the home, as this depicts when control of the promised good is transferred to our customer. For financed sales by the Company, the individual customer enters into a sales and financing contract and is required to make a down payment. These financed sales contain a significant financing component and any interest income is separately recorded in the statement of operations.

Revenue is measured as the amount of consideration expected to be received in exchange for transferring the homes to the customers. Sales and other similar taxes collected concurrently with revenue-producing activities are excluded from revenue.

The Company made an accounting policy election to account for any shipping and handling costs that occur after the transfer of control as a fulfillment cost that is accrued when control is transferred. Warranty obligations associated with the sale of a unit are assurance-type warranties for a period of twelve months that are a guarantee of the home’s intended functionality and, therefore, do not represent a distinct performance obligation within the context of the contract. The Company has elected to use the practical expedient to expense the incremental costs of obtaining a contract if the amortization period of the asset that the Company would have otherwise recognized is one year or less. Contract costs, which include commissions incurred related to the sale of homes, are expensed at the point-in-time when the related revenue is recognized. Warranty costs and contract costs are included in selling, general and administrative expenses in the statements of operations.

For the three months ended September 30, 2021 and 2020, sales to an independent third-party and its affiliates accounted for $2,335 or 4.8% and $13,253 or 36.2% of our product sales, respectively. For the nine months ended

7

LEGACY HOUSING CORPORATION NOTES TO CONDENSED FINANCIAL STATEMENTS (UNAUDITED) (dollars in thousands)

September 30, 2021 and 2020, sales to an independent third-party and its affiliates accounted for $7,399 or 6.1% and $39,559 or 37.0% of our product sales, respectively.

For the three months ended September 30, 2021 and 2020, total cost of product sales included $3,978 and $7,073 of costs relating to subcontracted production for commercial sales, reimbursed dealer expenses for consignment sales, and certain other similar costs incurred for retail store and commercial sales. For the nine months ended September 30, 2021 and 2020, total cost of product sales included $8,976 and $15,878 of costs relating to subcontracted production for commercial sales, reimbursed dealer expenses for consignment sales, and certain other similar costs incurred for retail store and commercial sales.

Other revenue consists of consignment fees, commercial lease rents, service fees and other miscellaneous income. Consignment fees are charged to independent retailers on a monthly basis for homes held by the independent retailers pursuant to a consignment arrangement until the home is sold to an individual customer. Consignment fees are determined as a percentage of the home’s wholesale price to the independent dealer. Revenue recognition for consignment fees are recognized over time using the output method as it provides a faithful depiction of the Company’s performance toward completion of the performance obligation under the contract and the value transferred to the independent retailer for the time the home is held under consignment. Revenue for commercial leases is recognized as earned monthly over a contractual period of 96 or 120 months. Revenue for service fees and miscellaneous income is recognized at a point in time when the performance obligation is satisfied.

8

LEGACY HOUSING CORPORATION NOTES TO CONDENSED FINANCIAL STATEMENTS (UNAUDITED) (dollars in thousands)

Disaggregation of Revenue. The following table summarizes customer contract revenues disaggregated by source of the revenue for the three and nine months ended September 30, 2021 and 2020:

| Three months ended | Nine months ended | ||||||||||||

| September 30, | September 30, | ||||||||||||

| 2021 | 2020 | 2021 | 2020 | ||||||||||

| Product sales: | |||||||||||||

| Direct sales | $ | 8,434 | $ | 1,453 | $ | 17,093 | $ | 7,528 | |||||

| Commercial sales | 12,198 | 17,681 | 37,840 | 54,532 | |||||||||

| Consignment sales | 18,641 | 11,950 | 43,381 | 29,875 | |||||||||

| Retail store sales | 5,929 | 3,939 | 15,435 | 11,475 | |||||||||

| Other (1) | 3,098 | 1,543 | 7,940 | 3,530 | |||||||||

| Total product sales | 48,300 | 36,566 | 121,689 | 106,940 | |||||||||

| Consumer and MHP loans interest: | |||||||||||||

| Interest – consumer installment notes | 4,019 | 4,014 | 12,208 | 11,983 | |||||||||

| Interest – MHP notes | 3,240 | 2,414 | 8,423 | 6,936 | |||||||||

| Total consumer and MHP loans interest | 7,259 | 6,428 | 20,631 | 18,919 | |||||||||

| Other | 911 | 749 | 2,679 | 2,163 | |||||||||

| Total net revenue | $ | 56,470 | $ | 43,743 | $ | 144,999 | $ | 128,022 | |||||

(1) Other product sales revenue from ancillary products and services including parts, freight and other services Share-Based Compensation

The Company accounts for share-based compensation in accordance with the provisions of Accounting Standards Codification (“ASC”) 718, Compensation—Stock Compensation. Share-based compensation expense is recognized based on the award’s estimated grant date fair value in order to recognize compensation cost for those shares expected to vest.

The Company has elected to record forfeitures as they occur. Compensation cost is recognized on a straight-line basis over the vesting period of the awards and adjusted as forfeitures occur.

The fair value of each option grant with only service-based conditions is estimated using the Black-Scholes pricing model. The fair value of each restricted stock unit (the ”RSU”) is calculated based on the closing price of the Company’s common stock on the grant date.

The fair value of stock option awards on the date of grant is estimated using the Black-Scholes option pricing model, which requires the Company to make certain predictive assumptions. The risk-free interest rate is based on the implied yield of U.S. Treasury zero-coupon securities that correspond to the expected life of the award. As a recently formed public entity with a small public float and limited trading of its common shares on the NASDAQ Global Market, it was not practicable for the Company to estimate the volatility of its common shares; therefore, management estimated volatility based on the historical volatilities of a small group of companies considered as close to comparable to the Company as available, all equally weighted, over the expected life of the option. Management concluded that this group is more characteristic of the Company’s business than a broad industry index. The expected life of awards granted represents the period of time that the awards are expected to be outstanding based on the “simplified” method, which is allowed for companies that cannot reasonably estimate the expected life of options based on its historical award exercise experience. The Company does not expect to pay dividends on its common stock.

9

LEGACY HOUSING CORPORATION NOTES TO CONDENSED FINANCIAL STATEMENTS (UNAUDITED) (dollars in thousands)

Accounts Receivable

Included in accounts receivable are receivables from direct sales of mobile homes, sales of parts and supplies to customers, consignment fees and interest.

Accounts receivables are generally due within 30 days and are stated at amounts due from customers net of an allowance for doubtful accounts. Accounts outstanding longer than the contractual payment terms are considered past due. The Company determines the allowance by considering several factors, including the aging of the past due balance, the customer’s payment history, and the Company’s previous loss history. The Company establishes an allowance for doubtful accounts for amounts that are deemed to be uncollectible. At September 30, 2021 and December 31, 2020, the allowance for doubtful accounts totaled $318 and $97, respectively.

Leased Property

The Company offers mobile home park operators the opportunity to lease mobile homes for rent in lieu of purchasing the homes for cash or under a longer-term financing agreement. In this arrangement title for the mobile homes remains with the Company.

The standard lease agreement is typically for 96 months or 120 months. Under the lease arrangement, the lessee (mobile home park operator) uses the mobile homes as personal property to be rented as a residence at the lessee’s mobile home park. The lessee makes monthly, periodic lease payments to the Company over the term of the lease. The lessee is responsible for maintaining the homes during the term of the lease. The lessee is also responsible for repairing all damages caused by force majeure events even in cases of total or partial loss of the property. At the end of the lease term or in the event of default, the lessee is required to deliver to the Company the homes with all improvements in good repair and condition in substantially the same condition as existed at the commencement of the lease. The lessee may terminate the lease with 30 days written notice to the Company and pay a lease termination fee equal to 10% of the remaining lease payments or six month’s rent, whichever is greater. The lessee has an option to purchase the homes at the end of the lease term for fair market value based on an agreed upon determination of fair market value by both parties using comparable sales, recent appraisal, or NADA official guidance. The lessee must provide the Company with 30 days written notice prior to expiration of the lease of intent to purchase the property for fair market value. The lease also includes a renewal option whereby the lessee has the option to extend the lease for an additional 48 months (the extended term) at the same terms and conditions as the original lease. The lessee must notify the Company of the intent to exercise the renewal extension option not less than six months prior to expiration of the lease term. The leased mobile homes are included in other assets on the Company’s balance sheet, capitalized at manufactured cost and depreciated over a 15 year useful life. Homes returned to the Company upon expiration of the lease or in the event of default will be sold by the Company through its standard sales and distribution channels.

Future minimum lease income under all operating leases for each of the next five years at September 30, 2021, are as follows:

| 2021 | $ | 473 | ||||

| 2022 | 1,924 | |||||

| 2023 | 1,924 | |||||

| 2024 | 1,924 | |||||

| 2025 | 1,924 | |||||

| Thereafter | 6,052 | |||||

| Total | $ | 14,221 | ||||

| 10 | ||||||

LEGACY HOUSING CORPORATION NOTES TO CONDENSED FINANCIAL STATEMENTS (UNAUDITED) (dollars in thousands)

Recent Accounting Pronouncements

The Company has elected to use longer phase-in periods for the adoption of new or revised financial accounting standards under the JOBS Act as an emerging growth company.

In February 2016, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update (“ASU”) 2016-02, Leases (Topic 842), to increase transparency and comparability among organizations by recognizing lease assets and lease liabilities on the balance sheet and disclosing key information about leasing arrangements. A lessee should recognize in the balance sheet a liability to make lease payments (the lease liability) and an asset representing its right to use the underlying asset for the lease term. The recognition, measurement and presentation of expenses and cash flows arising from a lease by a lessee have not significantly changed from previous requirements. The Company plans to use the longer phase-in period for adoption, and accordingly this ASU is effective for the Company’s fiscal year beginning January 1, 2022. Modified retrospective application and early adoption is permitted. The Company expects that the adoption of this standard will result in a material increase to assets and liabilities on the balance sheet, but will not have a material impact on the statement of operations. While the Company is continuing to assess all the effects of adoption, it currently believes the most significant effects relate to (i) the recognition of new right-of-use assets and lease liabilities on its balance sheet for its property and equipment operating leases and (ii) providing significant new disclosures about its leasing activities.

In June 2016, the FASB issued ASU 2016-13 Financial Instruments—Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments, which amends guidance on reporting credit losses for assets held at amortized cost basis and available for sale debt securities. For assets held at amortized cost basis, Topic 326 eliminates the probable initial recognition threshold in current GAAP and, instead, requires an entity to reflect its current estimate of all expected credit losses. The allowance for credit losses is a valuation account that is deducted from the amortized cost basis of the financial assets to present the net amount expected to be collected. For available for sale debt securities, credit losses should be measured in a manner similar to current GAAP, however Topic 326 will require that credit losses be presented as an allowance rather than as a write-down and affects entities holding financial assets and net investment in leases that are not accounted for at fair value through net income. The amendments affect loans, debt securities, trade receivables, net investments in leases, off balance sheet credit exposures, reinsurance receivables, and any other financial assets not excluded from the scope that have the contractual right to receive cash. The Company plans to use the longer phase-in period for adoption, and accordingly this ASU is effective for the Company’s fiscal year beginning January 1, 2023. The Company is continuing to evaluate the impact of the adoption of this ASU and is uncertain of the impact on the financial statements and disclosures at this point in time.

From time to time, new accounting pronouncements are issued by the FASB and other regulatory bodies that are adopted by the Company as of the specified effective dates. Unless otherwise discussed, management believes that the impact of recently issued standards, which are not yet effective, will not have a material impact on the Company’s financial statements upon adoption.

- CONSUMER LOANS

Consumer loans result from financing transactions entered into with retail consumers of mobile homes sold through independent retailers and company-owned retail locations. Consumer loans receivable generally consist of the sales price and any additional financing fees, less the buyer’s down payment. Interest income is recognized monthly per the terms of the financing agreements. The average contractual interest rate per loan was approximately 13.6% as of September 30, 2021 and 13.8% as of December 31, 2020. Consumer loans receivable have maturities that range from 3 to 30 years.

Loan applications go through an underwriting process that considers credit history to evaluate credit risk of the consumer. Interest rates on approved loans are determined based on consumer credit score, payment ability and down payment amount.

11

LEGACY HOUSING CORPORATION NOTES TO CONDENSED FINANCIAL STATEMENTS (UNAUDITED) (dollars in thousands)

The Company uses payment history to monitor the credit quality of the consumer loans on an ongoing basis.

The Company may also receive escrow payments for property taxes and insurance included in its consumer loan collections. The liabilities associated with these escrow collections totaled $9,350 and $7,729 as of September 30, 2021 and December 31, 2020, respectively, and are included in escrow liability in the balance sheets.

Allowance for Loan Losses—Consumer Loans Receivable

The allowance for loan losses reflects management’s estimate of losses inherent in the consumer loans that may be uncollectible based upon review and evaluation of the consumer loan portfolio as of the date of the balance sheet. An allowance for loan losses is determined after giving consideration to, among other things, the loan characteristics, including the financial condition of borrowers, the value and liquidity of collateral, delinquency and historical loss experience.

The allowance for loan losses is comprised of two components: the general reserve and specific reserves. The Company’s calculation of the general reserve considers the historical loss rate for the last three years, adjusted for the estimated loss discovery period and any qualitative factors both internal and external to the Company. Specific reserves are determined based on probable losses on specific classified impaired loans.

The Company’s policy is to place a loan on nonaccrual status when there is a clear indication that the borrower’s cash flow may not be sufficient to meet payments as they become due, which is when either principal or interest is past due and remains unpaid for more than 90 days or other indications of distress. Management implemented this policy based on an analysis of historical data, current performance of loans and the likelihood of recovery once principal or interest payments became delinquent and were aged more than 90 days. Payments received on nonaccrual loans are accounted for on a cash basis, first to interest and then to principal, as long as the remaining book balance of the asset is deemed to be collectible. The accrual of interest resumes when the past due principal or interest payments are brought within 90 days of being current.

Impaired loans are those loans where it is probable the Company will be unable to collect all amounts due in accordance with the original contractual terms of the loan agreement, including scheduled principal and interest payments. Impaired loans, or portions thereof, are charged off when deemed uncollectible. A loan is generally deemed impaired if it is more than 90 days past due on principal or interest, is in bankruptcy proceedings, or is in the process of repossession. A specific reserve is created for impaired loans based on fair value of underlying collateral value, less estimated selling costs. The Company uses various factors to determine the value of the underlying collateral for impaired loans. These factors are:

- the length of time the unit was unsold after construction; (2) the amount of time the house was occupied; (3) the cooperation level of the borrowers, i.e., loans requiring legal action or extensive field collection efforts; (4) units located on private property as opposed to a manufactured home park; (5) the length of time the borrower has lived in the house without making payments; (6) location, size, and market conditions; and (7) the experience and expertise of the particular dealer assisting in collection efforts.

Collateral for repossessed loans is acquired through foreclosure or similar proceedings and is recorded at the estimated fair value of the home, less the costs to sell. At repossession, the fair value of the collateral is computed based on the historical recovery rates of previously charged off loans; the loan is charged off and the loss is charged to the allowance for loan losses. At each reporting period, the fair value of the collateral is adjusted to the lower of the amount recorded at repossession or the estimated sales price less estimated costs to sell, based on current information. Repossessed homes totaled $698 and $1,395 as of September 30, 2021 and December 31, 2020, respectively, and are included in other assets in the balance sheets.

12

LEGACY HOUSING CORPORATION NOTES TO CONDENSED FINANCIAL STATEMENTS (UNAUDITED) (dollars in thousands)

Consumer loans receivable, net of allowance for loan losses and deferred financing fees, consists of the following:

| As of | As of | |||||||

| September 30, | December 31, | |||||||

| 2021 | 2020 | |||||||

| Consumer loans receivable | $ | 125,089 | $ | 115,639 | ||||

| Loan discount and deferred financing fees | (2,650) | (2,814) | ||||||

| Allowance for loan losses | (802) | (905) | ||||||

| Consumer loans receivable, net | $ | 121,637 | $ | 111,920 | ||||

The following table presents a detail of the activity in the allowance for loan losses:

| Three months ended | Nine Months Ended | |||||||||||||||||

| September 30, | September 30, | |||||||||||||||||

| 2021 | 2020 | 2021 | 2020 | |||||||||||||||

| Allowance for loan losses, beginning of period | $ | 814 | $ 916 | $ | 905 | $ | 913 | |||||||||||

| Provision for loan losses | 27 | 306 | 586 | 586 | ||||||||||||||

| Charge offs | (39) | (172) | (689) | (449) | ||||||||||||||

| Allowance for loan losses | $ | 802 | $ 1,050 | $ | 802 | $ 1,050 | ||||||||||||

| The reserve for loan losses consists of the following: | ||||||||||||||||||

| As of | As of | |||||||||||||||||

| September 30, | December 31, | |||||||||||||||||

| 2021 | 2020 | |||||||||||||||||

| Total consumer loans | $ | 125,089 | $ | 115,639 | ||||||||||||||

| Allowance for loan losses | $ | 802 | $ | 905 | ||||||||||||||

| Impaired loans individually evaluated for impairment | $ | 1,328 | $ | 1,603 | ||||||||||||||

| Specific reserve against impaired loans | $ | 437 | $ | 558 | ||||||||||||||

| Other loans collectively evaluated for allowance | $ | 123,761 | $ | 114,036 | ||||||||||||||

| General allowance for loan losses | $ | 365 | $ | 347 | ||||||||||||||

As of September 30, 2021 and December 31, 2020, the total principal outstanding for consumer loans on nonaccrual status was $1,328 and $1,603, respectively. A detailed aging of consumer loans receivable that are past due as of September 30, 2021 and December 31, 2020 were as follows:

| As of September 30, | % | As of December 31, | % | |||||||||

| 2021 | 2020 | |||||||||||

| Total consumer loans receivable | $ | 125,089 | 100.0 | $ | 115,639 | 100.0 | ||||||

| Past due consumer loans: | ||||||||||||

| 31 | – 60 days past due | $ | 316 | 0.3 | $ | 954 | 0.8 | |||||

| 61 | – 90 days past due | 440 | 0.4 | 221 | 0.2 | |||||||

| 91 | – 120 days past due | 111 | 0.1 | 141 | 0.1 | |||||||

| Greater than 120 days past due | 885 | 0.7 | 1,261 | 1.1 | ||||||||

| Total past due | $ | 1,752 | 1.4 | $ | 2,577 | 2.2 | ||||||

- NOTES RECEIVABLE FROM MOBILE HOME PARKS

The notes receivable from mobile home parks (“MHP Notes”) relate to mobile homes sold to mobile home parks and financed through notes receivable. The MHP Notes have varying maturity dates and call for monthly principal and interest payments. The interest rate on the MHP Notes can be fixed or variable. Approximately $82 million of the

13

LEGACY HOUSING CORPORATION NOTES TO CONDENSED FINANCIAL STATEMENTS (UNAUDITED) (dollars in thousands)

MHP Notes have a fixed interest rate ranging from 6.9% to 8.9%. The remaining MHP Notes have a variable rate typically set at 4.0% above prime with a minimum of 8.0%. The average interest rate per loan was approximately 7.7% and 7.7% as of September 30, 2021 and December 31, 2020, respectively, with maturities that range from 1 to 20 years. The collateral underlying the MHP Notes are individual mobile homes which can be repossessed and resold. The MHP Notes are generally guaranteed by the borrowers personally.

The Company had concentrations of MHP Notes with an independent third-party and its affiliates that equaled 29.8% and 52.9% of the principal balance outstanding, all of which was secured by the mobile homes, as of September 30, 2021 and December 31, 2020, respectively.

MHP Notes are stated at amounts due from customers, net of allowance for loan losses. The Company determines the allowance by considering several factors including the aging of the past due balance, the customer’s payment history, and the Company’s previous loss history. The Company establishes an allowance reserve composed of specific and general reserve amounts. There were minimal past due balances on the MHP Notes as of September 30, 2021 and December 31, 2020 and no charge offs were recorded for MHP Notes during the three and nine months ended September 30, 2021 and 2020, respectively. Allowance for loan loss is considered immaterial and accordingly no loss is recorded against the MHP Notes as of September 30, 2021 and December 31, 2020.

- OTHER NOTES RECEIVABLE

Other notes receivable relate to various notes issued to mobile home park owners and dealers, which are not directly tied to sales of mobile homes. The other notes have varying maturity dates and call for monthly principal and interest payments. The other notes are collateralized by mortgages on real estate, units being financed and used as offices, as well as vehicles, and are typically guaranteed by the borrowers personally. The interest rate on the other notes are fixed and range from 6.25% to 12.00%. The Company reserves for estimated losses on the other notes based on current economic conditions that may affect the borrower’s ability to pay, the borrower’s financial strength, and historical loss experience.

The balance outstanding on the other notes receivable were as follows:

| As of | As of | |||||||

| September 30, | December 31, | |||||||

| 2021 | 2020 | |||||||

| Outstanding principal balance | $ | 34,544 | $ | 15,179 | ||||

| Allowance for loan losses | (74) | (75) | ||||||

| Total | $ | 34,470 | $ | 15,104 | ||||

| 5. INVENTORIES | ||||||||

| Inventories consists of the following: | ||||||||

| As of | As of | |||||||

| September 30, | December 31, | |||||||

| 2021 | 2020 | |||||||

| Raw materials | $ | 16,398 | $ | 12,713 | ||||

| Work in progress | 339 | 412 | ||||||

| Finished goods (1) | 24,207 | 23,375 | ||||||

| Allowance for obsolescence | (469) | (620) | ||||||

| Total | $ | 40,475 | $ | 35,880 | ||||

- Finished goods includes $3,524 and $8,656 as of September 30, 2021 and December 31, 2020, respectively, is held for more than twelve months and classified as long-term.

14

LEGACY HOUSING CORPORATION NOTES TO CONDENSED FINANCIAL STATEMENTS (UNAUDITED) (dollars in thousands)

- PROPERTY, PLANT AND EQUIPMENT

Property, plant and equipment consists of the following:

| As of | As of | |||||||

| September 30, | December 31, | |||||||

| 2021 | 2020 | |||||||

| Land | $ | 14,850 | $ | 12,968 | ||||

| Buildings and leasehold improvements | 13,037 | 10,700 | ||||||

| Vehicles | 1,682 | 1,664 | ||||||

| Machinery and equipment | 4,486 | 4,127 | ||||||

| Furniture and fixtures | 298 | 298 | ||||||

| Total | 34,353 | 29,757 | ||||||

| Less accumulated depreciation | (7,925) | (7,141) | ||||||

| Total property, plant and equipment | $ | 26,428 | $ | 22,616 | ||||

Depreciation expense was $403 with $113 included as a component of cost of product sales for the three months ended September 30, 2021 and $249 with $88 included as a component of cost of product sales for the three months ended September 30, 2020. Depreciation expense was $784 with $327 included as a component of cost of product sales for the nine months ended September 30, 2021 and $750 with $267 included as a component of cost of product sales for the nine months ended September 30, 2020.

- OTHER ASSETS

Other assets consists of the following:

| As of September 30, | As of December 31, | ||||

| 2021 | 2020 | ||||

| Leased property, net of accumulated depreciation | $ | 9,909 | $ | 7,218 | |

| Prepaid rent | 255 | 274 | |||

| Repossessed homes | 698 | 1,395 | |||

| Total | $ | 10,862 | $ | 8,887 | |

Depreciation expense for the leased property was $143 and $53 for the three months ended September 30, 2021 and 2020, respectively, and $373 and $124 for the nine months ended September 30, 2021 and 2020, respectively.

- ACCRUED LIABILITIES

Accrued liabilities consists of the following:

| As of | As of | ||||||||

| September 30, | December 31, | ||||||||

| 2021 | 2020 | ||||||||

| Warranty liability | $ | 2,494 | $ | 2,594 | |||||

| Litigation reserve | 607 | 899 | |||||||

| Federal and state income taxes payable | 5,353 | 5,603 | |||||||

| Accrued expenses & other accrued liabilities | 8,619 | 6,394 | |||||||

| Total | $ | 17,073 | $ | 15,490 | |||||

| 15 | |||||||||

LEGACY HOUSING CORPORATION NOTES TO CONDENSED FINANCIAL STATEMENTS (UNAUDITED) (dollars in thousands)

- DEBT Lines of Credit

Revolver 1

At December 31, 2019, the Company had a revolving line of credit (“Revolver 1”) with Capital One, N.A. with a maximum credit limit of $45,000 and a maturity date of May 11, 2020. On March 30, 2020, the Company entered into an agreement with Capital One, N.A. to replace Revolver 1 with a new revolving line of credit (“New Revolver”). The New Revolver has a maximum credit limit of $70,000 and a maturity date of March 30, 2024. For the period January 1, 2020 through March 30, 2020, Revolver 1 accrued interest at one-month LIBOR plus 2.40%. Amounts available under Revolver 1 were subject to a formula based on eligible consumer loans and MHP Notes and were secured by all accounts receivable, consumer loans and MHP Notes.

The New Revolver accrues interest at one-month LIBOR plus 2.00%. The interest rate in effect as of September 30, 2021 and December 31, 2020 was 2.14% and 2.15%, respectively. As with Revolver 1, amounts available under the New Revolver are subject to a formula based on eligible consumer loans and MHP Notes and are secured by all accounts receivable, consumer loans and MHP Notes. The New Revolver requires the Company to comply with certain quarterly financial and non-financial covenants. The amount of available credit under the New Revolver was $61,719 and $33,826 as of September 30, 2021 and December 31, 2020, respectively. In connection with the New Revolver, we paid certain arrangement fees and other fees of approximately $300, which were capitalized as deferred debt issuance costs and will be amortized to interest expense over the life of the New Revolver.

For the three months ended September 30, 2021 and 2020, interest expense under the Capital One Revolvers was $318 and $239, respectively. For the nine months ended September 30, 2021 and 2020, interest expense under the Capital One Revolvers was $827 and $785, respectively. The outstanding balance as of September 30, 2021 and December 31, 2020 was $8,281 and $36,174, respectively.

Revolver 2

In April 2016, the Company entered into an agreement with Veritex Community Bank to secure an additional revolving line of credit of $15,000 (“Revolver 2”). On May 12, 2017, the Company entered into an agreement to increase the line of credit to $20,000. On October 15, 2018, Revolver 2 was amended to extend the maturity date from April 4, 2019 to April 4, 2021. Revolver 2 accrues interest at one month LIBOR plus 2.50% and all unpaid principal and interest is due at maturity on April 4, 2021. Revolver 2 is secured by all finished goods inventory excluding repossessed homes. Revolver 2 requires the Company to comply with certain quarterly financial and non-financial covenants. Amounts available under Revolver 2 are subject to a formula based on eligible inventory. The interest rate in effect as of March 31, 2020 was 4.17%. The amount of available credit under Revolver 2 was $12,028 at March 31, 2020. For the three and nine months ended September 30, 2020 interest expense was $0 and $17. In April 2020, this note was paid in full and the facility was terminated.

PPP Loan

On April 10, 2020, the Company entered into a loan with Peoples Bank as the lender in an aggregate principal amount of $6,546 (the “PPP Loan”) pursuant to the Paycheck Protection Program under the Coronavirus Aid, Relief, and Economic Security Act. The PPP Loan was evidenced by a promissory note dated April 10, 2020 and had a maturity date of April 10, 2022. The PPP Loan had an interest rate of 1.00% per annum, with the first six months of interest deferred. Principal and interest were payable monthly commencing on November 10, 2020 and could be prepaid by the Company at any time prior to maturity with no prepayment penalties. On May 1, 2020, this loan was paid in full.

16

LEGACY HOUSING CORPORATION NOTES TO CONDENSED FINANCIAL STATEMENTS (UNAUDITED) (dollars in thousands)

PILOT Agreement

In December 2016, the Company entered into a Payment in Lieu of Taxes (“PILOT”) agreement commonly offered in Georgia by local community development programs to encourage industry development. The net effect of the PILOT agreement is to provide the Company with incentives through the abatement of local, city and county property taxes and to provide financing for improvements to the Company’s Georgia plant (the “Project”). In connection with the PILOT agreement, the Putman County Development Authority provides a credit facility for up to $10,000, which can be drawn upon to fund Project improvements and capital expenditures as defined in the agreement. If funds are drawn, the Company would pay transaction costs and debt service payments. The PILOT agreement requires interest payments of

6.00% per annum on outstanding balances, which are due each December 1st through maturity on December 1, 2021, at which time all unpaid principal and interest are due. The PILOT agreement is collateralized by the assets of the Project. As of September 30, 2021 and December 31, 2020, the Company had not drawn on this credit facility.

- SHARE-BASED COMPENSATION

Pursuant to the Legacy Housing Corporation 2018 Incentive Compensation Plan (the “Compensation Plan”), the Company may issue up to 10.0 million equity awards to employees, directors, consultants and nonemployee service providers in the form of stock options, stock and stock appreciation rights. Stock options may be granted with a contractual life of up to ten years. At September 30, 2021, the Company had 9.7 million shares available for grant under the Compensation Plan.

In February 2019, the Company granted 120,000 restricted shares of its common stock to members of senior management. The shares were granted on February 7, 2019 and had a grant date fair value of $1,636. The shares vest at a rate of 14.3% annually, beginning on February 7, 2019, and becoming fully vested on February 7, 2025. During the second quarter of 2020, 42,857 of these restricted shares were forfeited due to the departure of a member of senior management.

In February 2019, the Company granted 2,936 restricted shares of its common stock to the independent directors on the Company’s Board of Directors. The shares were granted on February 7, 2019 and had a grant date fair value of $40. The shares became fully vested on December 13, 2019.

In August 2019, the Company granted 39,526 restricted shares of its common stock to a member of senior management. The shares were granted on August 2, 2019 and had a grant date fair value of $496. The shares vest at a rate of 20.0% annually, beginning on August 2, 2020, becoming fully vested on August 2, 2024. This grant was canceled during the second quarter of 2020 due to the departure of the member of senior management.

In March 2020, the Company granted 1,903 restricted shares of its common stock to the independent directors on the Company’s Board of Directors. The shares were granted on March 27, 2020 and had a grant date fair value of $18. The shares became fully vested on December 13, 2020.

In December 2020, the Company granted 2,022 restricted shares of its common stock to the independent directors on the Company’s Board of Directors. The shares were granted on December 2, 2020 and had a grant date fair value of $30. The shares become fully vested on October 4, 2021.

17

LEGACY HOUSING CORPORATION NOTES TO CONDENSED FINANCIAL STATEMENTS (UNAUDITED) (dollars in thousands)

The following is a summary of restricted stock units (the “RSU”) activity (in thousands, except per unit data):

| Weighted | ||||

| Average | ||||

| Grant | ||||

| Date Fair | ||||

| Number | Value Per | |||

| of Units | Unit | |||

| Nonvested, January 1, 2021 | 45 | $ | 13.68 | |

| Granted | – | $ | – | |

| Vested | (9) | $ | 13.63 | |

| Nonvested, September 30, 2021 | 36 | $ | 13.70 | |

As of September 30, 2021, approximately 36,000 RSUs remained unvested. Unrecognized compensation expense related to these RSUs at September 30, 2021 was $392 and is expected to be recognized over 3.36 years.

The Company granted 58,694 incentive stock options to a member of senior management. The options were granted on February 7, 2019 at an exercise price of $13.63 per share. The options vest at a rate of 12.5% annually, beginning on February 7, 2019, and becoming fully vested on February 7, 2026. All options expire ten years after the date of grant. Weighted-average assumptions used in the Black-Scholes option pricing model for stock options granted were as follows: risk free interest rate of 2.41%; dividend yield of 0.00%; expected volatility of common stock of 65.0% and expected life of options of 7.9 years. During the second quarter of 2020, these options were forfeited due to the departure of the senior manager.

The Company granted 34,626 incentive stock options to a member of senior management. The options were granted on August 10, 2020 at an exercise price of $14.44 per share. The options vest at a rate of 20.0% annually, beginning on August 10, 2021, and becoming fully vested on August 10, 2025. All options expire ten years after the date of grant. Weighted-average assumptions used in the Black-Scholes option pricing model for stock options granted were as follows: risk free interest rate of 0.24%; dividend yield of 0.00%; expected volatility of common stock of 75.0% and expected life of options of 6.5 years.

The Company granted 55,490 incentive stock options to a member of management. The options were granted on September 23, 2021 at an exercise price of $18.02 per share. The options vest at a rate of 10.0% annually, beginning on September 23, 2022, and becoming fully vested on September 23, 2031. All options expire ten years after the date of grant. Weighted-average assumptions used in the Black-Scholes option pricing model for stock options granted were as follows: risk free interest rate of 1.41%; dividend yield of 0.00%; expected volatility of common stock of 75.0% and expected life of options of 7.8 years.

The following is a summary of option activity (in thousands, except per unit data):

| Weighted | ||||||||||||

| Average | ||||||||||||

| Weighted | Grant | Weighted | ||||||||||

| Average | Date | Average | ||||||||||

| Exercise | Fair | Remaining | Aggregate | |||||||||

| Number | Price Per | Value | Contractual | Intrinsic | ||||||||

| of Units | Unit | Per Unit | Life | Value | ||||||||

| Outstanding, January 1, 2021, nonvested | 35 | $ | 14.44 | $ | 8.67 | 8.86 | ||||||

| Granted | 55 | $ | 18.02 | $ | 14.07 | 9.98 | ||||||

| Exercised | (7) | $ | 14.44 | $ | 8.67 | — | ||||||

| Outstanding, September 30, 2021, nonvested | 83 | $ | 16.83 | $ | 12.27 | 9.61 | $ | 98 | ||||

| Exercisable, September 30, 2021 | — | $ | — | $ | — | — | $ | — | ||||

18

LEGACY HOUSING CORPORATION NOTES TO CONDENSED FINANCIAL STATEMENTS (UNAUDITED) (dollars in thousands)

As of September 30, 2021, approximately 83,000 options remained nonvested. Unrecognized compensation expense related to these options at September 30, 2021 was $1,011 and is expected to be recognized over 9.98 years.

On March 31, 2020, the Company filed a registration statement on Form S-8 to register with the SEC approximately 2.3 million shares of Legacy common stock available for issuance under the 2018 Incentive Compensation Plan. The registration statement became effective upon filing.

- INCOME TAXES

The provision for income tax expense for the nine months ended September 30, 2021 and 2020 was $7,581 and $8,097, respectively. The effective tax rate for the nine months ended September 30, 2021 was 17.3% and differs from the federal statutory rate of 21% primarily due to a federal tax credit for energy efficient construction and partially offset by state income taxes. The effective tax rate for the nine months ended September 30, 2020 was 22.7% and differs from the federal statutory rate of 21% due to state income taxes.

- COMMITMENTS AND CONTINGENCIES

As of January 1, 2020, the Company instituted a self-insured health benefits plan with a stop-loss policy, which provides medical benefits to employees electing coverage under the plan. The Company estimates and records costs for incurred but not reported medical claims and claim development. This reserve is based on historical experience and other assumptions, some of which are subjective. The Company will adjust its self-insured medical benefits reserve based on actual experience, estimated costs and changes to assumptions. At September 30, 2021 and December 31, 2020, the Company accrued a $323 and $110, respectively, liability for incurred but not reported claims.

The Company is contingently liable under terms of repurchase agreements with financial institutions providing inventory financing for independent retailers of its products. These arrangements, which are customary in the industry, provide for the repurchase of products sold to retailers in the event of default by the retailer. The Company’s obligation under these repurchase agreements ceases upon the purchase of the home by the retail customer. The maximum amount for which the Company was liable under such agreements totaled $5,292 and $2,967 at September 30, 2021 and December 31, 2020, respectively, without reduction for the resale value of the homes. The Company considers its obligations on current contracts to be insignificant and accordingly have not recorded any reserve for repurchase commitment as of September 30, 2021 or December 31, 2020.

Leases. The Company leases facilities under operating leases that typically have 10-year terms. These leases usually offer the Company a right of first refusal that affords the Company the option to purchase the leased premises under certain terms in the event the landlord attempts to sell the leased premises to a third party. Rent expense was $140 and $135 for the three months ended September 30, 2021, and 2020, respectively, and $436 and $423 for the nine months ended September 30, 2021, and 2020, respectively. The Company also subleases properties to third parties, ranging from 3-year to 11-year terms with various renewal options. Rental income from the subleased property was approximately $82 and $90 for the three months ended September 30, 2021 and 2020, respectively, and $263 and $264 for the nine months ended September 30, 2021 and 2020, respectively.

19

LEGACY HOUSING CORPORATION NOTES TO CONDENSED FINANCIAL STATEMENTS (UNAUDITED) (dollars in thousands)

Future minimum lease commitments under all non-cancelable operating leases for each of the next five years at

September 30, 2021, are as follows:

| 2021 | $ | 124 | ||

| 2022 | 490 | |||

| 2023 | 481 | |||

| 2024 | 371 | |||

| 2025 | 335 | |||

| Thereafter | 665 | |||

| Total | $ | 2,466 | ||

Legal Matters

The Company is party to certain legal proceedings that arise in the ordinary course and are incidental to its business. Certain of the claims pending against the Company in these proceedings allege, among other things, breach of contract and warranty, product liability and personal injury. Although litigation is inherently uncertain, based on past experience and the information currently available, management does not believe that the currently pending and threatened litigation or claims will have a material adverse effect on the Company’s financial position, liquidity or results of operations. However, future events or circumstances currently unknown to management will determine whether the resolution of pending or threatened litigation or claims will ultimately have a material effect on the Company’s financial position, liquidity or results of operations in any future reporting periods.

- DERIVATIVE FINANCIAL INSTRUMENTS AND FAIR VALUE MEASUREMENTS Derivative Financial Instruments

On February 2, 2012, the Company entered into a master interest rate swap agreement. The Company elected not to designate the interest rate swap agreements as cash flow hedges and, therefore, gains or losses on the agreements as well as the other offsetting gains or losses on the hedged items attributable to the hedged risk are recognized in current earnings. ASC 815-10, Derivatives and Hedging, requires derivative instruments to be measured at fair value and recorded in the statements of financial position as either assets or liabilities. The Company entered into interest rate swap agreement with Capital One Bank on June 12, 2017 to fix the variable rate portion for $8,000 of the line of credit. This interest rate swap agreement matured on May 11, 2020. Included in the statements of operations for the nine months ended September 30, 2020 is a loss of $15 which was the result of the change in the fair value of the interest rate swap agreement.

Fair Value Measurements

The Company accounts for its investments and derivative instruments in accordance with ASC 820-10, Fair Value Measurement, which among other things provides the framework for measuring fair value. That framework provides a fair value hierarchy that prioritizes the inputs to valuation techniques used to measure fair value. The hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (Level I measurement) and the lowest priority to unobservable inputs (Level III measurements). The three levels of fair value hierarchy under ASC 820-10, Fair Value Measurement, are as follows:

Level I Quoted prices are available in active markets for identical assets or liabilities that the reporting entity has the ability to access at the measurement date.

Level II Significant observable inputs other than quoted prices in active markets for which inputs to the valuation methodology include: (1) Quoted prices for similar assets or liabilities in active markets;

- Quoted prices for identical or similar assets or liabilities in inactive markets; (3) Inputs other than quoted prices that are observable; (4) Inputs that are derived principally from or corroborated

20

LEGACY HOUSING CORPORATION NOTES TO CONDENSED FINANCIAL STATEMENTS (UNAUDITED) (dollars in thousands)

by observable market data by correlation or other means. If the asset or liability has a specified (contractual) term, the Level II input must be observable for substantially the full term of the asset or liability.

Level III Significant unobservable inputs that reflect an entity’s own assumptions that market participants would use in pricing the assets or liabilities.

The asset or liability fair value measurement level within the fair value hierarchy is based on the lowest level of any input that is significant to the fair value measurement.

The Company has used derivatives to manage risks related to interest rate movements. The Company does not enter into derivative contracts for speculative purposes. Interest rate swap contracts are recognized as assets or liabilities on the balance sheets and are measured at fair value. The fair value was calculated and provided by the lender, a Level II valuation technique. Management reviewed the fair values for the instruments as provided by the lender and determined the related asset and liability to be an accurate estimate of future gains and losses to the Company. The Company is not a party to any interest rate swaps as of September 30, 2021.

Fair Value of Financial Instruments

The Company’s financial instruments consist primarily of cash and cash equivalents, accounts receivable, consumer loans, MHP Notes, other note receivables, accounts payable, lines of credit, notes payable, and dealer portion of consumer loans.

The carrying amounts of cash and cash equivalents, accounts receivable, and accounts payable approximate their respective fair values because of the short-term maturities or expected settlement dates of these instruments. This is considered a Level I valuation technique. The lines of credit, notes payable, part of the MHP Notes and part of the other note receivables have variable interest rates that reflect market rates and their fair value approximates their carrying value. This is considered a Level II valuation technique. The Company also assessed the fair value of the consumer loans receivable, the fixed rate MHP Notes and the portion of other note receivables with fixed rates based on the discounted value of the remaining principal and interest cash flows. The Company determined that the fair value of the consumer loan portfolio was approximately $123,000 compared to the book value of $121,637 as of September 30, 2021, and a fair value of approximately $115,000 compared to the book value of $111,920 as of December 31, 2020. The Company determined that the fair value of the fixed rate MHP Notes was approximately $81,000 compared to the book value of $82,118 as of September 30, 2021, and a fair value of approximately $108,000 compared to the book value of $109,806 as of December 31, 2020. The Company determined that the fair value of the other notes was approximately $33,859 compared to the book value of $34,066 as of September 30, 2021, and a fair value of approximately $15,000 compared to the book value of $15,104 as of December 31, 2020. This is a Level III valuation technique.

21

LEGACY HOUSING CORPORATION NOTES TO CONDENSED FINANCIAL STATEMENTS (UNAUDITED) (dollars in thousands)

- EARNINGS PER SHARE

Basic earnings per common share (“EPS”) is computed based on the weighted-average number of common shares outstanding during each reporting period. Diluted EPS is based on the weighted-average number of common shares outstanding plus the number of additional shares that would have been outstanding had the dilutive common shares been issued. The following table reconciles the numerators and denominators used in the computations of both basic and diluted EPS.

| Three months ended | Nine months ended | ||||||||||

| September 30, | September 30, | ||||||||||