Skyline Champion Quarter Ending 7.1.2023 Results – CEO Yost – ‘Navigating Current Environment-Shifts in Demand’ Net Income Falls 56% – 1Q Fiscal 2024 Results; ‘Project Hat Trick’-Facts and Analysis

Oxford Languages defines the phrase “hat trick” as “three successes of the same kind, especially consecutive ones within a limited period.” What Skyline Champion referred to internally as “Project Hat Trick” will be revealed in Part II of this report and analysis. That noted, there are several valid questions that ought to be raised by prior and recent claims made by Skyline Champion (SKY) and its leadership in their remarks to shareholders and stakeholders. Quarterly reports are by their nature packed with facts. This report by Skyline Champion was issued prior to their remarks made as a result of their announced deal with ECN Capital to establish a ‘captive’ finance company with Triad Financial Services (TFS). Those remarks and more are linked from Part II of this report, analysis and expert commentary. Part I of this report was released to the media and public by Skyline Champion via Business Wire, a Berkshire Hathaway (BRK) owned brand. Berkshire Hathaway also owns Clayton Homes, 21st Mortgage Corporation, and Vanderbilt Mortgage and Finance (VMF) companies. It is worth noting that Berkshire recently revealed their increased investments into conventional housing production.

Skyline Champion Announces First Quarter Fiscal 2024 Results

August 01, 2023

TROY, Mich.–(BUSINESS WIRE)– Skyline Champion Corporation (NYSE: SKY) (“Skyline Champion”) today announced financial results for its first quarter ended July 1, 2023 (“fiscal 2024”).

First Quarter Fiscal 2024 Highlights (compared to First Quarter Fiscal 2023)

Net sales decreased 36.0% to $464.8 million

U.S. homes sold decreased 29.3% to 4,817

Total backlog decreased 15.7% to $260 million from the sequential fourth quarter

Average selling price (“ASP”) per U.S. home sold decreased 8.2% to $89,000

Gross profit margin contracted by 370 basis points to 27.9%

Net income decreased by 56.2% to $51.3 million

Earnings per share (“EPS”) decreased 56.4% to $0.89

Adjusted EBITDA decreased 58.9% to $66.8 million

Adjusted EBITDA margin contracted by 800 basis points to 14.4%

Net cash generated by operating activities of $74.9 million during the quarter

“Skyline Champion’s results for the first quarter of fiscal 2024 met expectations, reflecting continued execution on our operational initiatives as we navigate the current environment and shifts in demand” said Mark Yost, Skyline Champion’s President, and Chief Executive Officer. “On a sequential basis we are seeing orders increase and backlogs return to historically normal levels, while managing production to align with current demand trends. Skyline Champion continues to drive our strategic initiatives to transform homebuilding, generating value for shareholders now and in years to come.”

First Quarter Fiscal 2024 Results

Net sales for the first quarter fiscal 2024 decreased 36.0% to $464.8 million compared to the prior-year period. The number of U.S. homes sold in the first quarter fiscal 2024 decreased 29.3% to 4,817. Volume levels during the quarter were adversely impacted by the timing of community orders and the absence of FEMA-related sales which totaled $82.5 million in the first quarter of last year. The ASP per U.S. home sold decreased 8.2% to $89,000 due to the impact of product mix and the decrease in material surcharges. The number of Canadian factory-built homes sold in the quarter decreased to 221 homes compared to 352 homes in the prior-year period due to softening demand in certain markets.

Gross profit decreased by 43.5% to $129.7 million in the first quarter fiscal 2024 compared to the prior-year period. Gross profit margin was 27.9% of net sales, a 370-basis point contraction compared to 31.6% in the first quarter fiscal 2023. Gross margin contraction is being driven by lower volumes and changes in product mix including the absence of FEMA unit sales versus last year’s first quarter. Improvements in operational capabilities helped maintain the margin profile on a sequential basis despite lower production rates and consumer shifts to smaller less optioned homes.

Selling, general, and administrative expenses (“SG&A”) in the first quarter fiscal 2024 decreased to $70.4 million from $72.3 million in the same period last year. SG&A as a percentage of net sales was 15.2%, compared to 10.0% in the prior year period. SG&A during the quarter reflects lower sales volumes and variable compensation, partially offset by expenses related to acquisitions closed in fiscal 2023 and investments in new capacity.

Net income decreased by 56.2% to $51.3 million for the first quarter fiscal 2024 compared to the prior-year period. The decrease in net income was driven by lower sales in the quarter.

Adjusted EBITDA for the first quarter fiscal 2024 decreased by 58.9% to $66.8 million compared to the first quarter fiscal 2023. Adjusted EBITDA margin for the quarter was 14.4%, compared to 22.4% in the prior-year period.

As of July 1, 2023, Skyline Champion had $797.7 million of cash and cash equivalents, an increase of $50.3 million in the current quarter.

Conference Call and Webcast Information:

Skyline Champion management will host a conference call tomorrow, August 2, 2023, at 9:00 a.m. Eastern Time, to discuss Skyline Champion’s financial results and an update on current operations.

Investors and other interested parties can listen to a webcast of the live conference call by logging onto the Investor Relations section of Skyline Champion’s website at skylinechampion.com. The online replay will be available on the same website immediately following the call.

The conference call can also be accessed by dialing (877) 407-4018 (domestic) or (201) 689-8471 (international). A telephonic replay will be available approximately two hours after the call by dialing (844) 512-2921, or for international callers, (412) 317-6671. The passcode for the live call and the replay is 13739924. The replay will be available until 11:59 P.M. Eastern Time on August 16, 2023.

About Skyline Champion Corporation:

Skyline Champion Corporation (NYSE: SKY) is a leading producer of factory-built housing in North America and employs approximately 7,600 people. With more than 70 years of homebuilding experience and 44 manufacturing facilities throughout the United States and western Canada, Skyline Champion is well positioned with an innovative portfolio of manufactured and modular homes, ADUs, park-models and modular buildings for the single-family, multi-family, and hospitality sectors.

In addition to its core home building business, Skyline Champion provides construction services to install and set-up factory-built homes, operates a factory-direct retail business with 31 retail locations across the United States, and operates Star Fleet Trucking, providing transportation services to the manufactured housing and other industries from several dispatch locations across the United States.

Skyline Champion builds homes under some of the most well-known brand names in the factory-built housing industry including Skyline Homes, Champion Home Builders, Genesis Homes, Athens Park Models, Dutch Housing, Atlantic Homes, Excel Homes, Homes of Merit, New Era, Redman Homes, ScotBilt Homes, Shore Park, Silvercrest, Titan Homes in the U.S. and Moduline and SRI Homes in western Canada.

Presentation of Non-GAAP Financial Measures

In addition to the results provided in accordance with U.S. generally accepted accounting principles (“U.S. GAAP”) throughout this press release, Skyline Champion has provided non-GAAP financial measures, Adjusted EBITDA and Adjusted EBITDA Margin, which present operating results on a basis adjusted for certain items. Skyline Champion uses these non-GAAP financial measures for business planning purposes and in measuring its performance relative to that of its competitors. Skyline Champion believes that these non-GAAP financial measures are useful financial metrics to assess its operating performance from period-to-period by excluding certain items that Skyline Champion believes are not representative of its core business. These non-GAAP financial measures are not intended to replace, and should not be considered superior to, the presentation of Skyline Champion’s financial results in accordance with U.S. GAAP.

Skyline Champion defines Adjusted EBITDA as net income or loss plus expenses or minus income, (a) the provision for income taxes, (b) interest income or expense, net, (c) depreciation and amortization, (d) gain or loss from discontinued operations, (e) non-cash restructuring charges and impairment of assets, (f) other non-operating income and costs, including but not limited to those costs for the acquisition and integration or disposition of businesses and idle facilities. Adjusted EBITDA is not a measure of earnings calculated in accordance with U.S. GAAP, and should not be considered an alternative to, or more meaningful than, net income or loss, net sales, operating income or earnings per share prepared on a U.S. GAAP basis. Adjusted EBITDA does not purport to represent cash flow provided by, or used in, operating activities as defined by U.S. GAAP. Skyline Champion believes that Adjusted EBITDA is commonly used by investors to evaluate its performance and that of its competitors. However, Skyline Champion’s use of Adjusted EBITDA may vary from that of others in its industry. Adjusted EBITDA is reconciled from the respective measure under U.S. GAAP in the tables below. Adjusted EBITDA Margin is calculated as Adjusted EBITDA divided by net sales reported in the statement of operations.

Forward-Looking Statements

Statements in this press release, including certain statements regarding Skyline Champion’s strategic initiatives, and future market demand are intended to be covered by the safe harbor for “forward-looking statements” provided by the Private Securities Litigation Reform Act of 1995. These forward-looking statements generally can be identified by use of words such as “believe,” “expect,” “future,” “anticipate,” “intend,” “plan,” “foresee,” “may,” “could,” “should,” “will,” “potential,” “continue,” or other similar words or phrases. Similarly, statements that describe objectives, plans, or goals also are forward-looking statements. Such forward-looking statements involve inherent risks and uncertainties, many of which are difficult to predict and are generally beyond the control of Skyline Champion. We caution readers that a number of important factors could cause actual results to differ materially from those expressed in, implied, or projected by such forward-looking statements. Risks and uncertainties include regional, national and international economic, financial, public health and labor conditions, and the following: supply-related issues, including prices and availability of materials; labor-related issues; inflationary pressures in the North American economy; the cyclicality and seasonality of the housing industry and its sensitivity to changes in general economic or other business conditions; demand fluctuations in the housing industry, including as a result of actual or anticipated increases in homeowner borrowing rates; the possible unavailability of additional capital when needed; competition and competitive pressures; changes in consumer preferences for our products or our failure to gauge those preferences; quality problems, including the quality of parts sourced from suppliers and related liability and reputational issues; data security breaches, cybersecurity attacks, and other information technology disruptions; the potential disruption of operations caused by the conversion to new information systems; the extensive regulation affecting the production and sale of factory-built housing and the effects of possible changes in laws with which we must comply; the potential impact of natural disasters on sales and raw material costs; the risks associated with mergers and acquisitions, including integration of operations and information systems; periodic inventory adjustments by, and changes to relationships with, independent retailers; changes in interest and foreign exchange rates; insurance coverage and cost issues; the possibility that all or part of our intangible assets, including goodwill, might become impaired; the possibility that our risk management practices may leave us exposed to unidentified or unanticipated risks; the potential disruption to our business caused by public health issues, such as an epidemic or pandemic, and resulting government actions; and other risks set forth in the “Risk Factors” section, the “Legal Proceedings” section, the “Management’s Discussion and Analysis of Financial Condition and Results of Operations” section, and other sections, as applicable, in our Annual Reports on Form 10-K, including our Annual Report on Form 10-K for the fiscal year ended April 1, 2023 previously filed with the Securities and Exchange Commission (“SEC”), as well as in our Quarterly Reports on Form 10-Q, and Current Reports on Form 8-K, filed with or furnished to the SEC.

If any of these risks or uncertainties materializes or if any of the assumptions underlying such forward-looking statements proves to be incorrect, then the developments and future events concerning Skyline Champion set forth in this press release may differ materially from those expressed or implied by these forward-looking statements. You are cautioned not to place undue reliance on these statements, which speak only as of the date of this release. We anticipate that subsequent events and developments will cause our expectations and beliefs to change. Skyline Champion assumes no obligation to update such forward-looking statements to reflect events or circumstances after the date of this document or to reflect the occurrence of unanticipated events, unless obligated to do so under the federal securities laws.

SKYLINE CHAMPION CORPORATION

CONSOLIDATED BALANCE SHEETS

(Unaudited, dollars and shares in thousands)

July 1,

2023

April 1,

2023

(unaudited)

ASSETS

Current assets:

Cash and cash equivalents

$

797,717

$

747,453

Trade accounts receivable, net

50,678

67,296

Inventories, net

196,510

202,238

Other current assets

34,123

26,479

Total current assets

1,079,028

1,043,466

Long-term assets:

Property, plant, and equipment, net

184,259

177,125

Goodwill

196,574

196,574

Amortizable intangible assets, net

42,383

45,343

Deferred tax assets

18,746

17,422

Other noncurrent assets

96,669

82,794

Total assets

$

1,617,659

$

1,562,724

LIABILITIES AND STOCKHOLDERS’ EQUITY

Current liabilities:

Accounts payable

$

47,218

$

44,702

Other current liabilities

198,726

204,215

Total current liabilities

245,944

248,917

Long-term liabilities:

Long-term debt

12,430

12,430

Deferred tax liabilities

6,305

5,964

Other liabilities

62,059

62,412

Total long-term liabilities

80,794

80,806

Stockholders’ Equity:

Common stock, $0.0277 par value, 115,000 shares authorized, 57,133 and

57,108 shares issued as of July 1, 2023 and April 1, 2023, respectively

1,586

1,585

Additional paid-in capital

524,907

519,479

Retained earnings

775,980

725,672

Accumulated other comprehensive loss

(11,552

)

(13,735

)

Total stockholders’ equity

1,290,921

1,233,001

Total liabilities and stockholders’ equity

$

1,617,659

$

1,562,724

SKYLINE CHAMPION CORPORATION

CONSOLIDATED STATEMENTS OF OPERATIONS

(Unaudited, dollars and shares in thousands, except per share amounts)

Three months ended

July 1,

2023

July 2,

2022

Net sales

$

464,769

$

725,881

Cost of sales

335,096

496,546

Gross profit

129,673

229,335

Selling, general, and administrative expenses

70,439

72,282

Operating income

59,234

157,053

Interest (income) expense, net

(9,301

)

90

Other (income)

—

(634

)

Income before income taxes

68,535

157,597

Income tax expense

17,266

40,446

Net income

$

51,269

$

117,151

Net income per share:

Basic

$

0.90

$

2.06

Diluted

$

0.89

$

2.04

SKYLINE CHAMPION CORPORATION

CONSOLIDATED STATEMENTS OF CASH FLOWS

(Unaudited, dollars in thousand)

Three months ended

July 1,

2023

July 2,

2022

Cash flows from operating activities

Net income

$

51,269

$

117,151

Adjustments to reconcile net income to net cash provided by operating activities:

Depreciation and amortization

7,592

5,616

Amortization of deferred financing fees

69

95

Equity-based compensation

5,428

3,960

Deferred taxes

(997

)

1,685

Loss on disposal of property, plant, and equipment

1

6

Foreign currency transaction (gain) loss

(207

)

351

Change in assets and liabilities:

Accounts receivable

16,676

(38,141

)

Inventories

6,173

(48,855

)

Other assets

(6,974

)

(11,084

)

Accounts payable

1,375

(15,931

)

Accrued expenses and other liabilities

(5,548

)

32,569

Net cash provided by operating activities

74,857

47,422

Cash flows from investing activities

Additions to property, plant, and equipment

(10,341

)

(9,435

)

Investment in floor plan loans

(18,466

)

—

Proceeds from floor plan loans

3,184

—

Acquisitions, net of cash acquired

—

(9,553

)

Proceeds from disposal of property, plant, and equipment

8

17

Net cash used in investing activities

(25,615

)

(18,971

)

Cash flows from financing activities

Changes in floor plan financing, net

—

2,398

Stock option exercises

—

9

Tax payments for equity-based compensation

(961

)

(351

)

Net cash (used in) provided by financing activities

(961

)

2,056

Effect of exchange rate changes on cash and cash equivalents

1,983

(2,142

)

Net increase in cash and cash equivalents

50,264

28,365

Cash and cash equivalents at beginning of period

747,453

435,413

Cash and cash equivalents at end of period

$

797,717

$

463,778

SKYLINE CHAMPION CORPORATION

RECONCILIATION OF NET INCOME TO ADJUSTED EBITDA

(Unaudited, dollars in thousand)

Three Months Ended

July 1,

2023

July 2,

2022

Net income

$

51,269

$

117,151

Income tax expense

17,266

40,446

Interest (income) expense, net

(9,301

)

90

Depreciation and amortization

7,592

5,616

EBITDA

66,826

163,303

Transaction costs

–

338

Other

–

(973

)

Adjusted EBITDA

$

66,826

$

162,668

Part II – Additional Information with More MHProNews Analysis and Commentary

Stating the obvious can be clarifying. Asking the obvious can also be clarifying. Having institutional and professional member is routinely useful for trade media, perhaps most notably for MHProNews.

On 8.28.2023 MHProNews asked Bing’s AI chat function the following question: “What is Skyline Champion Corporation’s (SKY) Project Hat Trick?” Here was the response.

The response given to that same inquiry by the Bing search engine yielded the following as the #1 result on this date and time a report on MHProNews, but candidly that report didn’t mention Skyline Champion’s “Project Hat Trick.” That project – an internal designation by the firm – is attached as a download at this link here. Now the question ought to be asked and answered, why the name, Project Hat Trick? As the Bing AI inquiry reflects, there is at this time no known public response to that question from Skyline officials.

That noted, the following is at least curious. Or it may reflect something more significant.

From the Skyline Champion (SKY) website MHProNews accessed the following file on 8.28.2023 at about 3:55 AM. SKY referred to this investor relations presentation as Project Hat Trick. A hat trick is a term used in ice hockey. “A “hat trick” in hockey occurs when a player scores three goals in a single game,” says TheSportsGround. The FreeDictionary says of the phrase in a non-sports usage that a hat trick is: “An extremely clever or adroit maneuver.” Merriam Webster says: a hat trick is “a series of three victories, successes, or related accomplishments.”

Note: to expand this image to a larger or full size, see the instructions

below the graphic below or click the image and follow the prompts.

In the case of Cavco Industries, detail minded MHProNews readers may recall that Securities and Exchange Commission (SEC) attorneys made it publicly known that during the tenure of that firm’s former executive Joseph “Joe” Stegmayer, they used such colorful names in what the SEC alleged were violations of securities laws and regulations. Cavco and Stegmayer each settled for over a 7-figure dollar amount after protracted negotiations and maneuvers. That doesn’t necessarily imply that this matter is illegal. But it is at lease curious. There was an indication that a whistleblower payout occurred in the Cavco-Stegmayer matter. One Skyline Champion manager was named by the SEC in that case (see first linked report).

That noted, the manufactured home industry is demonstrably underperforming.

So too arguably is Skyline Champion (SKY).

Recent U.S. Census Bureau data reflects that conventional housing at the time of the report linked below was up 20 percent year-over-year (YoY). Meanwhile, manufacutred housing, per the latest data, is down sharply, at a similar rate as Skyline Champion.

As was noted above, Skyline Champion recently closed a deal with ECN Capital to establish a captive finance division in connection with what has long been the largest independent lender in manufactured housing that was not owned by Berkshire, as are 21st and VMF.

There has been a recent change in the handling of certain information by Skyline Champion and others which may or may not be revealed by MHProNews in the near term. That could be part of a future report.

For now, this report’s analysis will mention some additional points, including insights from third parties. In no particular order of importance.

Per Yahoo Finance, the overall trend for Skyline Champion has been lower for much of the past two years. This is odd at best, given the affordable housing crisis and the seemingly positive potential that ought to exist for the manufactured housing industry. See the graphic below.

Investors/the market initially had a favorable response to the deal announced on 8.14.2023 between Skyline Champion – ECN Capital/Triad Financial Services to form a captive finance company. But investors have clearly cooled on the idea.

2. A recent commentary on Skyline Champion by Caffital Research was published on the Seeking Alpha financial news site. It had the following top lines summary.

Summary

Skyline Champion Corporation is facing deteriorating earnings due to a slowdown in the real estate market after an inflated modular home market related to Covid.

Analysts have a moderate upside outlook for the stock, but a discounted cash flow model suggests an estimated fair value of $45.09, indicating a potential downside for SKY stock.

As investors currently have low visibility into Skyline’s future margins and growth, I believe investors should be conservative in evaluating the company.

MHProNews will note the incorrect use of the term “modular” above, given that Skyline Champion has per their own statements. FWIW, Caffital’s analyst referred to in the graphic below. Perhaps the analyst isn’t completely clear that HUD Code means manufactured homes? Whatever the case may be on grasping the terminology and related, the following image was in Caffital’s analysis.

Right or wrong, the analyst via popular Seeking Alpha said the following.

As the company is facing harder times with the slowdown in the real estate market after an inflated modular home market related to Covid, the company’s earnings are beginning to deteriorate. In my opinion the company’s deteriorating earnings aren’t completely priced into the stock, constituting a sell-rating.”

Their analysis also said the following.

As housing prices have soared in recent years, Skyline has seen a great increase in demand in FY22 and FY23 – in FY22 the company’s revenues grew by 55% with a further increase of 18% in FY23. These increases have turned into decreasing revenues in the most recent quarters as consumers’ purchasing power and the real estate market have seen cooldowns – in Q1 of FY24, Skyline’s revenues shrunk by 36%, with similar decreases expected in the coming quarters.”

Skyline has a cash balance of almost $800 million, with outstanding interest-bearing debts of only around $12 million in long-term debt; the company’s balance sheet doesn’t pose any risks to the company’s operations. The company does not currently pay out any dividends, leaving investors wondering where the cash balance is going to be allocated. Skyline’s capital expenditures also seem to be low compared to the company’s market capitalization of around $3.7 billion, as the company’s trailing capital expenditures are only $53.2 million – the cash balance could leave room for sizable M&A activity.”

For the time being, I still have a conservative approach to the valuation. Takeaway

At $64.81 a share, I believe the company’s currently deteriorating bottom line poses a risk for investors. Although Skyline could be a good investment given that the company implements business strategies well, I currently have a sell-rating given my DCF model’s estimated downside of 30%.”

If Caffital Research was alone in this type of down-trend thinking about Skyline Champion, perhaps the firm’s leadership could shrug it off. But the Yahoo Finance graphic above makes it clear that other investors aren’t bullish, they are “bearish” too.

3. Prior MHProNews reports relative to Skyline Champion are linked below.

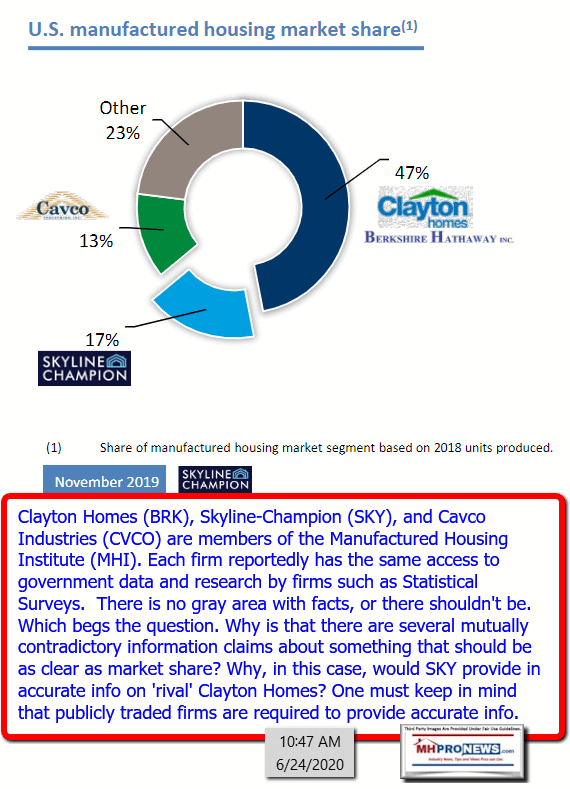

This is a hard statement to defend. Per our sources, Skyline Champion buys this data and should have known that what they published here was wrong. That suggests that for some reason, Skyline-Champion and Clayton have worked to understate Clayton’s market share to the industry, potential investors, and presumably public officials.

There should be significant concerns by manufactured housing political nuance wise investors about Skyline Champion, the industry’s other two “big three” HUD Code home builders and the Manufactured Housing Institute. See the reports linked below for insights.

See the remarks by MHARR’s Danny Ghorbani in the above.

MHProNews’ leadership has a strong belief in the industry true upside potential. However, it seems apparent that the corporate insiders who dominate MHI have something entirely different in mind. What is that difference? They appear to be more focused on steady consolidation rather than on organic growth.

One of the more popular – and arguably important – reports in recent months is the following.

When Caffital Research said: “At $64.81 a share, I believe the company’s currently deteriorating bottom line poses a risk for investors. Although Skyline could be a good investment given that the company implements business strategies well, I currently have a sell-rating given my DCF model’s estimated downside of 30%” haven’t they made some significant remarks that are shared in some way by other investors?

As MHProNews noted last week and previously, there are several possible strategies that a firm like Skyline, or Cavco for that matter, could and should deploy if they were serious about organic corporate and industry growth. But instead, Skyline appears to be deploying a “moat” move. Is it any wonder that several of those contacted for comments about the SKY-Triad deal expressed concerns about it? Recall that one high-level source told MHProNews that the move may ‘chill the market.’ After an initial bump, SKY’s stock has indeed ‘chilled’ or moved lower.

But this isn’t just a concern for investors of Skyline Champion. It ought to be a cautionary flag for independents in manufactured housing too. The fact that MHI’s CEO Lesli Gooch, Ph.D., keeps repeatedly making questionable at best, or possibly corrupt at worst statements and moves on behalf of ‘the industry’ is itself a red flag. Skyline CEO Mark Yost has a seat on the MHI board. There is no known indication that he is concerned about Gooch.

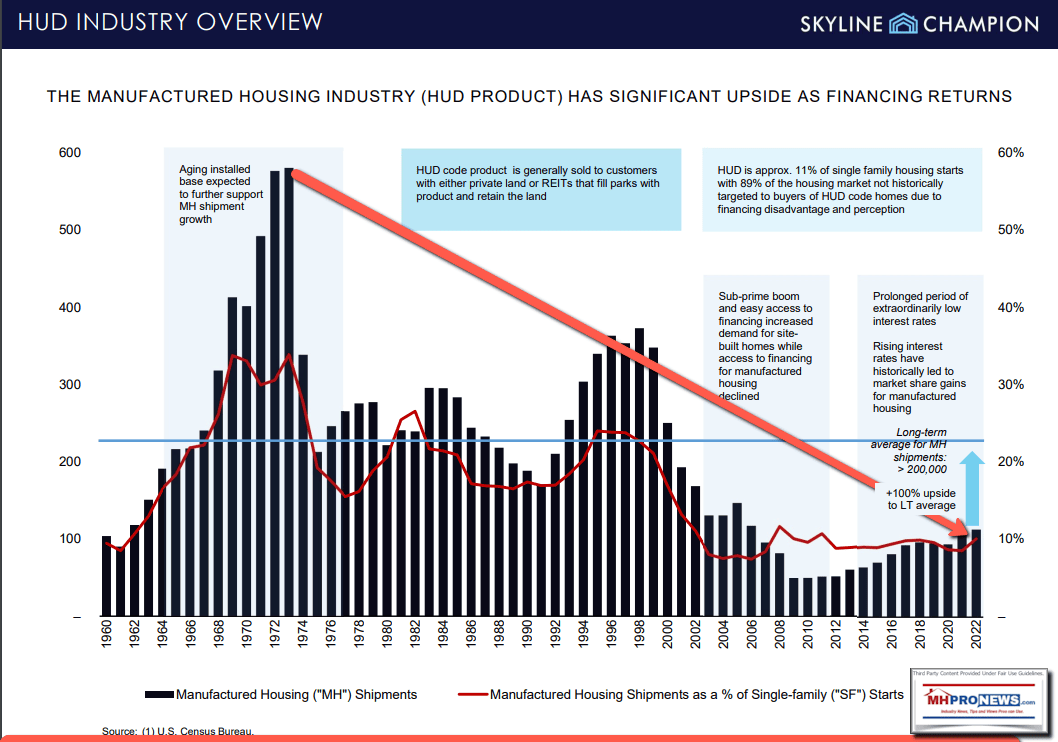

MHProNews’ Masthead shared insights on the industry’s potential in a report linked below. But the graphic that follows, with the base image from a prior Skyline Champion’s IR pitch, also suggests that manufactured housing ought to be performing at a far higher level of production.

Note: to expand this image to a larger or full size, see the instructions

below the graphic below or click the image and follow the prompts.

Trade media can and should be a ‘cheer leader’ when it is appropriate to do so. But authentic trade media also holds the powers that be to account. Who says? The American Press Institute. Click here to subscribe to the most complete and obviously most read manufactured housing industry news in seconds. Enter your desired email address, press submit, confirm in your inbox. Then You’re All Set for x2 weekly emailed news updates! To report a news tip – either ON or OFF the record – click the image above or send an email to iReportMHNewsTips@mhmsm.com – To help us spot your message in our volume of email, please put the words NEWS TIP or COMMENTS in the subject line.

Our son has grown quite a bit since this 12.2019 photo. All on Capitol Hill were welcoming and interested in our manufactured housing industry related concerns. But Congressman Al Green’s office was tremendous in their hospitality. Our son’s hand is on a package that included the Constitution of the United States, bottled water, and other goodies.

Tony earned a journalism scholarship and earned numerous awards in history and in manufactured housing.

For example, he earned the prestigious Lottinville Award in history from the University of Oklahoma, where he studied history and business management. He’s a managing member and co-founder of LifeStyle Factory Homes, LLC, the parent company to MHProNews, and MHLivingNews.com.

This article reflects the LLC’s and/or the writer’s position and may or may not reflect the views of sponsors or supporters.