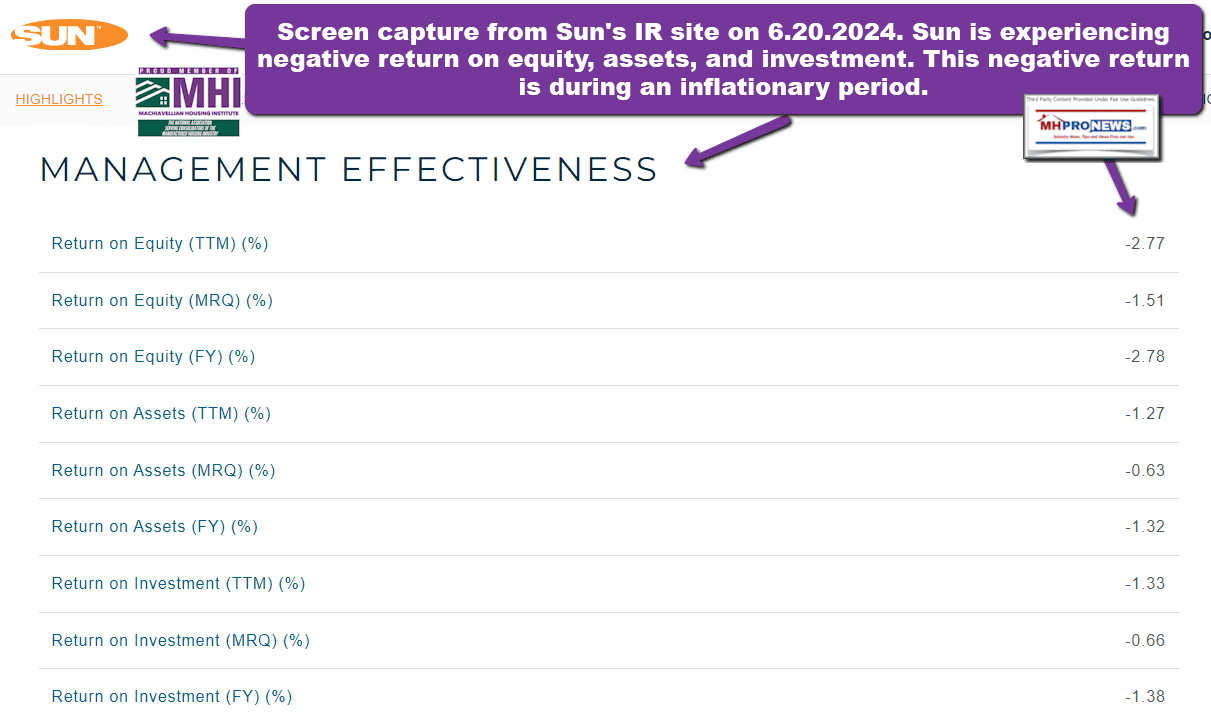

Have the proverbial chickens from years of Sun Communities (SUI) leadership antics finally come home to roost? The latest earnings call transcript, related financials, and their June 2024 Investor Relations (IR) presentations (pitch) all point to substantial areas of concern for the manufactured housing (MH) community owner-operator that over the years branched into the United Kingdom (UK a.k.a. England), recreational vehicle (RV) parks, and marinas. Sun’s leadership team for this earning’s call transcript was listed as: Gary Shiffman, Chairman, President and Chief Executive Officer; and Fernando Castro-Caratini, Chief Financial Officer; and Aaron Weiss, Executive Vice President of Corporate Strategy and Business Development. As regular and detail-mined MHProNews readers know, Shiffman has had his share of what some could call public scandals. After years of boasts, Sun’s management has brought them to the point where their own management effectiveness graphic shows the firm as having negative net profitability. After years of chasing an array of interests that often appear to share the common feature of not having much new developing (i.e.: MHCs, RVs parks and marina slips), Shiffman says below that their “goal [is] to create simplification up and down throughout the company.” Sun has reportedly sold two MHCs and may sell other assets. Per the graphic shown in Part II of today’s report from Yahoo Finance, Sun trails key stock market performance by losing value instead of gaining value during an inflationary period.

Sun is a higher profile Manufactured Housing Institute (MHI) member, has a seat on their board of directors, and they were hit with multiple national class action antitrust suits launched on behalf of residents (see an update on that topic at this link here). While Sun, Equity LifeStyle Properties (ELS), Flagship Communities, “Frank and Dave,” and other higher profile MHI National Communities Council (NCC) members have been proclaiming the supposed glories of very few new developments, their fellow MHI member UMH Properties recently came out with a boldly different statement, with Eugene and Sam Landy stating their vision is for the industry to develop 100,000 new communities in the foreseeable future. For those not familiar with the MHC count in MHVille, it currently stands at about 50,000 properties. MHI, perhaps due to members Datacomp/MHVillage (which are ELS owned), oddly say it is 43,000. Regardless, developing 100,000 new manufactured home communities would mean roughly tripling the current communities’ count in the U.S. Given the affordable housing crisis, there is a logic to having such a goal.

What this report with analysis may reveal is that years of cautionary articles on MHProNews and our MHLivingNews sister site that have included Sun may well be in the process of a sobering reckoning or less than joyous realization for those who put their faith in the arguably negative vision of limiting the industry by artificially limiting production. Manufactured housing production is down roughly 75 percent from its high in 1998. That drop is despite a growing population and evidence from California of how state preemption dramatically boosted Accessory Dwelling Unit (ADU) production. As the Manufactured Housing Association for Regulatory Reform (MHARR) has been arguing for years, two good federal laws needed to grow the industry already exist and need only be pressed into action by MHI. In the wake of facts and evidence, the apparent happy talkers in the MHI-orbit of bloggers and publishers other than MHProNews/MHLivingNews are beginning to look as bent and complicit as the trade group they are a part of.

As MHARR’s President and CEO Mark Weiss, J.D., has credited one of his law professor’s saying: “Facts are stubborn things.”

With all due respect to Weiss and that professor, both of whom likely know this too, it was founding father John Adams who is credited by GoodReads with that pithy insight: “Facts are stubborn things.”

With that preface, let’s dive into the facts per Sun’s most recent transcript in Part I. Along with additional information, MHProNews will begin to unpack those remarks in Part II. Because markets were closed yesterday due to Juneteenth (see the Juneteenth report, linked here), there is no Part III (market recap) today.

Part I

Per Yahoo Finance and Insider Monkey is the following transcript

MHProNews note: highlighting is added by MHProNews, but their transcript is otherwise as shown.

Sun Communities, Inc. (NYSE:SUI) Q1 2024 Earnings Call Transcript

Insider Monkey Transcripts

Wed, May 1, 2024

Sun Communities, Inc. (NYSE:SUI) Q1 2024 Earnings Call Transcript April 30, 2024 …

Operator: Good afternoon, ladies and gentlemen, and thank you for standing by. Welcome to the Sun Communities First Quarter 2024 Earnings Conference Call. At this time, management would like me to inform you that certain statements made during this call, which are not historical facts, may be deemed forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Although, the company believes the expectations reflected in any forward-looking statements are based on reasonable assumptions, the company can provide no assurance that its expectations will be achieved. Factors and risks that cause actual results to differ materially from expectations are detailed in yesterday’s press release and from time-to-time in the company’s periodic filings with the SEC.

This company undertakes no obligation to advise or update any forward-looking statements to reflect events or circumstances after the date of this release. Having said that, I’d like to introduce management with us today. Gary Shiffman, Chairman, President and Chief Executive Officer; and Fernando Castro-Caratini, Chief Financial Officer; and Aaron Weiss, Executive Vice President of Corporate Strategy and Business Development. After their remarks, there will be an opportunity to ask questions. [Operator Instructions] As a reminder, this call is being recorded. I would now like to turn the conference call over to your host, Gary Shiffman, Chairman, President and Chief Executive Officer. Mr. Shiffman, you may begin.

Gary Shiffman: Good afternoon, and thank you for joining us on our conference call to discuss first quarter 2024 earnings and our updated guidance. We’re pleased to report solid first quarter results underpinned by strong operational performance in each of our businesses. Core FFO per share of $1.19 for the quarter was driven by robust 7.9% year-over-year growth in North American same-property NOI and strong UK same-property NOI growth. Our first quarter results underscore how the favorable dynamics of high demand and limited supply, inherent in our best-in-class portfolio generate resilient real property income. Same-property manufactured housing NOI increased 8% compared to the first quarter of 2023 due to several factors, including rental rate increases, occupancy growth and lower expenses.

Same-property RV NOI increased 8.1%, primarily reflecting the positive impact of converting transient sites to annual leases, and continued expense savings that partially offset lower transient revenues. Same-property Marina NOI grew 7.5% compared to the prior year. The outperformance was driven by continued strong demand for wet slips and dry storage as well as strong rental rate increases. As we enter our third full year of ownership of our UK portfolio, this segment is now included in our same-property reporting. UK same-property NOI in the quarter was approximately $11 million, which is a strong start to the year. We remain focused on our capital recycling strategy. And as disclosed on our last earnings call, have sold two manufactured housing properties.

Currently, we have in the market with additional assets and feel positive about our ability to transact. In terms of capital deployment, Sun continues to be highly selective. Year-to-date, Sun has acquired several bolt-on Marina properties for approximately $12 million that strategically enhance our Marina member network on the East Coast. We recently published our sixth annual ESG report. Key highlights include completing our inventory methodology for reporting Scopes 1, 2 and 3 greenhouse gas emissions and a 73% increase in team member volunteer hours compared to 2022. Additionally, we continue to prioritize our dialogue and interactions with our stakeholders and to work with our supply chain partners to understand their ESG programs. We continue to execute on a plan, focused on delivering earnings growth from a reliable real property income.

I would like to thank our talented team members for their continued dedication and strong performance and all our stakeholders for their continued support. I will now turn the call over to Fernando to discuss our results and guidance in more detail. Fernando?

Fernando Castro-Caratini: Thank you, Gary. In the first quarter, Sun reported core FFO per diluted share of $1.19, driven by strong real property revenue growth and our continued focus on managing expenses. In North America, total same-property NOI for the quarter grew 7.9%, driven by a 6% increase in revenues and a 2.2% increase in expenses, further detailing each segment. Same-property manufactured housing reported another solid quarter with an 8% increase in NOI compared to 2023. The NOI was driven by a 6.8% increase in revenue and expense growth of 3.4%. For same-property RV, its 8.1% NOI growth was driven by a 3.1% increase in revenue and a 1.8% decrease in expenses. The year-over-year decline in RV operating expenses was due to aligning controllable costs with transient revenues, notably in payroll and utilities.

Occupancy for same-property manufactured housing and RV, adjusted to include expansion activity, increased 180 basis points year-over-year to 98.9%. Part of the uplift in occupancy can be attributed to conversions of transient to annual RV sites. For the trailing 12 months ended March 31, 2024, Sun converted over 1,750 transient sites to annual contracts, accounting for approximately 65% of our revenue-producing site gains. We are continuing our strategic focus on converting transient to annual sites. Since the start of 2020, we have completed nearly 7,100 conversions and have increased the number of annual sites by approximately 27%. Marina’s posted another strong quarter with same property NOI increasing 7.5% compared to 2023. This was driven mainly by rate increases for wet slips and dry storage spaces across the portfolio and stronger transient demand, resulting in a 7.1% increase in revenue, partially offset by a 6.5% increase in expenses, primarily driven by payroll.

In the U.K. same property NOI increased by $3.3 million, representing a 44.5% increase over 2023 same-property results, higher rental rates increased customer retention and the early timing of the Easter holiday break drove a 12.3% increase in revenue in the quarter. Property operating expenses decreased 1.7% year-over-year primarily reflecting timing differences for supply and repair and payroll costs. First quarter U.K. home sales volumes were in line with expectations. We sold more than 620 homes representing a 5.4% increase compared to the previous year. FFO contribution was $10.2 million for the quarter, reflecting the strong sales volume, offset in part by lower margins. The strong unit sales performance in the first quarter will lead to an increase in community occupancy and site rent for the year.

This aligns with our strategic objective to shift a larger share of our U.K. business activity from home sales to real property rents. Regarding capital allocation, Sun remains extremely disciplined, pursuing limited strategic opportunities. As Gary indicated, we recycled approximately $52 million of proceeds from selling two assets this year and acquired four highly strategic Marinas for approximately $12 million. Turning to our balance sheet. On March 31, 2024, the company had approximately $7.8 billion in net debt outstanding and our net debt to trailing 12-month recurring EBITDA ratio was 6.1x. We remain focused on further enhancing our balance sheet strength. During the quarter, Sun issued $500 million of five-year senior unsecured notes with an interest rate of 5.5%.

Net proceeds were used to pay down borrowings outstanding under our senior credit facility. During the quarter, we also paid off our corporate term loan with our revolving credit facility. Our weighted average debt maturity is 6.8 years, and our variable rate debt was approximately 11% at the end of the quarter. We intend to use free cash flow from operations and proceeds from planned asset sales to reduce overall leverage and variable rate debt percentages. As detailed in yesterday’s release, we are updating our 2024 guidance for first quarter results as follows: we narrowed our full year core FFO per share guidance to a range of $7.06 to $7.22. We are also establishing guidance for the second quarter of 2024 core FFO per share in the range of $1.83 to $1.91.

For our total portfolio, we expect real property NOI growth in the range of 6.5% to 7.3%. Higher expected NOI growth in MH and Marinas should offset lower expected NOI from RV. In North America, the updated full year same property growth range is 4.6% to 5.8%. The 40 basis point reduction at the midpoint is primarily due to transient RV revenue headwinds. Revised expectations are 6.2% to 7.1% for manufactured housing, a 15 basis point increase at the midpoint, negative 0.3% to 1.3% for RVs, a 230 basis point decrease at the midpoint driven by transient RV revenue headwinds, which we are partially offsetting with controllable expense reductions and 6.4% to 7.6% for Marinas, a 20 basis point increase at the midpoint. In the UK, we forecast approximately the same total FFO contribution for the year, but with a greater contribution now expected to come from real property results.

We are increasing our full year same property NOI forecast from the prior range of 1.3% to 3.3% to a new range of 6% to 8%. The increase is driven by greater expected rental revenues, complemented by continued cost management efforts. The higher real property revenue outlook is a function of the previously implemented rental rate increases and higher home sales volume and retention achieved year-to-date. For UK home sales, we maintain our range of expected volume for the year but expect lower FFO contribution due to lower margins. Our UK strategy remains focused on shifting a larger proportion of our income from home sales margins into the resilient reliable NOI generated by real property rents. Overall, we are pleased with our operating performance, expense management and minimizing capital spending over the course of this year.

Please refer to our supplemental for additional guidance information. As a reminder, our guidance includes acquisitions and dispositions and capital markets activity through April 29, but it does not include the impact of prospective acquisitions, dispositions or capital markets activities, which may be included in research analyst estimates. This concludes our prepared remarks. We will now open the call up for questions. Operator?

Q&A Session

Operator: Thank you. At this time, we will be conducting a question-and-answer session. [Operator Instructions] Our first question comes from Michael Goldsmith with UBS. Please proceed with your question.

Michael Goldsmith: Good afternoon. Thanks for taking my question. It seems like you guys have been able to convert the strategy for — in the UK from generating the bulk of the — or you’ve been able to convert from generating a lot of the NOI from home sales and you’ve made progress on generating it more from rent growth like. How are you able to achieve that in such a short period of time that it kind of influenced the guidance in such a large way? Thank you.

Gary Shiffman: Thanks for the question, Michael. The UK business overall is performing, generally, in line with expectations. There has been a strategy that — you mentioned that we’ve indicated from the time we acquired the acquisition that we look to sacrifice a little bit of the margin on home sales to be able to create a more sticky dependable real property income in the form of pitch fees there. And it is working very, very well in first quarter. I think is a good example of it. That being said, there are still economic pressures and headwinds in the UK. While we’re up in volume and overall growth. U.K. very much like what we’re seeing in the U.S. is probably not seeing the benefits of interest rate reductions as soon as they might have been anticipated a while ago.

So the bottom line is, I think that we’d be in a position to be even excelling further, and we expect to be doing so as we go through the year and into the future. And we’ll continue to sacrifice a little bit of that margin to gain the real property revenue. It’s been working so far, and we expect it to continue to do so.

Michael Goldsmith: Thanks for that Gary. And my follow-up question is, there were several moving pieces in the 2024 expectations, and that came two months after issuing your initial outlook two months ago. So as we look forward from here, do you sit here and think, okay, now we’ve got a much better grasp on the year sitting in the middle of spring. And so there shouldn’t be as much volatility with the guidance going forward? Or at this point in the year, could there still be kind of large shifts within the expectations going forward? I’m just trying to gain a better understanding of where the visibility is into the year at this point?

Gary Shiffman: It’s certainly a question we can relate to and understand, as we move forward to a very focused plan on taking the underpinning and the incredible performance, if you will, of our business platform and translating it into growth for our shareholders. We’re working very, very hard on a number of different areas that we’ve shared previously, certainly, the simplification, the recycling of capital, and many of the things that we’ve accomplished over the last couple of quarters. All in an effort, and this includes the continued conversions of transient, where it is harder to forecast out transient RV into annual agreements in our RV communities. All this and the approach that we’ve taken to looking hard at first quarter and knowing that it’s the lowest contributor across the Board first and fourth quarters to our overall FFO performance.

We feel comfortable with the adjustments that we made will leave us in the best position to really deliver the results that we’re sharing with you today.

Fernando Castro-Caratini : And Michael, while they’re certainly are moving pieces to the guidance, we did reiterate our FFO guidance per share with the second quarter.

Michael Goldsmith: Thank you very much.

Operator: Our next question comes from John Kim with BMO Capital Markets. Please proceed with your question.

John Kim: Thank you. Just wanted to follow-up on the FFO guidance, which you maintained, but when you look at the non-same-store real property items, it looks like a $0.15 reduction in your outlook. Part of that is higher G&A, but that’s another question. But how confident are you to make — that you can make up that $0.15 or 2% of FFO in your same-store portfolio?

Fernando Castro-Caratini : John, the G&A move upward from guide to guide. That’s from a GAAP perspective. So that does not include some add backs that we have for FFO, mainly deal costs and transaction costs, of which there were just over $11 million in the quarter. The transaction expenses related to finalizing the receivership process related to the Royale Life note and investor engagement during the first quarter. So while there is — on the guidance page, there is an increase from guide to guide in G&A. Our net of those add-backs, we are still expecting at the midpoint our G&A to grow by about 4.6%, again at the midpoint.

John Kim: And the other items, I mean, maybe my second question is your RV guidance was the only part that went down on your same-property outlook, you had 8% growth in the first quarter. So you’re basically implying it’s going to go negative for the rest of the year. I realize that the transient to seasonal or annual conversion, but typically you get a big uplift in revenue when you make that conversion. So, what is driving that reduction in the same-property RV outlook?

Fernando Castro-Caratini: And John, you’re seeing the uplift of that occupancy gain on the annual side, with just over 13% growth for that line item in the first quarter. The movement or the guide downward on the RV side is primarily due to the transient headwinds as mentioned earlier, where we will look to offset as much of it as possible by — with controllable expense, cost reductions. The — our forecast set in February for our guidance implied a 2.6% reduction in transient revenue for the year. That is — that was including the impact of conversions as mentioned that is currently, with all the information that we have in front of us as it relates to pace, shorter booking windows that is currently expected to be about 8%, reduction for the year. So that is the largest mover on the RV side. Overall, when you take that into consideration with our manufactured housing platform and Marina platform, the guide downward on the NOI side is about $4 million.

Q – John Kim: Okay. Thank you.

Operator: Our next question comes from Josh Dennerlein with Bank of America. Please proceed with your question.

Q – Josh Dennerlein: Hi, guys. Thanks for the question. Maybe just wanted to touch on the asset sales and just like how that marketing process is going?

Gary Shiffman: Well, Josh, we certainly got off to a good start and shared the two assets that we did sell. We are currently in the market. And there are a number of opportunities that we feel very good, within the selected assets that we offer for dispositions. Again, these are assets that we feel will benefit somebody else in the long run. And there are still buyers out there. There are those that are looking to build platforms, and looking past the negative leverage, if you will. But there is definitely, a shift in the marketplace with debt costs being higher than they had been for the last long period of time. We look forward to being able to share with everybody the results, of these dispositions that we have in the market right now. And hopefully, we’ll be able to do that in this coming quarter.

Q – Josh Dennerlein: I appreciate that, Gary. And then I just wanted to follow up on Michael’s question, about the guidance. When I think about your guides, it almost seems like every line item the range was revised. Just maybe stepping back and thinking big picture, how do you — like what’s your philosophy on providing these guidance ranges.

Fernando Castro-Caratini: We’re looking to provide as much disclosure as possible to the market, as it relates to all of the — all of our business platforms and other line items. So you can — with the guidance, you can track almost entirely P&L. We did add guidance in February, as it related to expected interest expense which had not been provided previously. So that is that’s looking to provide as much color as possible to the market, as it relates to our expectations, those expectations some shift upwards some shift downwards, as you’re seeing with the guidance provided last night. But it’s the best information that we have in front of us today to provide to you and the rest of the market.

Gary Shiffman: Josh the only thing that I would add to that is the fact that we certainly got through a lot of challenges in 2023 have had some headwinds in 2024 as we’ve shared with everybody. But I’ve also shared a strong desire to be simplifying and assisting with the ability to model. So, we continue to do a lot of work on that. And as we go through 2024, some of the steps that are taking place I think will put us in a cadence be able to provide an understanding and information as we go forward. A good example is U.K. home sales where we will sacrifice the margin and made a decision and management is actually executing on the decision to increase volume at the cost of a little bit of margin to add to real property income. They’ve done an outstanding job at Park Holidays. We really want to commend them on that. And it’s things like that that are causing adjustments. But I think as we continue quarter-by-quarter, we’ll take a cadence that will feel much better.

Josh Dennerlein: Okay. Appreciate the color.

Operator: Our next question comes from Brad Heffern with RBC Capital Markets. Please proceed with your question.

Brad Heffern: Yes, thanks. Is there any color that you can give about the pace at which you expect to move NOI out of the U.K. home sales business and into real property going forward? Should we continue to see sort of big chunky moves like this as the year goes on? Or does the guidance kind of fully reflect the underlying change in strategy?

Fernando Castro-Caratini: The guidance fully reflects the underlying change — or not a change in strategy, but the continuation of that strategy of shifting more right more income into the reliable real property side.

Brad Heffern: Okay. And is there any color you can give on kind of the pace at which we should expect that to happen? Obviously in the U.S. home sales are not a big contributor. Is there visibility on that happening in the U.K. over the next five years or three years? Or any sort of framework you can give us around the speed at which you can accomplish the transition?

Gary Shiffman: Brad are we talking about the U.K.?

Brad Heffern: Yes, for the U.K.

Gary Shiffman: Again I’d kind of reiterate what Fernando said in the fact that even going back to when we announced the acquisition we had a strategy recognizing that the model in the U.K. is different than it is in the U.S. And we would sacrifice margin for increase in occupancy and gaining that more sticky dependable if you will and modelable is such a word FFO on the real property side. So, what you’re seeing is a continuation on that. We — in 2023, definitely hit headwinds of a slowing economy that caused that to accelerate faster than our five or seven-year plan originally had it. But I would say right now where we’re at we’re right on target where we want them to be with Park Holidays. And I think you’ll just continue to see us hit guidance and if things should improve or if we have an opportunity to make more rapid we would definitely share that in the future.

Operator: Our next question comes from Wes Golladay with Robert W. Baird. Please proceed with your question.

Wes Golladay: Hello, everyone. I just want to go back to the transient forecast. Can you unpack that a little bit? What has driving the EBITDA adjusted for the conversions? Are you seeing any rate pressure? And then when you have your forecast for the balance of the year, are you extrapolating the current trends into the balance of the year?

Gary Shiffman: Wes we continue to believe in the long-term strength of the overall RV sector. And as you know, we’ve been strategically reducing our transient exposure, and relative contribution over the past few years in favor of the stability of the growth of the annual agreements that we’re really, really focused on. So we’ve increased the annuals by about 27% by converting the transient since 2020 and our expectation and our outlook moving forward, if you’ll continue to see that. And again, that allows us to budget and forecast with a higher degree of confidence, as we have those homes in on an annual basis. And they’re not subject to the concerns of whether again much of the transient is within a three-hour drive of the home base of our guests.

And so weather conditions as we saw in April. And as we’ve seen more recently in the last couple of years, do impact that short-term transient guest stability, to be able to forecast it. So I think that, while it’s a good business. And we will continue to have a percentage of it. We will continue to focus on converting those transient over to annuals. And we’re seeing stronger-and-stronger demand and we’re opening up more-and-more of our transient sites and will allow them to be converted to annual.

Wes Golladay: Yeah. No. I get all that. Just maybe looking at the transient forecast, so it did come down about 6% — 5% or 6%. And I’m just wondering if there’s a rate pressure or is it just occupancy? And is it mainly just the current trends that you’re seeing, and are you extrapolating that into the second half of your forecast? Just trying to get a sense of maybe how conservative the guide is maybe a little too conservative as weather potentially impacting the guide at the moment?

Gary Shiffman: Yeah. I would just suggest as Fernando mentioned, certainly pace has a lot to do with it. We’re seeing it 8% down year-over-year. There is concept that says the shorting booking windows will yield, the potential for upside, but in our efforts to give the best guidance that we can going forward. We’re looking at outpacing is right now. I don’t know, if Fernando, of you have anything to add.

Wes Golladay: Okay. And then maybe going to the UK is there any onetime items that hit the first quarter and then anything in the forward guidance? And maybe just can you confirm that there’s the price is lowering, the pricing to build those, sticky income on the real property that’s nothing new that you changed this year year-to-date is something that you’ve been doing all along.

Gary Shiffman: Yeah. I’ll answer the first part and Fernando, can talk about guiding forward. But the strategy of shifting margin for occupancy gain has been our strategy all along. As I indicated before it more rapidly accelerated in 2023, as we brought margins down due to the headwinds of the economy. But what you’re seeing right now is continued strong demand for the Park Holidays community. And a management team that from day one, understood the concept of being able to increase occupancy and increase real property contribution over the concept of the one-time sales margin, that probably worked much better for them as the portfolio was owned by private equity firms in the past. So it’s pretty much it exactly where we want it to be now .Sand we’re hoping to continue it and really make a difference in how we’re going to look long-term at the value creation if you will of the real property contribution.

Fernando Castro-Caratini: And then, Wes, on aggregate the total FFO contribution from Park Holidays for 2024 is in line with original expectations. Park Holidays contribution to core FFO also includes SRD&E through retail and F&B operations and head office personnel and corporate activities on the G&A side. In the first quarter and for the year, included in the overall contribution to core FFO was an expected payroll tax withholding, that refund and third-party costs related to securing this refund. These various items had a net impact of about $2 million to our aggregate $153 million of core FFO in the first quarter or much larger for the rest of the year. These changes are similar and consistent with call it it’s akin to real estate tax or sales tax or other expense changes that are periodically reflected, updated treatment of revenue or expense. These changes are sometimes favorable or unfavorable to the current period.

Wes Golladay: Okay. And so just the bottom line that is a contract expense you had. And so the UK real property revenue is just a true upward lift in on the full year?

Fernando Castro-Caratini: Yeah. It was on same property is — and that is detailed during the call is primarily driven by the higher rental rates, higher retention than expected and we did see a stronger Easter break, which also the comp on a year-over-year basis where Easter was during the second quarter in 2023.

Wes Golladay: Got it. Thanks for the time everyone.

Operator: Our next question comes from Keegan Carl with Wolfe Research. Please proceed with your question.

Keegan Carl: Yes. Thanks for the time guys. Maybe first, I guess just on your acquisition of the land parcels. It was a bit surprising given your comments on development and expansion last quarter. So I guess I’m just curious what changed on this front?

Gary Shiffman: Yeah. I think we’ve talked about being very, very strategic in our thinking with use of capital. And we’ve also shared the plan that we’re looking to both recycle capital and dispositions, as well as through cash flow by shutting down development and using that cap will pay down more costly debt on a rate basis. I think that when you have 500 to 600 properties that are very, very strategically located and the strategic piece of land or opportunity comes about, we take advantage of that, thinking about the long-term nature of Sun. And all you’re seeing there is as you saw in the Marinas. There are just some bolt-on opportunities where we have a very, very low cost, a great deal of potential value creation in the future and those are just one-off strategic opportunities small in nature.

Keegan Carl: And then shifting gears here on home sales, I guess both in the US and UK, maybe UK first. I know you mentioned margin. Is it just a function of mix? Like are you selling more used homes to new homes? Or is it just lower general pricing. Is there any update on Sandy Bay as well as those are higher priced homes? And then in the US, I know that outlook was reduced too. Is it explicitly tied to existing home sales? Or is there something else we should be aware of?

Fernando Castro-Caratini: Keegan on the UK side that’s a mix of both of pricing and mix shifting more towards the pre-owned side of sales. Sandy Bay is ramping up well as it relates to marketing efforts for sales, heading into a busier season over the course of the next couple of months.

Gary Shiffman: Yeah. On the US home side, Keegan, really given the high occupancy of which our MH properties operate and our strategic shift away from deploying capital into that development and expansion. We did guide towards much lower home sales this particular year. And that is something I think that just demonstrates a little bit of the strength that we’re seeing at nearly 98% occupancy in the MH and annual communities.

Keegan Carl: Great. Thanks for the time guys.

Operator: Our next question is from Eric Wolfe with Citibank. Please proceed with your question.

Eric Wolfe: Hey, thanks. As you look at your guidance, I was just wondering if there’s anything in the core numbers that is sort of onetime in nature one way or the other. So, for instance, it seems like there might have been a tax refund in the UK same-store NOI this quarter. Just trying to understand if there’s anything in this year’s core FFO that won’t be repeated next year, as we think about the right sort of base from which to project things in 2025.

Fernando Castro-Caratini: Eric, has detailed a little bit earlier in the quarter and budgeted this way contribution in the UK, included a VAT refund on the real property side. It included additional expenses or higher expenses, given payroll tax withholding and costs associated with securing that refund. The net of those figures is about $2 million for the quarter or for the year. But consistent with this is akin to say, real estate tax assessments right where we may pay, a little bit more given the assessment that we get from the state. And if there’s — if we are able to work through that assessment, we might be at a refund in a later period. It’s similar and consistent with that practice.

Eric Wolfe: Yes, that makes sense. I guess, I was just trying to make sure there was nothing else. I mean so it sounds like just net, like maybe $2 million and understood, on the reason for it I just want to make sure that when we’re projecting out to 2025 there’s nothing else that would sort of distort those numbers. I guess second question, on the recurring CapEx. It looks a little bit high relative to last year’s quarterly average. Just wondering, if we should expect it to come down? And then also I saw that there’s a decrease in sort of acquisition CapEx, but still a bit of this sort of bolt-on investment to former acquisitions. I guess, when should we expect that to come down as well? Thanks.

Fernando Castro-Caratini: Thank you, Eric. The spend on the recurring CapEx side is consistent, and we do have higher CapEx — recurring CapEx on the Marina side and on the UK side, during the first quarter of the year. So that spend is expected to moderate over the rest of the year, as it relates to total nonrecurring CapEx for the quarter, it does represent about a 45% reduction as compared to the first quarter of last year. And is expected to ramp up, as we’ve discussed with the market, our spend on CapEx is expected to be somewhere around 55% reduction to the figures that you saw spend in 2023.

Eric Wolfe: Got it. Thank you.

Operator: Our next question comes from Anthony Powell with Barclays. Please proceed with your question.

Q – Anthony Powell: Hi, good afternoon. I guess another question on transient RV. I understand that you’re trying to convert many of those sites to annual, but you still have a meaningful amount of transient sites. So I’m curious, are there any trends that you can employ to maybe improve growth there? And what’s your optimal annual transient split in that business?

Gary Shiffman: I think answering the second part of your question first. We talked about reducing transient from high 20,000s to about 14,000 15,000 over a three- four- five-year period of time, transient sites to be our best in transient properties as well as the feeder to continue to feed annual RV guests as they move out. So we’re making good, good progress there. And with regard to other opportunities, I think on the social media side, on the marketing side, we’ve been very, very focused. I think that there’s been a lot of talk about the incredible growth through COVID and the return to pre-COVID periods of time. We’re really just focused if you will, growing from where we are and we have engaged a number of third parties who have hospitality experience looking at different forms of revenue management, different forms of looking for business activity in the shorter parts of the week in the shorter seasons.

So we’re very, very focused. And I do believe that there is opportunity than near to long-term to really enhance the transient pool of properties and sites that we have. We’re also what is left in the portfolio becomes the best of the best of the transient. So there’s an opportunity, as well as we continue to convert to see longer to mid-term improvements in growth than we’re seeing right now. But there’s nothing specific that I could point to that would tell you that it’s leading directly to an anticipated change.

Anthony Powell: Okay. Thank you.

Operator: Our next question is from Jamie Feldman with Wells Fargo. Please proceed with your question.

Jamie Feldman: Great. Thank you, and thanks for taking my question. I guess, just focusing on the balance sheet. Can you just remind us your deleveraging or leverage objectives and floating rate debt objectives in terms of those metrics? And can you also give us some thoughts on the glide path to get there? What do you think it takes to get to your goal? And how long do you think it takes to get to your goals for both of those items?

Fernando Castro-Caratini: Sure Jamie. As we’ve stated previously, our long-term leverage targets are to be at 5.5 times and below. Today we are at 6.1 times from a leverage perspective. Growth in EBITDA over the course of the year should provide deleveraging by the end of the year, as well as Gary had stated before, we have multiple opportunities from a capital recycling standpoint that we trust, we’ll update the market with over the course of the next couple of months and quarters that should also contribute towards reaching and surpassing that goal of 5.5 times. Floating rate debt today as of the end of the quarter was just above 11%, we will look to manage that percentage to be below 10%. So that’s something that we can do here over the course of the short-term.

Jamie Feldman: Okay. And just to confirm the 5.5, you’re saying by year-end? Or no that’s going to take much longer?

Fernando Castro-Caratini: That takes us into 2025 from that standpoint.

Jamie Feldman: Okay. And then I guess just taking a step back over the last nine months, year, a lot of new initiatives at the company. You added two new Board members. You took the plan to simplify earnings. I think whether it was NAREIT meetings in November or end of year conference call discussions, it seemed like you had ring-fenced a lot of the concerns on the UK and some of the problems that certainly the market was concerned about. So you look today you guys maintained your guidance. Your core business actually seems a little bit better than expected when we started the year, but the stock is underperforming by almost 600 basis points to REITs. Can you just talk about maybe looking behind the curtain of what’s going on at the company and some of the initiatives that your Board is debating, your management team is debating, your company is debating about ways to address the problem, fix the problem.

Just maybe things that we on this side of the fence don’t necessarily have a view on that people can look forward to as they think about this company and what’s to come the year ahead.

Gary Shiffman: Sure. I think I’d share and really reiterate the thoughts related specifically to that, which the goal to create simplification up and down throughout the company. The company has grown a lot, complexities certainly crept in. And as we’ve discussed previously, we’re really making good progress along those lines. With regard to the Board, we’re pleased with the addition of the new Board members. We’re pleased with the setup of the committees going forward. We’re doing well through our disposition program and recycling that capital. We’ve talked about one of the JVs that we’ve been able to simplify greatly that we shared the Northgate properties last quarter. We’ve talked about stepping out of the headstock in Australia.

And we’ve sold off our interest in the proprietary software for managing our RV communities. Although, we still use it great software Campspot. And at the same time the conversions that are taking place that we’ve spent a lot of time talking about today and other days, allow us to manage our business much better to bring the cost margins are greater in the annual properties than they are in the transient properties which will translate to future growth as well. I think that the strategy that is working well in the UK right now with regard to moving more of the volatile home sales margin into real property income. The fact that we’ve been able to get through the foreclosure process on the assets in the UK and have Park Holidays, manage them.

In particular the great job they’re doing at Sandy Bay. We’re excited to share the results of how things are shaping up over there. So these are all the things that the Board. And the managed team — our management team are focused on. It also gives me the opportunity to mention that, we have Aaron Weiss, sitting in on our call today we brought in, two years ago. So as an effort to broaden our executive team and our bench, I think that we’re really excited to be able to demonstrate how the simplification and approach to everything is going to translate into FFO growth as Sun has been known for it historically. But of course, we realize that we have a ways to go to demonstrate it through 2024, gain some of that lost credibility back. And we’re working very, very hard and very, very diligently to do so.

And I think it’s just underpinned by the really outstanding performance of the business platform. And we continue to work hard and share more of that information quarter-by-quarter with you.

Jamie Feldman: Thank you, Gary. This is very helpful and lots to think about. I guess just one quick follow-up if you don’t mind, just because we get asked this a lot. I mean how long does it take for whatever initiatives even if all the initiatives you’ve put in place at year-end or all the initiatives you’re going to do? Like, how long does it really take for it to have the full impact?

Gary Shiffman: Well, I’m going to suggest what we talked about at NAREIT and some of the conferences in our calls that 2024 isn’t without its headwinds. We talked a lot about the specific financial headwinds and the simplification paths that were taking place. Our real goal is to look at 2025 when most of these headwinds that we can identify are behind us and we can really, really begin to translate the very strong core business growth into growth to our shareholders. So while there is upside and there is a risk to everything as we go through the year we all know it’s still a challenged economy with a lot of uncertainty in there. As far as what we can control in the company, we feel like we’ll be in a very, very good position finishing out 2024 and going into 2025.

Jamie Feldman: Okay. Great. Thank you. Appreciate your thoughts.

Operator: Our next question is from Anthony Hau with Truist Securities. Please proceed with your question.

Anthony Hau: Good afternoon guys. Thanks for taking my questions. Given that you brought sales margin down in the U.K. are you seeing more buyers homeowners buying premium lodges compared to before? And what percentage of buyers are buying standard versus premium today?

Fernando Castro-Caratini: Anthony, our — we have brought margin expectations down for the year by about $2600 that is helping drive more pre-owned lodge sales that premiumization or those upgrade sales is something that we will continue to work with our customers that have bought a pre-owned home over the course of the last couple of years and are looking to upgrade. So that is part of the strategy as it relates to that higher retention that we’ve been discussing as it relates to our homeowners across the portfolio.

Anthony Hau: And when you upgrade a home from like standard to premium you increased your pitch fee by three times, right?

Fernando Castro-Caratini: It’s going to depend Anthony on the size of that home and that site and where that site is in the portfolio. But yes, there is usually a premiumization not just from the sale of the home but also on the pitch fee side.

Anthony Hau: Okay. And just one quick question about revenue for using sites gain. I think the initial guidance assumed 2400 to 2700 site gains, has the underlying assumption for this metric change for the current guidance? And how confident are you to achieve this target, given that only 233 sites were gained in the first quarter?

Fernando Castro-Caratini: Anthony, no change to the expectations for the full year as it relates to the revenue-producing site gains across manufactured housing and RV for the year.

Anthony Hau: Okay. Thank you.

Operator: Our next question comes from John Pawlowski with Green Street. Please proceed with your question.

John Pawlowski: Thanks for the time. I have two questions on the RV business. One just a clarifying question on the comments made. So is it that the 8% shortfall in reservation pace is that revenues for the second quarter and third quarter are trending 8% below a year ago? Is that just a number of reservations. Could you just be more specific on that stat?

Fernando Castro-Caratini: Sure, John. The 8% number that I quoted is expected year-over-year decline in revenue growth for the full year. Currently as it relates to the second quarter we are expecting about an 8.6% decline in revenue year-over-year.

John Pawlowski: Okay. And then can you give me some on-the-ground details of what’s going on with consumer demand right now? Which regions are you seeing the most pronounced softness? Is it – or is it a property-type divergence for highly amenitized resorts are suffering? Is it camping? Can you just help me understand what your local teams are seeing so we have a sense of consumer price sensitivity right now?

Gary Shiffman: John, generally it’s been pretty much across the Board with just a slower pace. So we’re guiding a bit based on that year-over-year pacing if you will. Second quarter has been quiet. We’re approaching the seasonal communities that are opening up April, May and a little bit of weather issue impacts us a little bit if it did through the months but it is mostly just the pacing across the Board. So there’s no one thing that we can point to and we don’t want to put an expectation of outperformance there. But certainly, we’ll see if shorter and closer to normal visitations that the bookings don’t pick up a little bit. And – but for that we really don’t have anything to point to. We’d suggest we asked that question all the time of our management team.

There is a return to a lot of other forms of vacation as we all know taking place out there across the Board. But we will keep you posted as to any other specific change that we would see. So there’s nothing I could point to regionally or within a segment of our communities.

John Pawlowski: Okay. Final question from me. Fernando, the $0.14 you’re adding back in transaction costs and nonrecurring G&A, it’s not too far off from what the cost the magnitude of costs added back and in ’23 and ’22 during much more acquisitive years. And so, outside of Royale Life what else is in this specifically? What else is in this number? And I imagine Royale Life was known at the start of the year. So again what drove the $0.07 incremental add-back guide versus guide?

Fernando Castro-Caratini: Sure. So, it would be the activity that we saw in the first quarter that is largely driving that increase on a guide to guide basis. As we’ve shared with the market during February, we expected about $9.5 million of add-backs over the course of the year. We did surpass that in the first quarter and are now projecting that just above $18 million related to. As mentioned earlier, primarily these are debt deal costs of transactions that we have been underwriting. And we’ll walk away from or have walked away from the transaction costs as detailed earlier as well. We do have implementation expenses for our technology platforms that we amortize over a period of time and it’s the amount that we’ve spent to develop those technologies and implement them.

But at this time, that add back for the full year is expected to be $18.4 million as detailed in yesterday’s press release. So it would — that’s about $7 million of additional over the course of the rest of the year, but that can change.

John Pawlowski: All right. Thank you.

Operator: We have reached the end of the question-and-answer session. I’d now like to turn the call over to Chairman, President and CEO, Gary Shiffman for closing remarks.

Gary Shiffman: Thank you everybody. We just want to end and letting everyone know we are very, very focused on the concept of understanding closing the gap in valuation and we are working very, very hard with everything we do to move forward on that and I look forward to speaking to everybody on the next quarterly call. Thank you, operator.

Operator: You’re welcome. This concludes today’s conference. You may disconnect your lines at this time and we thank you for your participation. Goodbye. ##

Part II – Additional Information with More MHProNews Analysis and Commentary

In no particular order of importance are the following facts from Sun Communities (SUI) and other sources as cited. Analysis and commentary will be woven in in what follows.

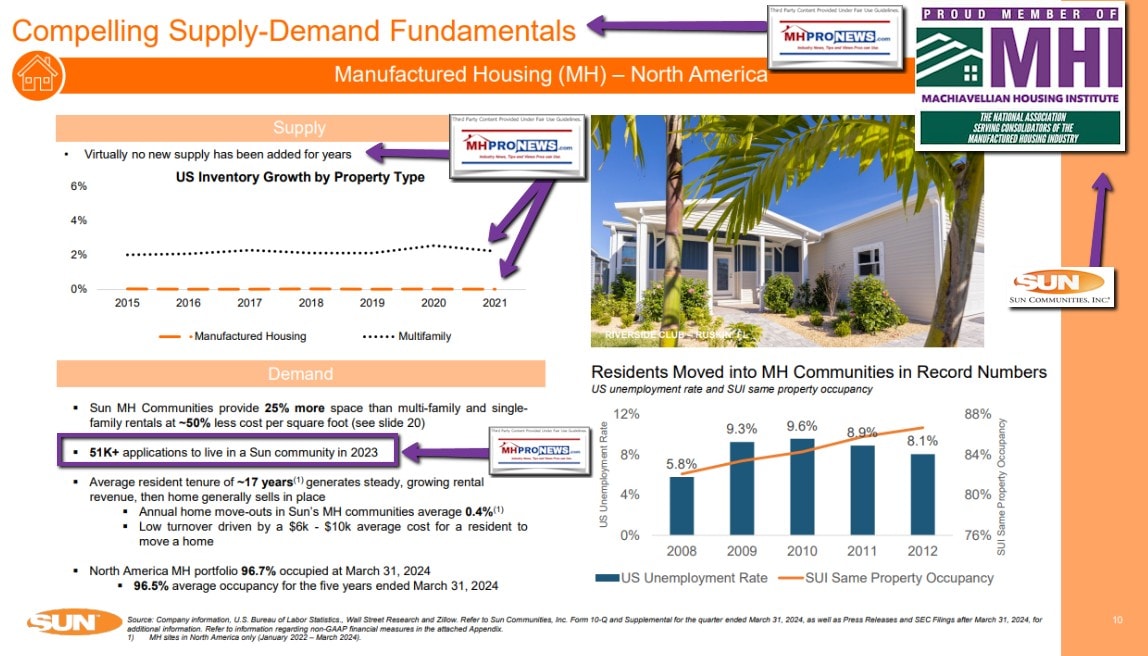

1) Established in 1975, Sun Communities became a publicly owned corporation in December, 1993. Per RV Business: “The company (Sun) purchased its first RV resort in 1996 in Florida and its first northern camping resort in Michigan in 2011.” Left-leaning Wikipedia says: “In September 2020, the company acquired Safe Harbor Marinas for $2.11 billion. On Nov. 16, 2021, Sun RV Resorts Rebrands to Sun Outdoors.” UK Parks said: “Park Holidays UK, has been acquired by US real estate investment trust Sun Communities, Inc. (“Sun”). The £950 million acquisition was agreed in November 2021, and closed this month (April) following approval from the Financial Conduct Authority.” Despite all those varied acquisitions, per their own data, the largest segment of the company is still its land-lease manufactured home community (MHC) portfolio.

2) According to Yahoo Finance summaries pre-dawn on 6.20.2024 are the following insights. Note the negative value growth for Sun year-to-date (YTD), for 1 year, and for 3 years vs. the general S&P 500 market performance.

In several devices the image below can be opened to a larger size.

In many cases you can click the image and follow the prompts.

3) According to the June 2024 Sun Communities investor presentation is the following statements.

Largest publicly traded owner /

operator of MH communities in

North America:

296 MH Communities

100K sites

96.7% Occupied

4) According to left-leaning Bing’s Copilot on this date:

Based on that information, it would appear that Sun has not kept pace with the average rate of inflation.

Source: Company information and U.S. Bureau of Labor Statistics. Refer to Sun Communities, Inc. Form 10-Q and Supplemental for the quarter ended March 31, 2024, as well as Press Releases and SEC Filings after March 31, 2024, for additional information. Refer to

information regarding non-GAAP financial measures in the attached Appendix.

Note: With respect to guidance, estimates and forecasted information, see “Cautionary Statement Regarding Guidance” on page 2 of this presentation.

1) Preliminary 2024 rental rate increases. CPI-U 12-month percentage change as of April 2024.

- Disposed of 2 MH properties in Florida and Arizona for ~$52mm

- 1,177 home sales in the UK through the end of May, an increase of 556 homes since March 31, 2024, and continuing to see demand for homes in our communities [MHProNews note: why is Sun able to boost sales at this pace in UK without making a similar effort to boost new home sales in the U.S.? After all there is still 3.3 percent vacancy, per their implied data (96.7 percent occupied is about 3.3 percent unoccupied – while that’s not perfect – due to properties that may have a home on a site but not an occupant – it is an indicator). Furthermore, Sun says they had 51,000 applications for Sun MHCs in 2023 alone. If that 51,000 applications statement is true, then why isn’t the firm at or near 100 percent capacity? Why are they pushing higher occupancy in the U.K., which is understandable, but not doing something vigorous that generates results here in the U.S.? Sun’s own statements, properly understood, often come back to bite their leadership, execution, and strategy.]

In several devices the image below can be opened to a larger size.

In many cases you can click the image and follow the prompts.

5) Keegan Carl with Wolfe Research, per the transcript above, asked:

Gary Shiffman: Yeah. I think we’ve talked about being very, very strategic in our thinking with use of capital. And we’ve also shared the plan that we’re looking to both recycle capital and dispositions, as well as through cash flow by shutting down development and using that cap will pay down more costly debt on a rate basis. I think that when you have 500 to 600 properties that are very, very strategically located and the strategic piece of land or opportunity comes about, we take advantage of that, thinking about the long-term nature of Sun. …”

MHProNews has kept readers abreast of the issue Carl with Wolfe research raised. Despite their claims of simplification and no new developing or acquisitions, from one quarter to the next they pivoted on the property acquisition front.

6) Note that while the headline specifically mentions Sun’s fellow MHI member Legacy Communities, the report provides an update on the class action litigation that Sun is a defendant in. The report takes a closer look at antitrust allegations that include Sun.

7) Per Sun’s own “management effectiveness” management is quite effective as measured by losing value. There are negative returns on equity, assets, and investments. How is it that the Sun board is allowing management to continue in a business-as-usual fashion?

In several devices the image below can be opened to a larger size.

In many cases you can click the image and follow the prompts.

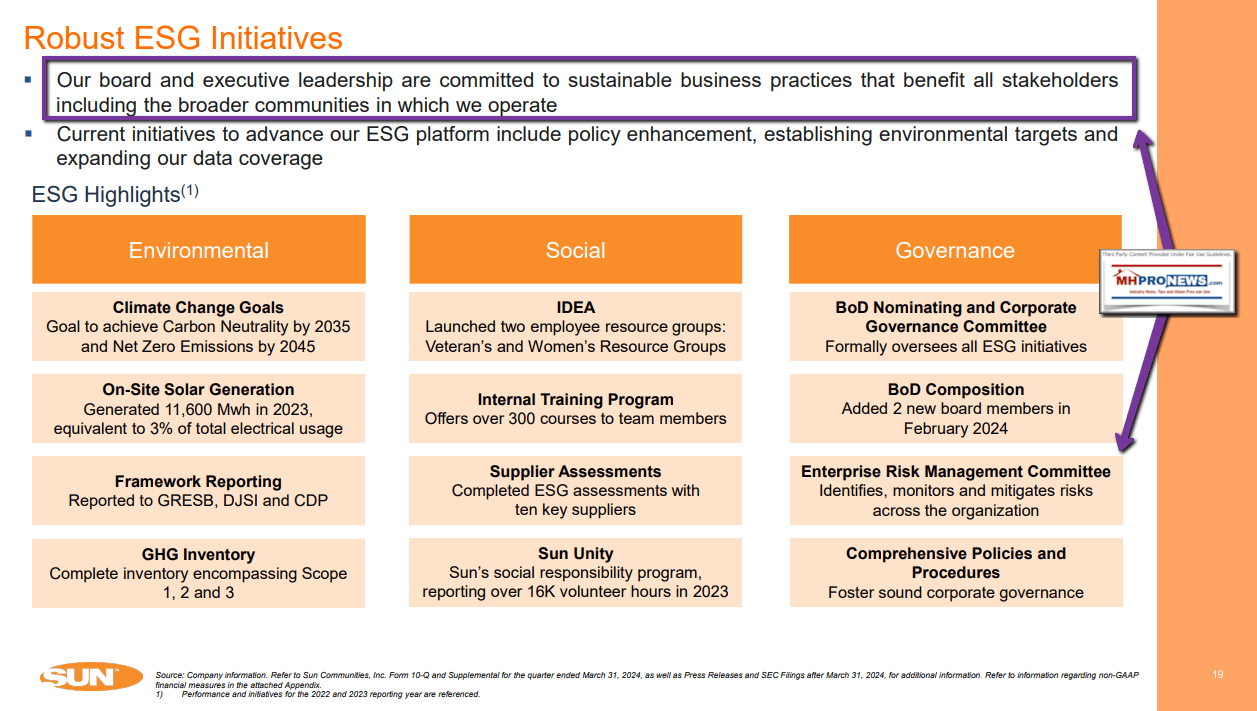

8) The ESG claims made by Sun may arguably be described as laughable.

Per the Sun ESG IR pitch page: “Our board and executive leadership are committed to sustainable business practices that benefit all stakeholders including the broader communities in which we operate.” Seriously? Ask their residents who are engaged in a class action suit if they are meeting the needs of that key stakeholder constituency. Ask their investors which are losing equity. Why not grow a pair and openly declare that ESG is a bad joke that may benefit a few deep pocketed investors, but is often harmful to smaller investors and society at large?

In several devices the image below can be opened to a larger size.

In many cases you can click the image and follow the prompts.

Fellow MHI member Cavco’s ESG statement to Congress, while also arguably hypocritical, aptly stated that ESG mandates distort markets and drives up costs for insurance and housing.

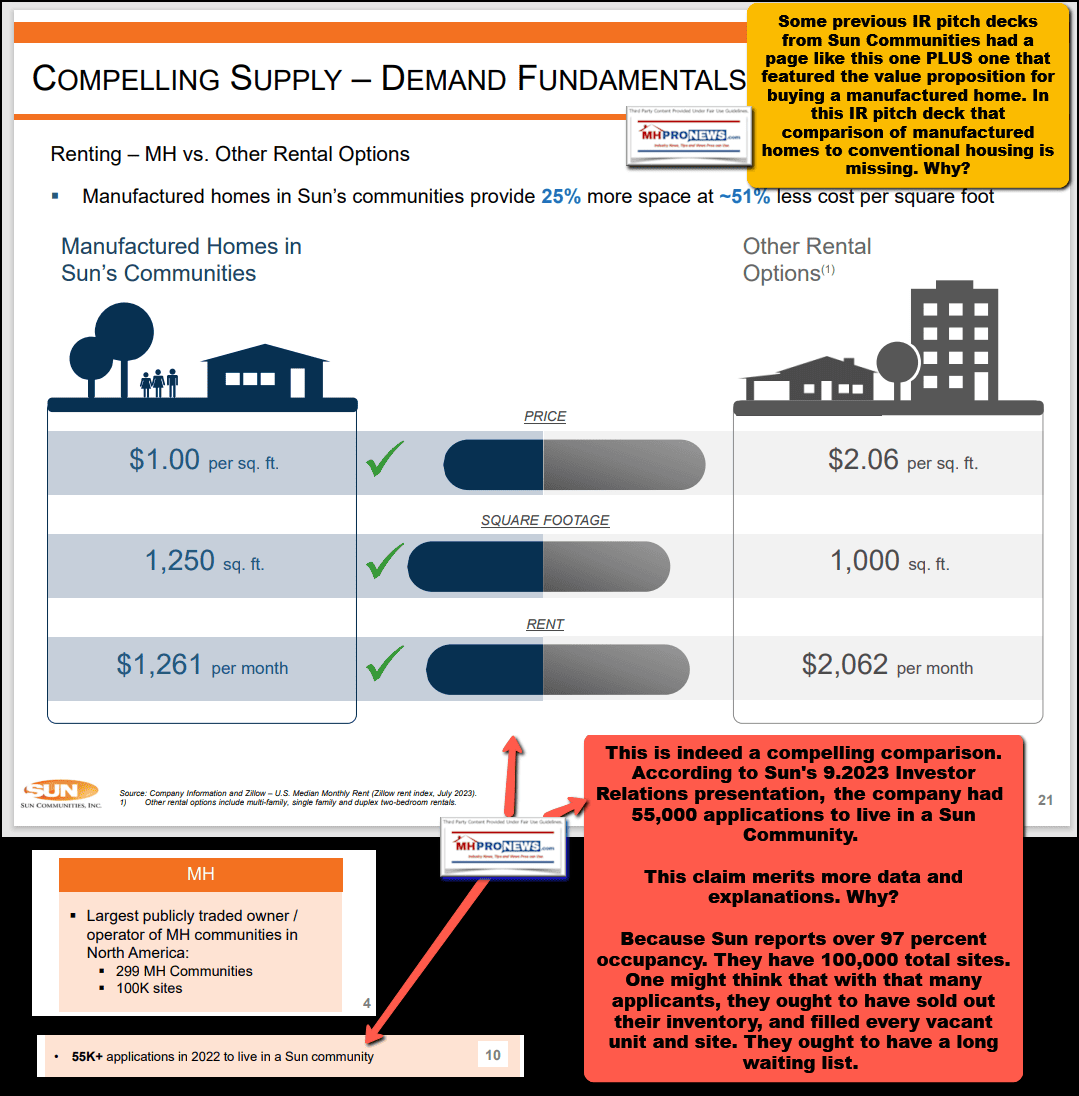

9) The policies of Sun and several prominent MHI members are arguably risky, per legal analysis – potentially illegal in terms of antitrust, RICO and of questionable materiality/SEC concerns – and have led the industry into years of poor performance during an affordable housing crisis. To boldly claim they are benefiting society (the S in social) is thus seemingly Orwellian. For years, Sun has apparently paltered. They are correct in saying that manufactured homes are a better option than multi-family housing and can be a path to homeownership for millions of renters.

In several devices the image below can be opened to a larger size.

In many cases you can click the image and follow the prompts.

This claim merits more data and explanations. Why?

Because Sun reports over 97 percent occupancy. They have 100,000 total sites. One might think that with that many applicants, they ought to have sold out their inventory, and filled every vacant unit and site. They ought to have a long waiting list. Their own statements bear scrutiny and follow up questions. For instance. What percentage of those applications were for properties other than MH? What is the fallout rate of interest (applications) and actually closing on a deal that results in a move-in? What would such insights tell current or potential investors in manufactured housing? https://www.manufacturedhomepronews.com/sun-communities-compelling-supply-demand-fundamentals-virtually-no-new-supply-added-for-years-but-manufactured-home-sales-drop-quarterly-y2d2023-data-with/

Note: depending on your browser or device, many images in this report can be clicked to expand. For example, in some browsers/devices you click the image and select ‘open in a new window.’ After clicking that selection, you click the image in the open window to expand the image to a larger size. To return to this page, use your back key, escape or follow the prompts.

10) Let’s stress again that not every MHI member is corrupt and predatory. That noted, several have for years have been peddling often-self-contradictory statements and behaviors. Sun falls into that category. Without implying any endorsement of Warren Buffett and his business practices, some of Buffett’s memorable remarks come to mind with respect to Sun.

11) A video documentary written, produced and directed by John Pilger with Alan Lowery that MHProNews is considering featuring in the near term provides numerous examples of the role that media plays in propaganda. In several ways, it supports the evidence and contentions in the previously reported items posted-linked below. But as is often true, the Pilger-Lowery production includes a clear focus on how important it is for media to be more than just stenographers for corporate or government interests. Pilger’s docu-drama, per AI powered Copilot: “The film questions the ethics and responsibility of the media in reporting the truth…” Failure to report the truth leads to serious, costly, and deadly consequences, says Pilger and several of those interviewed in that documentary.

Apply those notions to MHVille. In a sense, MHProNews benefits from trade publishers and would-be blogger/rivals because – however unintentionally – they routinely make us look good. While they are busy carrying water for MHI’s insiders, they are leading people into blind allies where they may get financially mugged.

Applying their own observations and pitches in a reasonably consistent fashion may tend to expose just how corrupt several of these operations appear to be.

12) Among the points that arise from Pilger’s documentary, if they were applied to MHVille, would reveal how important it is for media – that should include trade media – to ask the tough questions, to pay attention to the disconnects between the claims of officials and reality, and how a lack of transparency can lead to serious trouble. Manufactured housing ought to be soaring to record highs. But that is not the case. When the root issues are traced, it routinely comes back to some dominating firms that are members of MHI (or MHI-NCC). Sun is one of those members. There is a case to be made that the worst may be yet to come for several of these apparently corrupt and predatory operations. Should public officials and/or shareholder-stakeholder attorneys seriously dig into these issues, the results could call to mind other major 21st century scandals previously provided by MHProNews as cautionary tales/reminders to those involved in MHVille.

What’s happened before can happen again. The chickens for Sun’s leaders and faithful followers may be coming home to roost. Time will tell, so stay tuned. ###

In several devices the image below can be opened to a larger size.

In many cases you can click the image and follow the prompts.

![DuncanBatesPhotoLegacyHousingLogoQuoteZoningBarriersLookBiggestHeadwindIinThisEntireIndustryIsWhereToPut[HUDCodeManufactured]HomesMHProNews](http://www.manufacturedhomepronews.com/wp-content/uploads/2023/11/DuncanBatesPhotoLegacyHousingLogoQuoteZoningBarriersLookBiggestHeadwindIinThisEntireIndustryIsWhereToPutHUDCodeManufacturedHomesMHProNews.jpg)

Again, our thanks to free email subscribers and all readers like you, as well as our tipsters/sources, sponsors and God for making and keeping us the runaway number one source for authentic “News through the lens of manufactured homes and factory-built housing” © where “We Provide, You Decide.” © ## (Affordable housing, manufactured homes, reports, fact-checks, analysis, and commentary. Third-party images or content are provided under fair use guidelines for media.) See Related Reports, further below. Text/image boxes often are hot-linked to other reports that can be access by clicking on them.)

By L.A. “Tony” Kovach – for MHProNews.com.

Tony earned a journalism scholarship and earned numerous awards in history and in manufactured housing.

For example, he earned the prestigious Lottinville Award in history from the University of Oklahoma, where he studied history and business management. He’s a managing member and co-founder of LifeStyle Factory Homes, LLC, the parent company to MHProNews, and MHLivingNews.com.

This article reflects the LLC’s and/or the writer’s position and may or may not reflect the views of sponsors or supporters.

Connect on LinkedIn: http://www.linkedin.com/in/latonykovach

Related References:

The text/image boxes below are linked to other reports, which can be accessed by clicking on them.’