But as MHProNews and our MHLivingNews sister-site have uniquely documented in recent years, there is a pattern of evidence – a case that often provided by public companies make directly or by implication -that point to efforts that divert or downplay federal laws that could spark far more manufactured home sales. Put differently, by wild coincidence and/or design, the ‘bigger boys’ at the Manufactured Housing Institute (MHI) routinely support or accept failed efforts. Why? Because apparently market constraints that result in underperformance forces smaller players out, which means larger companies that can access capital can acquire others at discounted valuations.

Oversimplified, to coin the phrase, “the system is rigged.”

That rigging of the system, properly understood, purportedly harms consumers, white hat manufactured home independents, numbers of investors, and the general public because taxpayers often foot the bill for affordable housing programs that could be reduced if good federal laws were properly enforced.

Tonight’s featured focus is the most recent earnings call transcript from UMH Properties that arguably supports the thesis about the broader trends, as well as points made in our recent spotlight on UMH that is linked below.

As normal, the featured focus follows thought provoking quotable quotes, today’s left-right headline recap, and two of the three market snapshots at the closing bell today. The manufactured housing market summary of publicly traded equities at the close today follow the featured focus and the linked recent/related reports.

Quotes That Shed Light – American Social, Industry, National Issues…

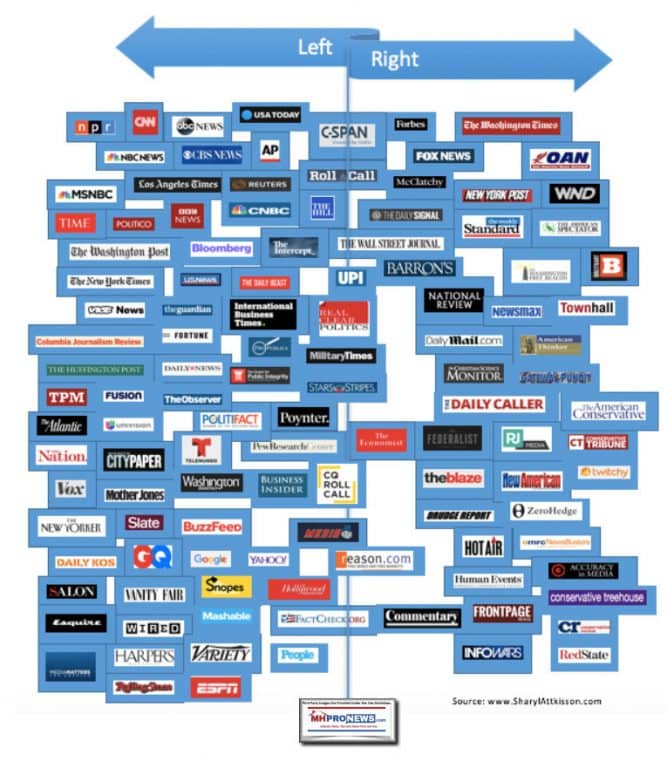

Headlines from left-of-center CNN Business

- Airlines get a lift

- LOS ANGELES, CA – NOVEMBER 11: United Airlines Boeing 737-924 takes off from Los Angeles international Airport on November 11, 2020 in Los Angeles, California.

- United and American welcome back thousands of furloughed workers after stimulus bill passes

- 10 years in prison for illegal streaming? It’s in the Covid relief bill

- The two Senate races in Georgia will shape the economic recovery

- Congress passed a $900 billion Covid rescue package. What now?

- Watch these Fox News hosts criticize holiday travel guidance

- Trump’s private bankers resign from Deutsche Bank

- Expanding a deduction for business lunches won’t do much to help restaurants

- Opinion: Biden’s childcare plan is essential if we want to restart the American economy

- Walmart is attempting to solve one of the biggest pain-points of online shopping

- 2020 has been the worst. But these work changes are sticking around

- How Google, Microsoft and others plan to work post-pandemic

- Sorry, but video meetings are here to stay

- Bridgewater Associates Founder & Co-Chairman/Co-CIO Ray Dalio speaks onstage during TechCrunch Disrupt San Francisco 2019 at Moscone Convention Center on October 02, 2019 in San Francisco, California.

- Billionaire is worried that America’s massive wealth gap could lead to conflict

- A Chinese flag hangs from a pole near the Semiconductor Manufacturing International Corp. headquarters in Shanghai, China, on Saturday, Dec. 19, 2020. The U.S. is preparing to blacklist SMIC and dozens of other Chinese companies, Reuters reported, citing people familiar with the matter.

- US strikes at the heart of China’s bid to become a tech superpower

- PHILADELPHIA – MAY 8: Economic stimulus checks are prepared for printing at the Philadelphia Financial Center May 8, 2008 in Philadelphia, Pennsylvania. One hundred and thirty million households are eligible to receive a tax rebate check under the $168 billion economic stimulus plan.

- How will you spend your $600 stimulus check?

- MARKETS

- ESCAPING SAN FRANCISCO

- FUERSTENWALDE, GERMANY – SEPTEMBER 03: Tesla head Elon Musk arrives to have a look at the construction site of the new Tesla Gigafactory near Berlin on September 03, 2020 near Gruenheide, Germany. Musk is currently in Germany where he met with vaccine maker CureVac on Tuesday, with which Tesla has a cooperation to build devices for producing RNA vaccines, as well as German Economy Minister Peter Altmaier yesterday.

- Here are all the millionaires and companies leaving Silicon Valley

- Elon Musk says he has moved to Texas

- Will Elon Musk’s move to Texas affect Tesla brand?

- Oracle is moving its headquarters to Austin

- The company that literally started Silicon Valley is moving to Texas

- WORK TRANSFORMED

- For the first time, there’s a woman on every S&P 500 board

- Here’s how the pandemic has changed work forever

- Performance reviews won’t be the same this year

- Want to switch careers? Don’t let the pandemic stop you

- Why Reddit will pay workers the same salary no matter where they live

- WHAT TO WATCH

- How the vaccine gets from the lab to your arm

- McDonald’s is putting cameras in dumpsters. Here’s why

- This vegan restaurant is actually opening locations during the pandemic

- 2020 was a dark year. These moments made it a bit brighter

- See Alaska Airlines’ Covid-19 ‘Safety Dance’

Headlines from right-of-center Newsmax

- More GOP Lawmakers Say They’ll Join Electoral College Challenge

- 6 is a key day in the election process, when Congress is to accept an Electoral College tally favoring Joe Biden. But some Republican lawmakers say they’ll mount a late-stage challenge to that process, even though political observers have describe it as a longshot. Still, the planned move threatens to disrupt a typically symbolic vote and divide even members of the same party.

- Election 2020

- Thune Sees Challenge to Biden Win Going Down Like ‘Shot Dog’

- Loeffler: Republicans Must ‘Hold the Line’ in Georgia

- Gingrich: Trump Should ‘Probably’ Attend Biden Inauguration

- Trump Defense Veto Threat Hangs Over Senate Runoffs

- Pat Robertson: Trump Should Move On, Not Run in 2024

- Peter Navarro: Stolen Election ‘Brass Knuckle Politics’

- Rudy Giuliani: Pennsylvania Lawsuit First of Many Efforts

- The Trump Presidency

- Biden Says Hack of US Shows Trump Failed at Cyber Security

- Acting Defense Chief Visits Afghanistan During Troop Pullout

- Trump Considering Pardons For Ex-Reps. Stockman and Hunter

- Congress Approves $900B COVID Relief Bill, Sending to Trump

- China Imposes New Visa Limits in Back-and-Forth with US

- Kushner Joins Israelis on Landmark Visit to Morocco

- US Publishes List of Chinese, Russian Firms With Military Ties

- Finance

- Tesla Stock Seen as Too Expensive, in Bubble Territory

- One researcher feels that Tesla stock is too expensive and is in bubble territory after the share price tumbled on Monday as it debuted on the S&P 500 and ended 6.5% down from a record high in the previous session.

- Deliveries Pile Up as Shoppers Avoid Stores, Hit Websites

- Apple’s Stock Surge Dwarfs GM After Car Rollout News

- Amazon Delays Hike in Fees It Charges Merchants Until June

- CEO Culp Earns $47M Payday by Winning Over GE’s Doubters

Market Indicator Closing Summaries – Yahoo Finance Closing Tickers on MHProNews…

Featured Focus –

Where Business, Politics and Investing Can Meet

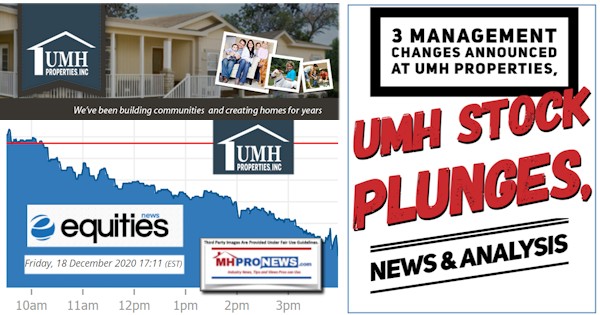

As the quote above reflects, UMH is bragging that their sales are up. But for those who do some math, the number of sales per community is less than 2 per location during the covered period. While rentals are – per UMH President and CEO Sam Landy – at about 8 rentals to 1 housing sale, the market – for whatever reason, is not buying it. At least that is what is suggested by the 5 year trend chart, shown below.

That noted, let’s dive into the most recent 3rd quarter transcript to see what light it sheds.

UMH Properties Inc (UMH) Q3 2020 Earnings Call Transcript

UMH earnings call for the period ending September 30, 2020.

Contents:

Prepared Remarks

Questions and Answers

Call Participants

Prepared Remarks:

Operator

Good morning, and welcome to the UMH Properties Third Quarter 2020 Earnings Conference Call. [Operator Instructions]

It is now my pleasure to introduce your host Ms. Nelli Madden, Vice President of Investor Relations. Thank you, Ms. Madden. You may begin.

Nelli Madden — Vice President, Investor Relations

Thank you very much, operator. In addition to the 10-Q that we filed with the SEC yesterday, we have filed an unaudited third quarter supplemental information presentation. This supplemental information presentation, along with our 10-Q, are available on the company’s website at umh.reit. I would like to remind everyone that certain statements made during this conference call, which are not historical facts, may be deemed forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. The forward-looking statements that we make on this call are based on our current expectations and involve various risks and uncertainties. Although the company believes the expectations reflected in any forward-looking statements are based on reasonable assumptions, the company can provide no assurance that its expectations will be achieved. Risks and uncertainties that could cause actual results to differ materially from expectations are detailed in the company’s third quarter 2020 earnings release and filings with the Securities and Exchange Commission.

The company disclaims any obligation to update its forward-looking statements. In addition, during today’s call, we will be discussing non-GAAP financial metrics. Reconciliations of these non-GAAP financial metrics to the comparable GAAP financial metrics as well as explanatory and cautioning language are included in our earnings release, our supplemental information and our historical SEC filings. Having said that, I would like to introduce management with us today: Eugene Landy, Chairman; Samuel Landy, President and Chief Executive Officer; Anna Chew, Vice President and Chief Financial Officer; Brett Taft, Vice President and Chief Operating Officer; Jim Lykins, Vice President of Capital Markets; and Daniel Landy, Vice President.

It is now my pleasure to turn the call over to UMH’s President and Chief Executive Officer, Samuel Landy.

Samuel A. Landy — President and Chief Executive Officer

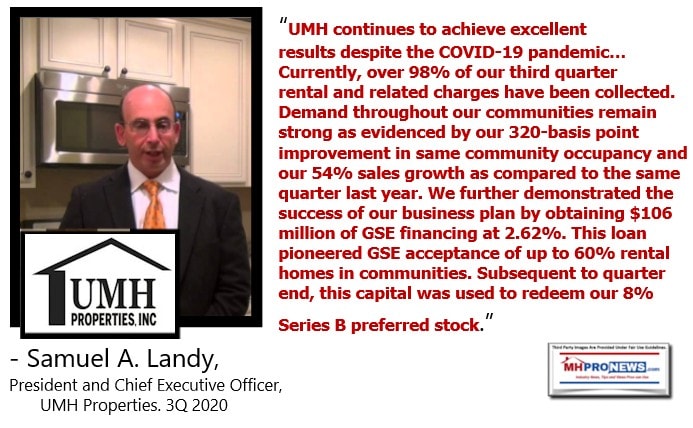

Thank you very much, Nelli. We are pleased to report our results for the third quarter ended September 30, 2020. UMH continues to achieve excellent results despite the COVID-19 pandemic. Our rent collections remain in line with our historical performance. Currently, over 98% of our third quarter rental and related charges have been collected. Demand throughout our communities remain strong as evidenced by our 320 basis point improvement in same community occupancy and our 54% sales growth as compared to the same quarter last year. We further demonstrated the success of our business plan by obtaining $106 million of GSE financing at 2.62%. This loan pioneered GSE acceptance of up to 60% rental homes in communities. Subsequent to quarter end, this capital was used to redeem our 8% Series B preferred stock. This 500 basis point improvement will result in over $5 million in additional FFO per year or approximately $0.12 per share. UMH is well positioned to excel in 2021. Normalized FFO for the third quarter was $0.18 per diluted share compared to $0.15 in the prior year period. This represents an increase of 20%.

We are pleased that our $0.18 dividend per quarter is now fully covered by our current operating performance. This is prior to the positive impact that the redemption of our Series B preferred will have on FFO. Our community operating results continue to improve. In accordance with our business plan, the value-add communities that we have acquired over the past few years are now starting to deliver significant revenue growth and are positively impacting our overall performance. Throughout the pandemic, we have continued our capital improvements, expansions and rental home additions. Our communities look better and are operating more efficiently than ever before. Total income for the quarter is up 16%. Year-to-date, total income is up 11%. Our operating expense ratio has decreased from 47.8% to 44.6%. The combination of income growth and expense ratio reduction resulted in overall NOI growth of 17% for the quarter and 19% for the year. Our same-property occupancy rate improved 320 basis points to 86.9% from the same quarter last year. This translates to an increase of 706 revenue-producing sites year-over-year.

This occupancy growth has contributed to income growth of 8.6% for the third quarter and 7.8% year-to-date, generating same-property NOI growth of 12.9% and 13.7%, respectively. This is the fourth quarter in a row that we have delivered double-digit same-store NOI growth. The primary driver of our overall occupancy and revenue growth is the rental home program. Through the COVID-19 crisis, rental homes have proven to be as stable and income stream as homeowner occupied sites. We have increased our rental home portfolio by 684 units so far this year. We are on track to add 800 to 900 new rental units this year. We now own approximately 8,100 rental homes. At quarter end, our rental home occupancy rate was 95.4%. As a result of our performance through COVID, we are more convinced than ever that rental homes and manufactured housing communities are the best way to provide quality affordable housing. We continue to seek value-add acquisition opportunities in strong markets where we can implement our rental home program. We recently entered into a line of credit with FirstBank secured by our rental homes and the income derived by them.

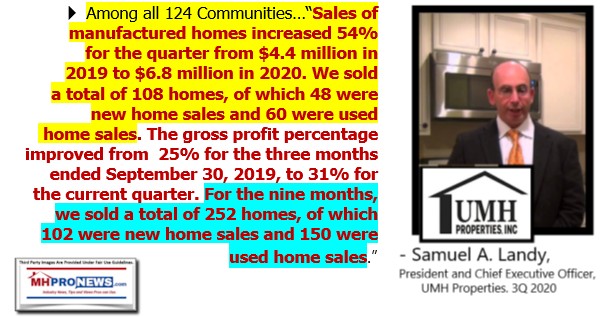

This line allows us to tap into the equity that we have in our rental homes at a reasonable rate of prime plus 25 basis points. Our goal is to continue to increase our rental home program and reduce the cost of capital used for that purpose. Gross sales for the quarter were $6.8 million, representing an increase of 54% over the same period last year. Gross sales for the year are at $15 million, which is now up 8% over the first three quarters of 2019. Despite the COVID-19 pandemic, we continue to see increasing demand for sales throughout our portfolio. Our sales generated income of approximately $640,000 for the quarter and approximately $450,000 for the year. As we continue to grow our sales volume, we expect to generate meaningful income, which will further improve FFO. To ensure that we have the lots available to generate this volume, we are working on developing additional sites at many of our best sales locations. We remain on track to complete the development of 191 sites this year. In 2021, we expect to obtain approvals on approximately 800 sites. We should develop about 400 of these approved sites in the next 18 months.

During the quarter, we closed on the acquisition of two communities containing 310 sites for a total purchase price of $7.8 million or $25,000 per site. These are value-add communities with an in-place occupancy rate of 64%. Over the next few months, we expect to complete our initial turnaround work and begin to infill the communities with rental homes. These communities are both located in markets that we already operate in, creating management efficiencies. We have been able to add to our acquisition pipeline. We have executed letters of intent on four communities in three new states that fit our growth criteria. These communities contain approximately 580 sites, of which 64% are occupied. The total purchase price for these communities is $21 million or $36,000 per site.

On previous calls, we have discussed our plans to improve community operating results, acquire and expand communities, improve sales profitability, refinance our capital stack and ultimately improve our FFO. During extremely difficult economic circumstances, we have achieved many of these goals and made substantial progress toward achieving the others. We have covered our $0.18 dividend prior to the positive impact that the redemption and refinance of our Series B preferred will have on earnings. This change in our capital stack is expected to add $0.12 of FFO per share annually. We have laid the foundation to deliver excellent FFO growth in 2021 and beyond.

Now Anna will provide you with greater detail on our results for the quarter and for the year.

Anna T. Chew — Vice President And Chief Financial Officer

Thank you, Sam. Normalized FFO, which excludes realized gains on the sale of securities and other nonrecurring items, was $7.4 million or $0.18 per diluted share for the third quarter of 2020 compared to $6 million or $0.15 per diluted share for the prior year period. As we had previously announced, we redeemed all 3.8 million issued and outstanding shares of our 8% Series B cumulative redeemable preferred stock totaling $95 million on October 20. This, together with our recent GSE financing, will generate savings of approximately 500 basis points or $0.12 per share annually going forward. Rental and related income for the quarter was $36.4 million compared to $32.9 million a year ago, representing an increase of 10%. Community NOI increased by 17% for the quarter from $17.2 million in 2019 to $20.1 million in 2020. These increases are attributable to our acquisitions, rent increases, the success of our rental home program and reduction of our operating expense ratio. Our operating expense ratio improved from 47.5% for the third quarter of 2019 to 44.7% for the current quarter.

For the nine months, our expense ratio decreased from 47.8% to 44.6%. At quarter end, our portfolio average monthly site rent increased by 2.7% to $455 over the same period last year. Our average monthly home rent increased by 2.8% to $781 over the same period last year. Same-property income for the third quarter increased 8.6% over the same period last year, while expenses increased by 3.2%, resulting in same-property NOI growth of 12.9%. Sales of manufactured homes increased 54% for the quarter from $4.4 million in 2019 to $6.8 million in 2020. We sold a total of 108 homes, of which 48 were new home sales and 60 were used home sales. The gross profit percentage improved from 25% for the three months ended September 30, 2019, to 31% for the current quarter. For the nine months, we sold a total of 252 homes, of which 102 were new home sales and 150 were used home sales. The gross profit percentage was 29% and 27% for the nine months ended September 30, 2020 and 2019, respectively. As we turn to our capital structure, at quarter end, we had approximately $507 million in debt, of which $472 million was community level mortgage debt and $35 million was loans payable. 93% of our total debt is fixed rate.

The weighted average interest rate on our mortgage debt was 3.81% at quarter end compared to 4.14% in the prior year. The weighted average maturity on our mortgage debt was 6.3 years at quarter end compared to 6.2 years a year ago. At quarter end, UMH had a total of $383 million in perpetual preferred equity, not including the $95 million of our Series B preferred stock, which was redeemed on October 20. Our preferred stock, combined with an equity market capitalization of $564 million and our $507 million in debt, results in a total market capitalization of approximately $1.5 billion at quarter end, representing an increase of 3% over the prior year period. From a credit standpoint, our net debt to total market capitalization was 31%. Our net debt less securities to total market capitalization was 25%. Our net debt to adjusted EBITDA was 5.8 times. Our net debt less securities to adjusted EBITDA was 4.7 times. Our interest coverage was 4.1 times, and our fixed charge coverage was 1.5 times. From a liquidity standpoint, we ended the quarter with $55 million in cash and cash equivalents, $60 million available on our unsecured credit facility with an additional $50 million potentially available pursuant to an accordion feature and $29 million available on our revolving lines of credit for the financing of home sales and the purchase of inventory.

We also had $85 million unencumbered in our REIT securities portfolio. This portfolio represents approximately 6% of our undepreciated assets. We limit our portfolio to no more than 15% of our undepreciated assets. With the exception of reinvesting our dividends, we are committed to not increasing our investments in the REIT securities portfolio. The company continues to enhance its liquidity position. Through our preferred and common stock ATM programs, we raised net proceeds of $9.8 million during the quarter and $73 million during the nine months. Subsequent to quarter end, we raised an additional $14.2 million through these programs. Additionally, as Sam mentioned, in October, we entered into a $20 million line of credit with FirstBank secured by our rental homes and the income derived by them. This line is expandable to $30 million with an accordion feature. In conjunction with the Series B preferred stock redemption, subsequent to quarter end, we drew down $30 million on our unsecured credit facility and $26 million on our margin line.

And now let me turn it over to Gene before we open it up for questions.

Samuel A. Landy — President and Chief Executive Officer

We have been incredibly pleased with the performance of our portfolio of 124 communities. We believe the favorable performance will continue in the years ahead. Our staff, despite the burden of the pandemic, has continued to serve the housing needs of our communities. UMH has acquired communities, installed and rented new homes, profitably sold homes, completed capital improvements, expanded communities and financed communities and rental homes at historically low interest rates. As a result of these accomplishments, UMH is well positioned for a productive 2021 and beyond. The shortage of affordable housing is a critical domestic issue facing our nation. The pandemic has caused the population migration from the cities to the suburbs. UMH is now experiencing an increased demand for affordable single-family housing. In an age where environmental, social and governance concerns are highly valued, UMH seeks to become a preferred investment as it provides the nation with much-needed affordable housing. UMH’s capital stock includes preferred shares that could be redeemed with lower-cost capital in both 2022 and 2023.

Our properties have become more valuable. They have increased occupancy levels and improved operating metrics. Incumbent properties should become eligible for increased GSE financing at low rates. The potential for favorable changes in the capital stock is one important factor. The favorable economics in the housing market provides a pathway for UMH’s improved operating results. Housing values are now increasing because of economic fundamentals. In addition, the winds of inflation may also begin to blow across the landscape. We have built a much needed important housing company over our 53 year history. The years ahead can reflect the prudence of long-term values and visions.

We will now be happy to take your questions.

Questions and Answers:

Operator

[Operator Instructions] And our first question will come from Barry Oxford with D.A. Davidson. Please go ahead.

Barry Oxford — D.A. Davidson — Analyst

Great. Thanks. Sam, when we look at your for-sale portfolio and how that’s tracking and then we look at the rental, given this economic environment, how do you look at those two businesses over the next six to nine months? Do you see it favoring more the rentals?

Samuel A. Landy — President and Chief Executive Officer

For the next six to nine months, yes, I think we’ll always rent out about eight homes for every one we sell. There is work being done nationally on the finance issue to make financing more available for the retail customer to securitize those loans and make financing more available for the resale of homes, all of which could generate additional and more profitable sales. But at the same time, the rental business solves the problem of the customer who doesn’t want to be tied down, who’s only staying at a place three years or less. So, I think rentals will always be about 8:1 with sales.

Barry Oxford — D.A. Davidson — Analyst

Great. Thanks. And Sam, you’ve been fairly active on the acquisition side. Are you — and I know that it’s hard to find these acquisitions and actually win these deals. As you look out over the horizon, again, maybe over the next six to nine months, do you see a continued strong pipeline? Or [Barry], we just kind of had a flurry of activity in here?

Samuel A. Landy — President and Chief Executive Officer

No. Brett is going to give you more detail. But basically, our philosophy is this: we know how hard it is to get approvals to build new communities. It’s extremely hard. But you can expand your existing communities, and we know expansion sites close to about 70,000 a piece. The acquisitions other people do are 95% occupied communities buying at about a four cap. We can find communities pretty much all over the country that, for various reasons, have declined to 70% occupancy and have deferred maintenance, lack of capital improvements. And so basically, you’re buying the bones at a very low price, $25,000 a site, you renovate the community, make it as new relatively quickly for only an additional $10,000 a site, add the rental units, fill the community, it becomes very profitable, looks just like a brand new community, and we can do this all over. Basically, we’ve created this river of income coming from 124 communities, which are our 124 tributaries, and we can continue to add to that by acquiring communities and sites at low prices, upgrading them and adding rental units. And now Brett will tell you more about our acquisition pipeline.

Barry Oxford — D.A. Davidson — Analyst

Yes. So, we have four deals under letter of intent right now. Two of those, we do expect to sign the contract today. I think everybody will be happy to hear that these are in three new states. The two that we’re going to sign the contracts on are in Alabama and South Carolina. These are value-add communities. They’re in strong demographic markets, which should have very favorable rental demand. Those two were 345 sites and they’re only 40% occupied. But again, they’re in strong markets with big populations and very good comparable rental housing in the market. So, we think our business plan will work very well there. Those two are $8 million or $23,000 per site. We’re getting them at a reasonable price, where we can go in, implement our business plan and create — generate significant value. The other two properties aren’t quite as far along.

So, I can’t get into too many specifics, but it is in another new state in the Northeast. It’s 235 sites, 97% occupied. It’s not our typical value-add deal, but there is a value-add component in the fact that there’s an old sales center, which we plan to reopen. It’s a very strong sales market. And we also have the ability to develop some additional sites at the property. So those four deals represent $21 million total. We’re very happy with where the pipeline stands currently, and we look forward to growing it in the near future. Great. Last question. Anna, when we look at G&A, you guys have been running 8% of revenues. Is that good? Are you comfortable with that number? Or look, G&A might be moving in 2021 for this reason?

Anna T. Chew — Vice President And Chief Financial Officer

Well, G&A right now is about 6.5% of total income, and we believe that, that is a good number. In 2019, it was also about 6.5%. It was 6.4%. But as we grow, we’ve been growing our G&A, but still at a reasonable amount compared to our total income because our total income has been growing just as fast or if not faster.

Barry Oxford — D.A. Davidson — Analyst

Right. Perfect. Appreciate it. All right. Thanks, guys.

Samuel A. Landy — President and Chief Executive Officer

Thanks, guys.

Operator

Our next question will come from Rob Stevenson with Janney. Please go ahead.

Rob Stevenson — Janney — Analyst

Good morning, guys. Sam, you’ve been having some big gains in occupancy that’s really been juicing the same-store results. At what point do those gains start to slow down that the year-over-year comps become much more challenging or it’s tougher to get the occupancy gains going forward once you get 88%, 89%?

Samuel A. Landy — President and Chief Executive Officer

Well, I believe that the supply of new, affordable housing is that something like a 40-year low. So, with that in mind, there’s a lot of reason to believe we’ll continue to increase occupancy from our 86% into the mid-90s by adding the rental units. So, I really don’t see a negative change there. I see — the cost of building new communities, the difficulties of building affordable housing, our competitors in apartments, townhouses, condos cost much more money. We have a fantastic product at a fantastic price, and I really only see revenue and occupancy growth there.

Rob Stevenson — Janney — Analyst

Okay. So I guess another question, a related question is, so how much rental unit demand is there beyond what you’re already tapping to within your existing communities? In other words, you guys added, I think it was 317 rental units in the third quarter. And so if you added [100 million] (sic) [100] more rental units last quarter, would you have been able to lease a good chunk of them up? Or was demand essentially plus or minus a bit the 317 units that you did and that’s why you didn’t add 400 or 500 rental units in the quarter?

Samuel A. Landy — President and Chief Executive Officer

There’s a number of timing issues. One is how long it takes to get the house from the factory. Two is how long it takes to set it up. And just like a developer building a housing development, we consider successful to be adding four homes per month. It’s usually not realistic to expect to go much faster than that, although we have it in some communities. So we expect managers in communities to fill about four units per month. And so we look at it, speaking to a Vice President of Rentals, who’s very on top of demand. And on a same-store basis, we expect to add the 800 to 900 units. These new acquisitions with their vacancies give us the opportunity to accelerate that. But again, you have a little bit of a time lag because the first year and a half we have to turn around the physical asset, improving it, improving the reputation, marketing, getting personnel who knows how to do what we want to do. But following that, it’s additional vacant sites for us to fill quickly.

Rob Stevenson — Janney — Analyst

Okay. And then lastly for me. If I’m doing my math right, you guys sold 108 homes for around $6.8 million in the quarter, boils down to sort of $62,000, $63,000 a home. Is that reflecting — is that similar homes that you were doing over the last few quarters and just reflecting cost inflation on homes? Is that reflecting more expensive homes that you sold, either double wides or improvements, et cetera, or add-ons and stuff like that? Because $63,000 seems higher than what you guys have been selling the last year or so.

Samuel A. Landy — President and Chief Executive Officer

So Brett will help me with the exact numbers. But before December 31, we’re going to complete how many lots? It’s approximately…

Brett Taft — Chief Operating Officer

191 lots, yes.

Samuel A. Landy — President and Chief Executive Officer

And next year, we expect to complete?

Brett Taft — Chief Operating Officer

So through the spring of 2021, it’s 324 lots.

Samuel A. Landy — President and Chief Executive Officer

Okay. And all of those new lots are going to be primarily used for multi-section sales, which can range from $120,000 to over $200,000. So you should, in the future, have a higher average price per home sale. And they’re on the same general markup, 30%. So that should improve. The demand for the multi-section houses has been good. And there’s also the learning curve as we acquired new communities, teaching the people to sell and add homes, and that’s all going in the right direction. So there’s a lot of reason to believe we’re going to continue to increase sales at higher prices, higher total revenue and higher profits.

Anna T. Chew — Vice President And Chief Financial Officer

The margin overall was about $60,000, $62,000. But on the new homes, the average price on the new homes was $93,000 versus about $88,000 last year. And then on the used, it was about $37,000 for both last year and this year. That’s on a total for year-to-date.

Rob Stevenson — Janney — Analyst

Okay. What — how much more square footage are the bigger ones or the nicer ones having versus the stuff that you’re buying for rentals, et cetera?

Samuel A. Landy — President and Chief Executive Officer

Rentals are generally 1,000 square foot, 16 by 62 homes, could be 68, could be 70. And sales homes are generally multi-section, the used homes are single section. But the new homes are your 28 by 60, 28 by 70. It can even be 32, but most of ours are 28.

Rob Stevenson — Janney — Analyst

Okay. Perfect. Thanks, guys. I appreciate it.

Operator

Our next question will come from Allen Zitting with Home. Please go ahead.

Allen Zitting — Home — Analyst

Hello. Thank you. Where is — you’ve got almost as many used homes as new homes. I’m just wondering where all the used home inventory is coming from. Are you picking those up when you buy new parks? Or are they people foreclosing on the newer homes that were in previous quarters? What — where are those coming from?

Brett Taft — Chief Operating Officer

Yes. So a lot of different places. We have 8,100 rentals and a lot of those used home are going to be used rental home sales. Certainly, there are some foreclosures, but nothing significant, nothing outside of the norm. So yes, it’s going to be a combination of rentals and some of those older foreclosures. But again, it’s nothing outside the norm, and it’s about where we would expect it to be.

Allen Zitting — Home — Analyst

I see. About what percentage is selling a rental home?

Anna T. Chew — Vice President And Chief Financial Officer

Well, we had a total sales of used homes of about — I guess, it would be about 140, 150 units. So if you think of 150 units, most of those being our rental homes, and we have 8,000 rental homes, so it’s really a minimal amount that is being sold on an annual basis.

Allen Zitting — Home — Analyst

But the percentage of what you sold was repossessed homes. Is that like 3% or 30%? Or…

Anna T. Chew — Vice President And Chief Financial Officer

It’s a minimal number. I don’t have the exact number, but I would think it would be under 5%.

Samuel A. Landy — President and Chief Executive Officer

And that percentage and number goes up and down with the economy. And today, with things very good, there’s very few repos.

Allen Zitting — Home — Analyst

Yes. That makes sense. Okay, so it’s just people — it’s just rental homes are getting sold. I wonder what portion of the rental homes being sold are getting sold to the people that were renting the home, that were in the home.

Samuel A. Landy — President and Chief Executive Officer

Almost all, right?

Anna T. Chew — Vice President And Chief Financial Officer

Yes, for the most part. I mean, people rent the homes, they like it and they would like to buy it. There may be also some others that — we always have our homes for sale or rent. So therefore, if a person wants to stay for over three years and they want a lower priced home than our double wides, which can go for $100,000, we may sell them or rental.

Allen Zitting — Home — Analyst

Yeah. Okay. Thank you very much.

Operator

Our next question will come from Keegan Carl with Berenberg. Please go ahead.

Keegan Carl — Berenberg — Analyst

Hey, guys. Thanks for taking my question. So first, I know you haven’t issued formal guidance, but maybe if you could give us some color on what your rental increases are looking like going into next year. Are they kind of on par with what you’ve done so far this year?

Samuel A. Landy — President and Chief Executive Officer

Yes. So it’s 4% on any communities with over 80% occupancy. If they have less, they won’t get a rent increase at all. This year, there was a delay. When COVID began, there were no rent increases for approximately three months. So that actually decreased our increased revenue from rent increases, although revenue growth was very strong.

Anna T. Chew — Vice President And Chief Financial Officer

And that was because of occupancy, too, because the occupancy went up. So that made up for the delay in our rent increases.

Keegan Carl — Berenberg — Analyst

Okay. That’s helpful. And then I know you guys have mentioned about how you expanded into several new states. Can you maybe give us some color on particular states you’re looking at? And what pipelines could look like several years down the road? Do you think there’s more opportunity in some newer states than where you’re currently at?

Samuel A. Landy — President and Chief Executive Officer

Well, the best thing to do is to duplicate what we did in Nashville, and what we found in Nashville was neglected communities just outside of the center of the city. And it appears there’s more opportunities like that, predominantly in the South, but probably in other places. And the higher the population is the better we will do. And that’s what we’re looking for. And what COVID made us recognize, pre-COVID, people would always ask, “How would we do in a downturn with the rental homes?” And we always assumed we do as well as apartments, but that could generate vacancies in a decline. But in fact, we maintained 90 — what’s the percentage?

Brett Taft — Chief Operating Officer

95.7% rental home occupancy.

Samuel A. Landy — President and Chief Executive Officer

95.7% rental home occupancy and 98% rent collection. So it really doesn’t get any better than that. So with that in mind, we knew there’s no reason not to grow this business. And so we actively started searching new markets and fortunately we’ve already found deals that we can do. And we are sure there are more of them, and we will continue looking and doing them.

Keegan Carl — Berenberg — Analyst

Okay. Cool. And just one final one for me. How should we think about the funding mix going forward, especially now that you’ve utilized your preferred ATM?

Samuel A. Landy — President and Chief Executive Officer

So the most important thing here is that we’ve redeemed the $98 million in 8% preferred using the new debt at 2.62%. So that benefits us forever, and it benefits us at the rate of $0.12 per share. So that is incredible, and there’s going to be further opportunities to do the exact same thing. We’ll continue to issue preferred and potentially common through the ATM to keep a strong balance sheet. But Anna will give you more color on redeeming the future preferreds as they come due and using mortgage debt.

Anna T. Chew — Vice President And Chief Financial Officer

Well, we have our Series C, which is about $250 million right now, that’s at 6.75%, and that comes due in July of 2022 or redeemable in July of 2022. And our D is at about $135 million, 6.375%, redeemable January of 2023. So over the next few years, we have about $100 million of mortgages which will be coming due. And because of the value we’ve created and because of the increased occupancy and increased income, we believe that those communities will generate maybe approximately $200 million in mortgages. So we’ll have another $100 million right there. Also, we have been working with FirstBank and with that was the GSEs to try to — and with FirstBank, we’ve already succeeded that we are able to tap into our rental homes, the equity in our rental homes. In the past, we had purchased these rental homes using preferred stock. And now we have been able to get a $20 million line of credit, which is expandable to $30 million, and since it’s a new program, it’s probably even expandable further. But the interest rate on those loans is going to be about prime plus 0.25%, which is about 4.5% — I’m sorry, 3.5%. So the savings that we’ll have there and the additional rental home that we will be able to finance is another avenue of capital.

Samuel A. Landy — President and Chief Executive Officer

And just to repeat what we tell people when we meet with them, in 2011, when we first went to rental units, we had to get acceptance by our residents in the community that people who owned homes accepted rental homes. We had to get acceptance by our bankers and acceptance by our investors. The people in the communities have clearly accepted rental units. They recognize brand-new homes upgrade the communities and increased the value of the homes they own. This loan was a giant milestone because now Fannie Mae has recognized the value of rental units and given us this 2.62% mortgage. And we continue to work with the GSEs to create a program to strictly finance the chattel, the rental home, at low rates.

That’s being worked on every day but has not been implemented as of yet. And the last party that needs to accept it is the investors, which I think have not really yet noticed what we’ve done. You have apartment REITs, you have rental home REITs, you have manufactured home REITs, but nobody’s recognized the value and our ability to grow this business of rental manufactured homes and communities. It’s the way to provide affordable housing. It meets the social need. We’re the lowest-cost producer of quality, affordable housing. And UMH has the staff, our professional engineers, vice presidents, sales staff, to continue to do it and grow.

Keegan Carl — Berenberg — Analyst

Alright. Thanks for the question guys.

Operator

[Operator Instructions] Our next question will come from Craig Kucera with B. Riley FBR. Please go ahead.

Craig Kucera — B. Riley FBR — Analyst

Good morning guys. I want to start out talking about your sales. Given the pickup in pace here this quarter, do you anticipate any inventory issues over the next several quarters if demand remains this high?

Samuel A. Landy — President and Chief Executive Officer

It is a problem. We’re pushing the manufacturers that they have to way — find a way to produce more houses, and I believe that’s doable. You have issues with setup companies. You need more setup crews. There’s issues that the factories have with getting materials. So there are issues out there that may slow down our growth, but we’ve continued to replace anything we sell with new homes. And to an extent, we’d like to go faster, and I know there’s some delays out there. Brett can be more specific.

Brett Taft — Chief Operating Officer

Yes. So backlog, all of a sudden at the factories ramped up to about five to six months. So it certainly is an issue. And to Sam’s point, we’ve always kept a good amount of inventory knowing that this could happen. So right now, we do have inventory in stock, but our orders that we’re placing now are going to be delivered in March and, in some cases, April. So we are proactively ordering inventory so that if these backlogs continue, we won’t have this issue.

Craig Kucera — B. Riley FBR — Analyst

Got it. And when you’re selling used homes, do you have to complete any meaningful capex on those homes before you put them up for sale? Or is it pretty low cost?

Samuel A. Landy — President and Chief Executive Officer

Go ahead, Anna.

Anna T. Chew — Vice President And Chief Financial Officer

Pretty low cost. I mean we always maintain our rental homes. So therefore, there’s very minimal cost involved when we sell.

Craig Kucera — B. Riley FBR — Analyst

Okay. Got it. I want to circle to the dividend policy. I think you’ve been at about $0.18 a quarter since 2009. With the strength in operations, mid-double-digit same-store NOI, you’ve got the reduction in your cost of capital here in the fourth quarter going forward and a few things coming up over the next several years. Can you talk about how the Board would view the dividend if your payout ratio drops significantly in 2021 and maybe beyond?

Eugene W. Landy — Chairman Of The Board

Well — this is Eugene Landy, Chairman. We are always considering whether we can increase the dividend. And we’re not tied as much to convention of FFO. When you look at our quarterly reports or yearly reports, the value of our communities is rising rapidly, and these values can be realized by financing the communities. And so we have access to mortgage capital, and we’re not at a very high capital — we’re not over leveraged at all. And so if you think company is going ahead $50 million a year in value and you talk about 40-some million shares and increasing the dividend by $0.05 or $0.10, you’re talking about $2 million, $4 million, that’s not significant. And that — we want the investment community to realize how well the company is doing and how much the value of the company is going up each year.

So that — we will consider increasing the dividend, but really because of — we don’t want to be too unconventional. But as we go over the $0.72, if we pick up the additional $0.12 on the refinancing of the 8% preferred, if we — as we approach a dollar per share FFO, you can be sure that we will seriously consider increasing the dividend to reflect the real values that are occurring and increased value of the company. And of course, there’s a potential for the company growing as we go to full occupancy and have our rents approach the competitors’ rents and the additional efficiencies caused as you get to be fully occupied. So yes, we are going to consider that, but let’s have a couple of good quarters first, then we’ll take that step.

Samuel A. Landy — President and Chief Executive Officer

But my math is if you increase the dividend $0.01 per quarter during 2021, at the end of the year, you might wind up at an $0.18 payout ratio with a $0.04 dividend increase. So we’ll play that day by day. But if things work out, that’s where we could be.

Craig Kucera — B. Riley FBR — Analyst

Got it. Brett, I wanted to circle back on the acquisitions. Are the two other properties you mentioned in the Northeast likely to close here in fourth quarter? Or are those possibly going to slip into first quarter or first half of next year?

Brett Taft — Chief Operating Officer

So I don’t want to touch on that too much, but I would say it’s much more likely that they close in the first quarter of 2021. We’re not under contract yet. So timing-wise, diligence, et cetera, they are unencumbered, so that does help us. But first quarter is more likely.

Craig Kucera — B. Riley FBR — Analyst

Got it. And can you talk about the pricing differential from a cap rate perspective between buying these 40% occupied assets in the South versus the 95% ones in the Northeast?

Brett Taft — Chief Operating Officer

Sure. So the Northeast properties are in that 5.5% range, which I think is actually a pretty good price given what we see in other areas of the market. Properties, high-quality communities in our markets are trading at 4%, 4.5% cap rate. So we’re very pleased with where we are there. The deals in the South, it’s tough to put a cap rate on them. I mean I would be giving you a projection because at 40% occupancy, it’s really not a cap rate play. We’re buying them at a cost per site that we think is reasonable. We can get in there, make the improvements at our $50,000 rental home and earn a return that we’re very comfortable with. So those, I wouldn’t put a cap rate on it only because we’re going to go in there, we’re going to do some significant capital improvements or will be home removal. Those properties will go backwards before they go forward. But after two or three years, you’re going to be the significant — you’re going to see the significant NOI growth that you’ve seen in our other previous acquisitions.

Samuel A. Landy — President and Chief Executive Officer

And we’ve taken a look at — what’s the percentage return on properties we’ve owned, say, 10 years?

Brett Taft — Chief Operating Officer

Yes. So it’s between 40% and 100%, depending on what year you look at, and that’s even less than 10 years. That’s 5, six years in some cases. So we certainly generate a solid total return after we’re able to get in there, clean these properties up, stabilize them and ultimately, increase occupancy and reduce our expenses.

Craig Kucera — B. Riley FBR — Analyst

And because they’re 40% occupied, does that extend sort of the period at which you would get it stabilized? I feel like, traditionally, you’ve been buying closer to 60% or 70% and get it stabilized inside of three years, let’s say. Does this become maybe four or five years? Or do you think it’s still pretty much on target for your normal kind of two or 3-year stabilization period?

Brett Taft — Chief Operating Officer

I’d say it’s probably three years. I mean I really — based on what we see in the market, it’s a strong rental demand market. We’ve had properties — this year, for instance, one of our 2018 acquisitions went forward 100 rental homes. So assuming strong demand of 25 to 50 homes per year, it’s a 3-year process. If for whatever reason it lags behind that, then sure it could certainly drag on a little bit. But the good thing is we’re looking for markets where, based on the in-place demographics, we think we can execute based on what we’ve done in our Northeastern portfolio. So the plan is the two to 3-year turnaround.

Craig Kucera — B. Riley FBR — Analyst

Okay. Great. Thanks.

Operator

This concludes our question-and-answer session. I would like to turn the conference back over to Samuel Landy for any closing remarks. Please go ahead.

Samuel A. Landy — President and Chief Executive Officer

Thank you, operator. I would like to thank the participants on this call for their continued support and interest in our company. As always, Gene, Anna, Brett and I are available for any follow-up questions. We look forward to reporting back to you in March with our fourth quarter and year-end 2020 results. Thank you.

Operator

The conference has now concluded. Thank you for attending today’s presentation. The teleconference replay will be available in approximately one hour. To access this replay, please dial U.S. toll-free one (877) 344-7529 or international at one (412) 317-0088. The conference ID number is 10147928. Thank you, and please disconnect your line.

Duration: 51 minutes

Call participants:

Nelli Madden — Vice President, Investor Relations

Samuel A. Landy — President and Chief Executive Officer

Anna T. Chew — Vice President And Chief Financial Officer

Brett Taft — Chief Operating Officer

Eugene W. Landy — Chairman Of The Board

Barry Oxford — D.A. Davidson — Analyst

Rob Stevenson — Janney — Analyst

Allen Zitting — Home — Analyst

Keegan Carl — Berenberg — Analyst

Craig Kucera — B. Riley FBR — Analyst

##

(MFTranscribers)

Nov 5, 2020 at 11:31PM

UMH Properties Inc (NYSE:UMH)

Q3 2020 Earnings Call

Nov 5, 2020, 10:00 a.m. ET

###

MHProNews will unpack more of this in the days ahead. But for now, to learn more about these issues, see the related reports, shown below.

Related, Recent, and Read Hot Reports

Manufactured Housing Industry Investments Connected Closing Equities Tickers

Some of these firms invest in manufactured housing, or are otherwise connected, but may do other forms of investing or business activities too.

- NOTE: The chart below includes the Canadian stock, ECN, which purchased Triad Financial Services, a manufactured home industry lender

- NOTE: Drew changed its name and trading symbol at the end of 2016 to Lippert (LCII).

- NOTE: Deer Valley was largely taken private, say company insiders in a message to MHProNews on 12.15.2020, but there are still some outstanding shares of the stock from the days when it was a publicly traded firm. Thus, there is still periodic activity on DVLY.

Winter 2020…

Berkshire Hathaway is the parent company to Clayton Homes, 21st Mortgage, Vanderbilt Mortgage and other factory built housing industry suppliers.

· LCI Industries, Patrick, UFPI, and LP each are suppliers to the manufactured housing industry, among others.

· AMG, CG, and TAVFX have investments in manufactured housing related businesses. For insights from third-parties and clients about our publisher, click here.

Enjoy these ‘blast from the past’ comments.

MHProNews. MHProNews – previously a.k.a. MHMSM.com – has celebrated our 11th year of publishing, and is starting our 12the year of serving the industry as the runaway most-read trade media.

Sample Kudos over the years…

Learn more about our evolutionary journey as the industry’s leading trade media, at the report linked below.

· For expert manufactured housing business development or other professional services, click here.

· To sign up in seconds for our industry leading emailed headline news updates, click here.

Disclosure. MHProNews holds no positions in the stocks in this report.

That’s a wrap on this installment of “News Through the Lens of Manufactured Homes and Factory-Built Housing” © where “We Provide, You Decide.” © (Affordable housing, manufactured homes, stock, investing, data, metrics, reports, fact-checks, analysis, and commentary. Third-party images or content are provided under fair use guidelines for media.) (See Related Reports, further below. Text/image boxes often are hot-linked to other reports that can be access by clicking on them.)

By L.A. “Tony” Kovach – for MHLivingNews.com.

Tony earned a journalism scholarship and earned numerous awards in history and in manufactured housing. For example, he earned the prestigious Lottinville Award in history from the University of Oklahoma, where he studied history and business management. He’s a managing member and co-founder of LifeStyle Factory Homes, LLC, the parent company to MHProNews, and MHLivingNews.com. This article reflects the LLC’s and/or the writer’s position, and may or may not reflect the views of sponsors or supporters.

{kind=link}