According to Kevin Clayton, “Literally every time when I would talk to Warren [Buffett, Chairman of Berkshire Hathaway] he would say, “Kevin, you and the team need to make that decision. Just rest assured you have plenty of capital to do so.” It doesn’t get much better than that.” That is straight from Clayton’s mouth as captured on the video posted in this report, analysis, and expert commentary with the video transcript provided below. Clayton remark came after Buffett’s statement per an annual letter by Buffett to Berkshire Hathaway shareholders that reflected upon the “cardiac arrest” of “the financial system” in “September 2008…” That year, per Buffett’s letter, “Berkshire was a supplier of liquidity and capital to the system, not a supplicant. At the very peak of the crisis, we [Berkshire Hathaway] poured $15.5 billion into a business world that could otherwise only look to the federal government for help.” That year, as the markets largely melted down, Buffett’s letter said: “Our [Berkshire Hathaway] gain in net worth during 2009 was $21.8 billion, which increased the per-share book value of both our Class A and Class B stock by 19.8%.”

There is no known indication that Buffett’s remarks to Clayton about access to capital have ever been rescinded. Indeed, experience has shown that Berkshire has directly or through guarantees continued to supply Clayton Homes and their affiliated lenders with the capital or money supply they needed or desired. As Kevin says in the video/transcript below, “Not having to worry about capital and the public markets provides a lot of extra time to work on building a better home.”

There is obviously time to work on an array of other things beyond ‘building a better home. Kevin has invested in the “Company Store” and a restaurant chain, for example.

Why do those words about access to capital and the advantages it gives Clayton matter?

Consider other comments made by Clayton or Buffett or the array of possible ways that more capital access could be used to increase the output of the manufactured home industry in general, or Clayton and their affiliates more specifically.

Then consider that among other potential investors in the manufactured housing industry (a.k.a. MHVille) are large private equity giants, if they so desired. Hold those thoughts for the analysis and commentary portion of this report that follows the video transcript.

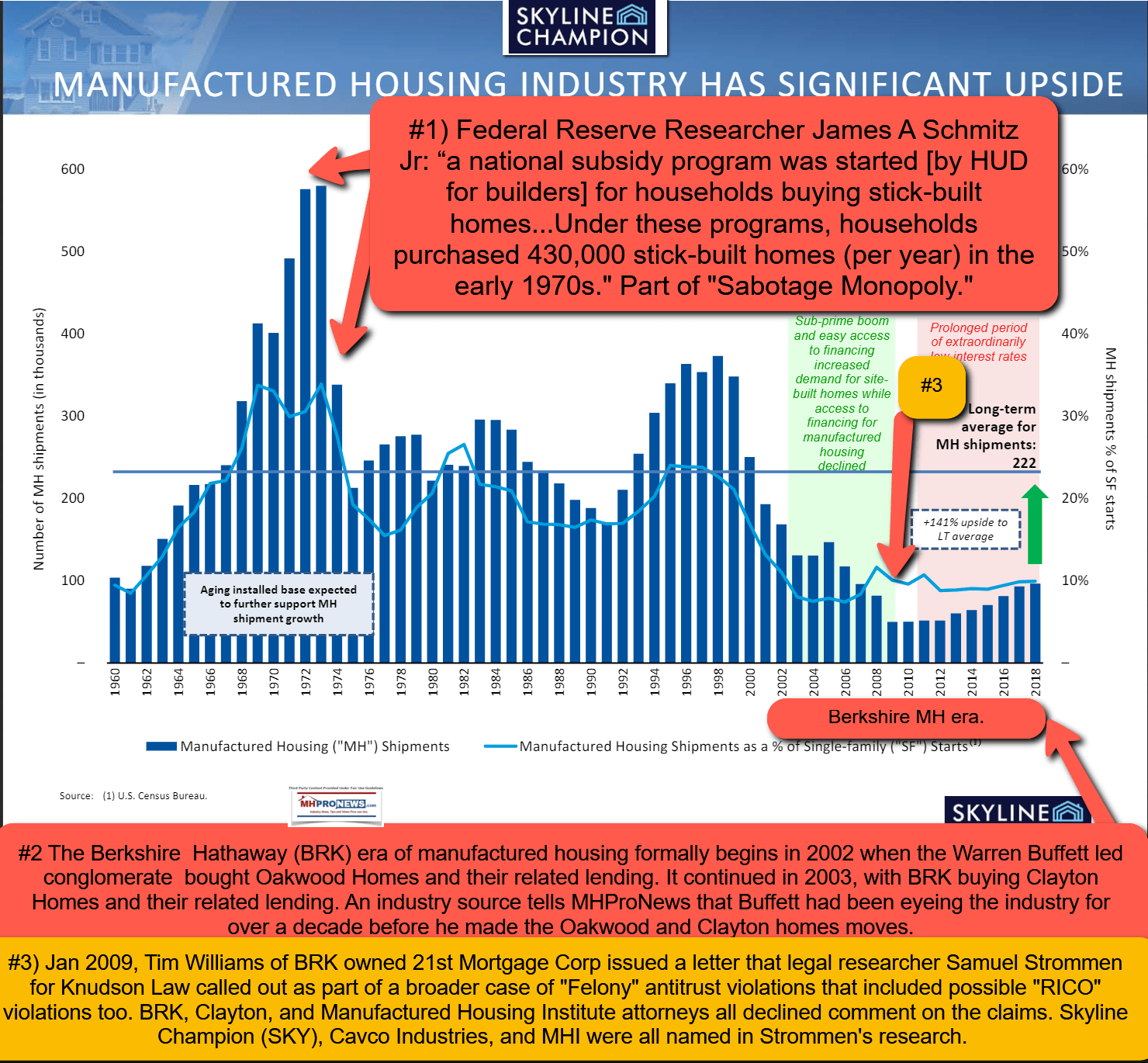

That said, note that Buffett’s remarks to Kevin, as the report linked here documented in a systematic fashion, apparently contradicted a now infamous letter in 2009 from Tim Williams, President and CEO of 21st Mortgage Corporation.

Per that letter from 21st’s Williams sent to thousands of retailers, communities, loan brokers, and others, Williams said in part the following.

- 1) We will no longer offer any of our programs to Mortgage Brokers.

- 2) We will offer FHA Title 1 financing for any brand homes subject to retailer meeting FHA requirements.

- 3) All other finance plans will only be offered for sales of the following homes:

- a) 21st Mortgage repossessions

- b) New homes built by Clayton Homes, Karsten Homes, Southern Energy or any other Clayton Homes subsidiary. The dealership must be a 21st Mortgage approved retailer.

- c) For any brand of home floor planned by 21st Mortgage prior to March 1 2009.

- d) For any brand of home sold from a retailer’s inventory provided the retailer replaces the Inventory with a home built by a Clayton Homes subsidiary.

- 4) Any loan application approved before March 1 must be closed before the loan approval expires. …”

A PDF of the full letter by Tim Williams reportedly sent to thousands via ‘the wires’ and the U.S. Mail is linked here. An annotated copy of that Williams’ letter on 21st letterhead with relevant remarks is linked here.

The case has been made by a legal researcher that the Williams letter was a prima facie example of the antitrust violation known as “tying.”

Tying and Antitrust Law

According to the U.S. Justice Department website: “1) A tying arrangement occurs when, through a contractual or technological requirement, a seller conditions the sale or lease of one product or service on the customer’s agreement to take a second product or service.” While it is common, as that Justice Department article stated in its closing line that “When the Agencies do identify anticompetitive situations, however, they will pursue them.” The DOJ is one of two federal agencies that are on point for antitrust enforcement.

The Federal Trade Commission (FTC) is the other federal agency tasked with antitrust legal enforcement. The FTC also cites tying as routinely being a violation of antitrust laws. The FTC framed that as follows: “but the general rule is that tying products raises antitrust questions when it restricts competition without providing benefits to consumers.”

Lending is the lifeblood of housing, noted Eric Belsky who was then a Harvard fellow with the Joint Center on Housing Studies (JCHS).

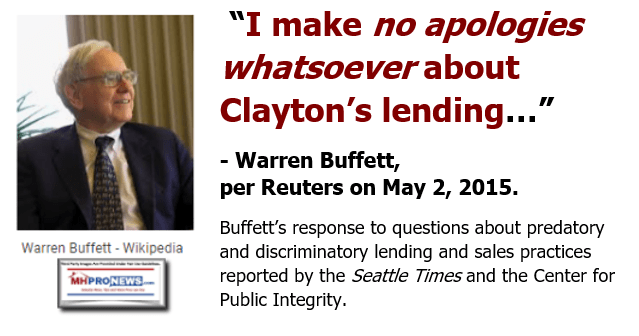

Given the ongoing U.S. affordable housing crisis the collapse of the manufactured housing market following that letter from Williams cutting off lending to thousands of independent manufactured home operations not selling Clayton Homes benefited that Berkshire brand but was clearly harmful to scores of competitors. It would therefore be difficult to argue that there was no consumer harm or that the 21st letter did not ‘restrict competition.’ While some may think that statute of limitations may apply, there are also legal arguments that can be made that allow for an extension of legal action beyond statutes of limitations. Note that the original version of this video on YouTube has had the comments turned off and is no longer available for posting on other websites. Fortunately, MHProNews captured that YouTube video interview in its entirety. Miles and Kevin Clayton’s remarks are unchanged in that video, which is posted below. There are facts and editorial comments added to the visuals that point to issues that ought to be of interest to legal and manufactured housing industry researchers. The case could be made that this video is therefore ‘better’ for researchers.

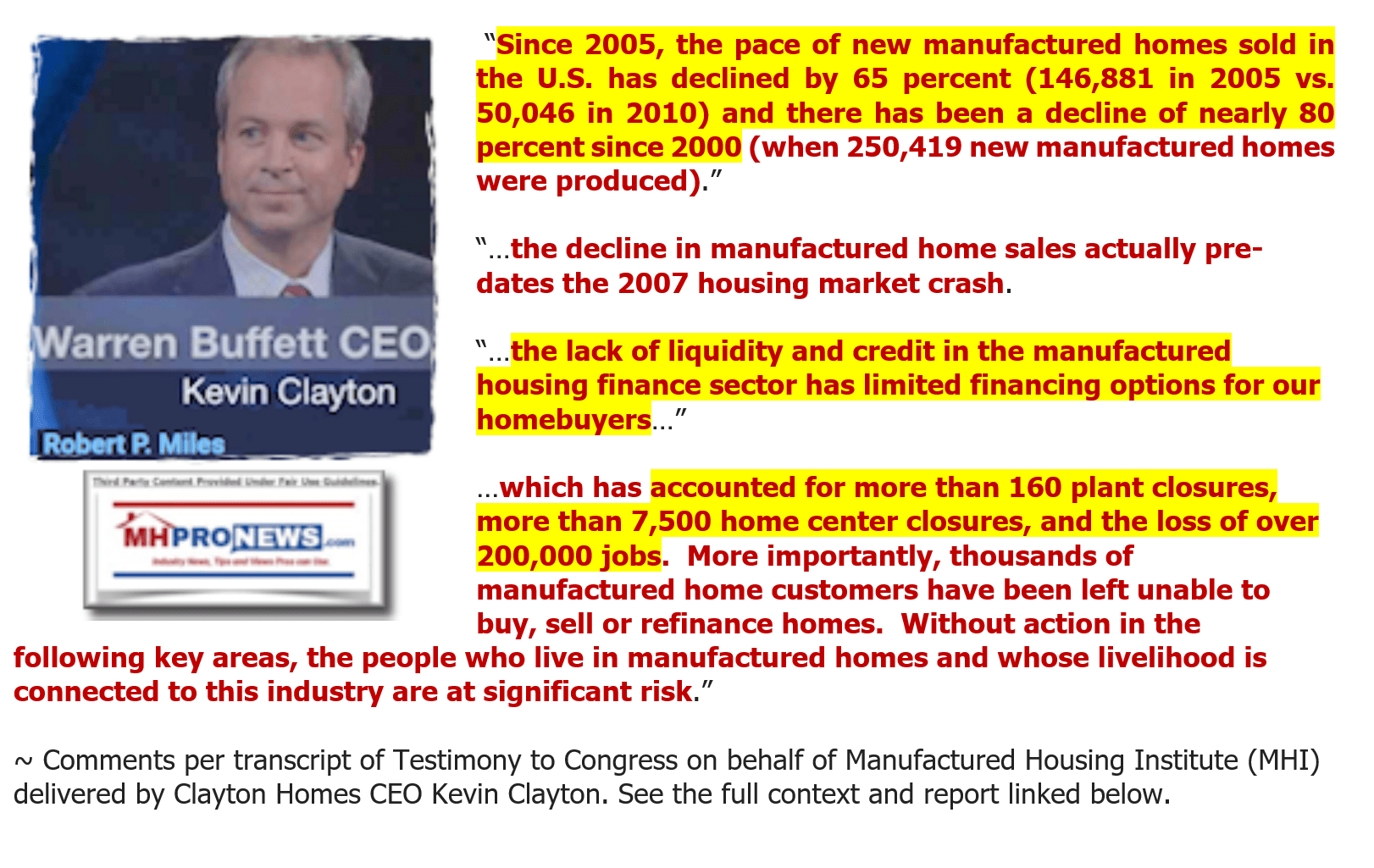

The impact of that 21st letter on the market can be measured in part by Clayton’s own words to Congress, although he failed to mention that Williams letter in his testimony which occurred about the same timeframe that this video (with related interview transcript) was produced.

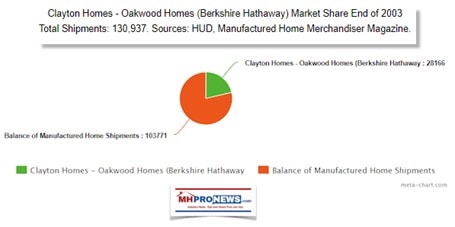

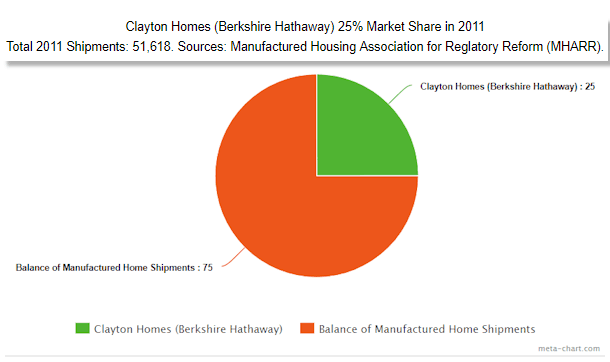

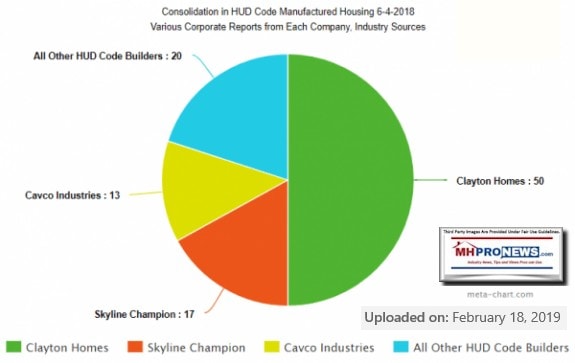

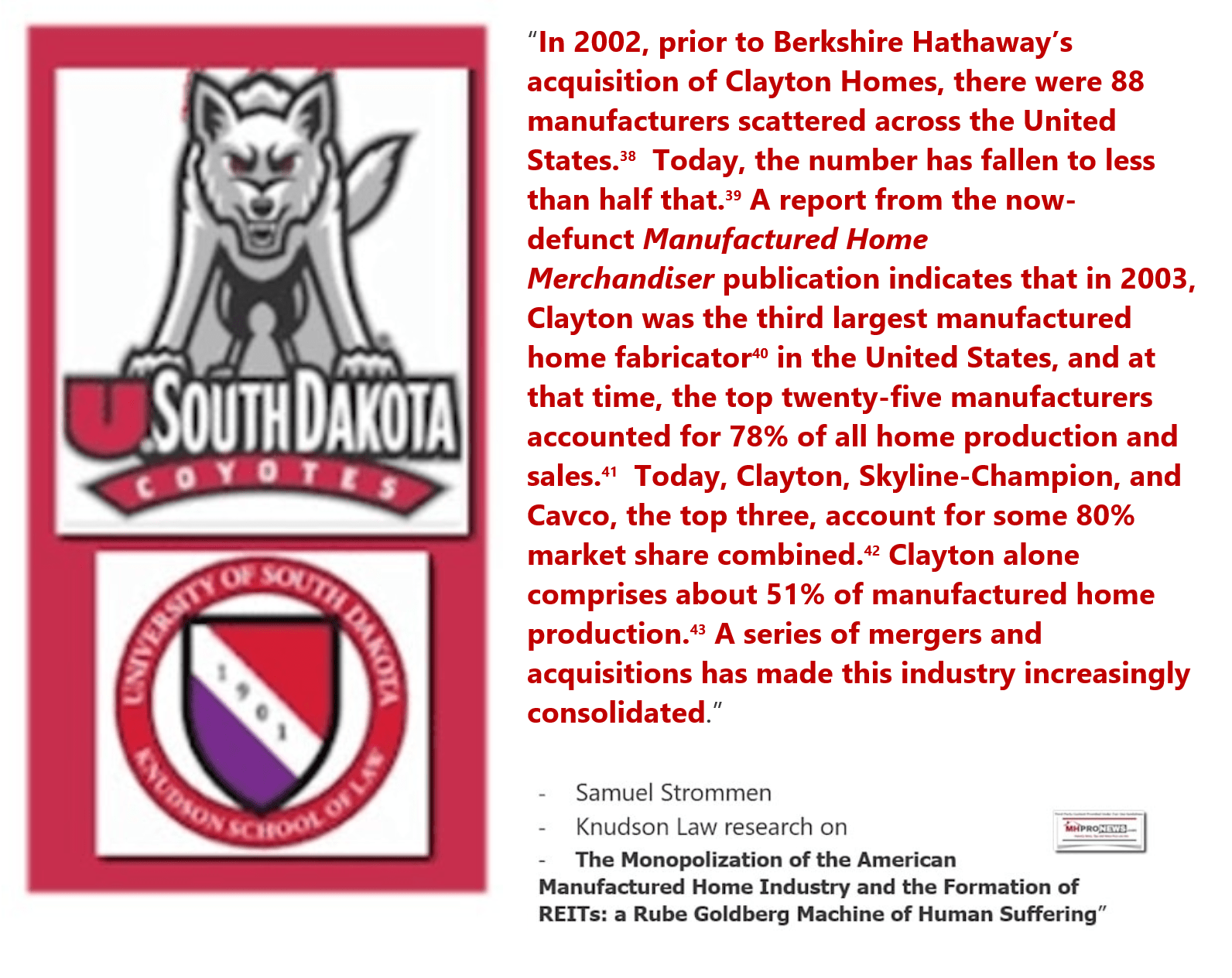

Putting the impact in market share terms, the following graphics are revealing. After the Berkshire effectively bought an interest in Oakwood Homes in 2002 and then purchased Clayton Homes in 2003 and ‘rolled’ Oakwood Homes into Clayton, the combined market share of those two brands was as shown in the first graphic below. The second graphic below reveals the market share at about the time of the Clayton interview with Robert Miles. The third graphic reveals the market share enjoyed by Clayton Homes circa 2018.

There are any number of insightful, stunning, and revealing statements by Kevin Clayton in the video posted above with the reported transcript shown below. Don’t let the casual, seemingly good-natured softball interview of Kevin by Miles lull you into complacency. For instance, keep paltering in mind.

When the facts and nuances about the manufactured home industry and market conditions at that time are clearly understood, some of Clayton’s comments are more subtle while others are rather brazen in nature.

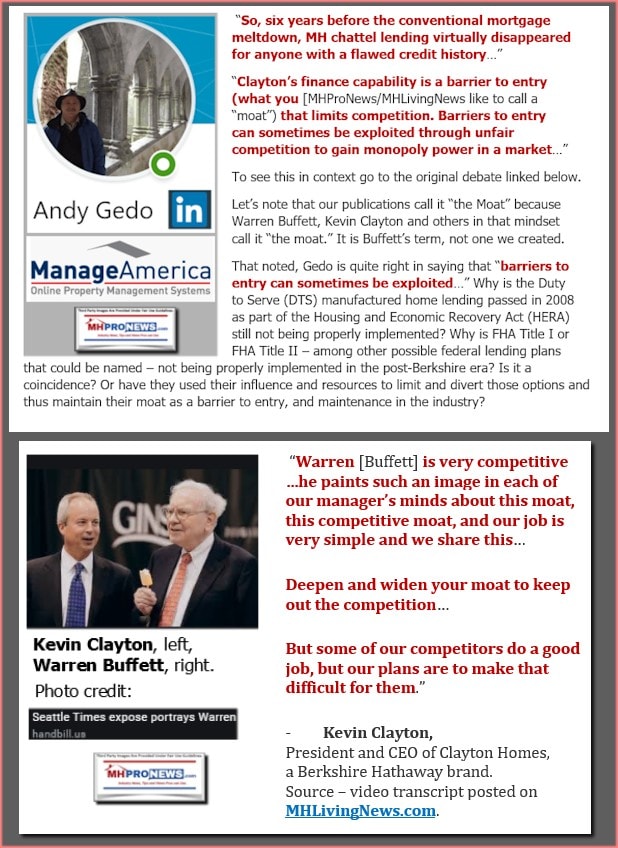

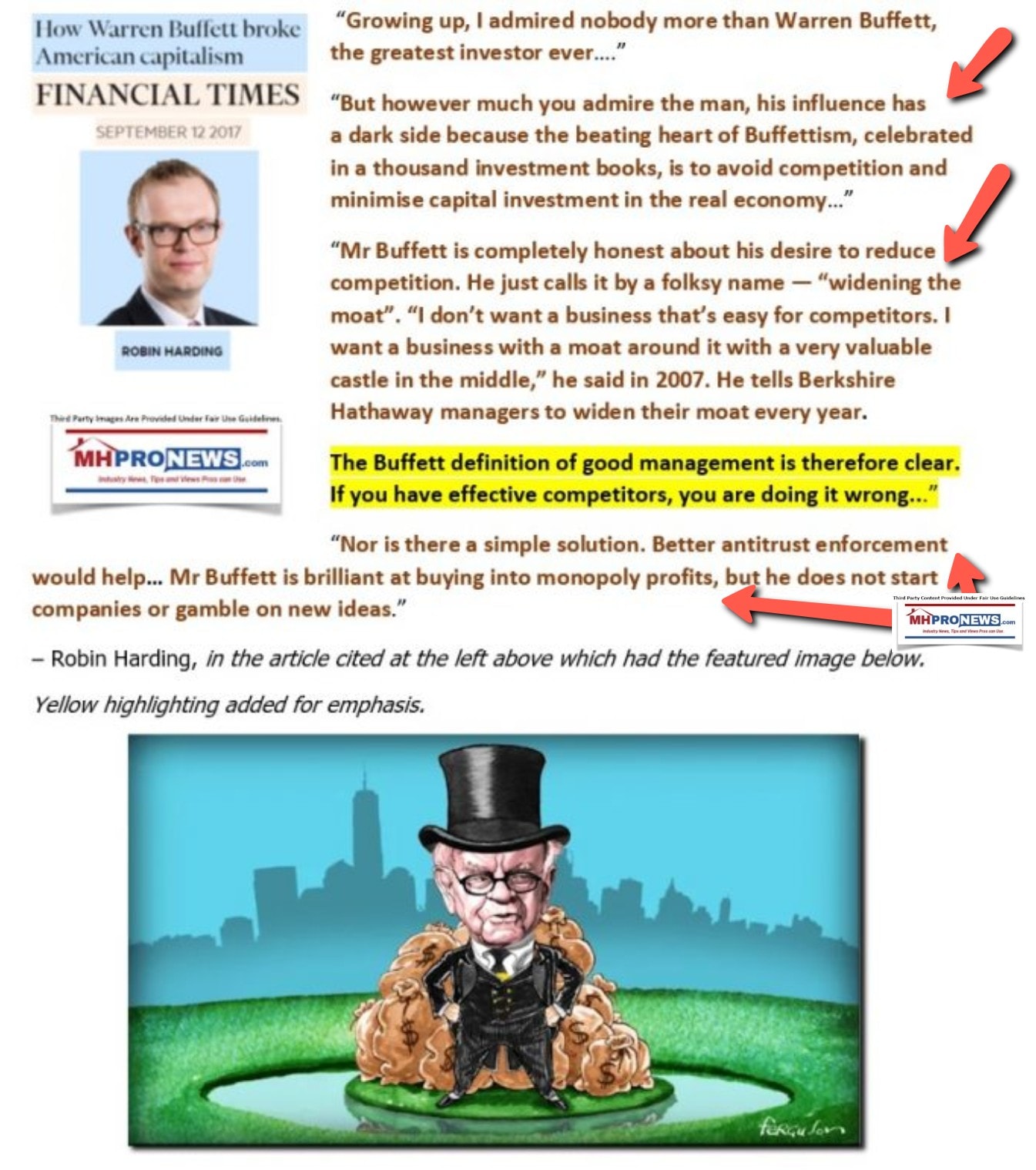

For example. Clayton made it no secret that “Warren” disliked competition. Kevin described the moat methodology as preached by Buffett was also repeated by Clayton management to their staff members. Tom Hodges, general counsel for Clayton Homes and prior Manufactured Housing Institute (MHI) Chairman who still serves on the MHI “executive committee” has also used the moat language in his communications.

Approaching 14 years since Williams’ notorious letter led to the collapse of thousands of street retailers or ‘dealers.’ The apparently deceptive nature of that letter by Williams was illustrated by Buffett’s pledge to Kevin that they have plenty of capital. The natural and logical conclusion to be drawn is that Buffett-Kevin-Williams wanted to put large numbers of competitors out of business.

And so, it occurred. That also fits the general comments by Buffett ally and large Berkshire investor, William “Bill” Gates III.

That harmful impact on independent retailers had ripple effects for manufactured home producers as well as manufactured home communities. Once giant companies in manufactured housing, such as Fleetwood or Champion were already struggling. They were apparently tipped into insolvency as were many others. This led to the subsequent era of the elimination or consolidation of the types of competitors that Buffett ‘hated.’

The effects of that episode are still being felt as the most proven affordable housing in U.S. history went into decline in the 21st century. What was once as high as 50 percent of U.S. housing starts in the early 1970s, per James A. “Jim” Schmitz Jr and other researchers into the pre-HUD Code mobile homes that transformed into HUD Code manufactured housing. Manufactured homes held over 20 percent market share of U.S. single family housing starts for much of the 20th century. But now, the current market share during an affordable housing crisis has hovered around the 9 to 10 percent mark for several years. That trend in manufactured housing market share for single family housing starts begs the question. Why did the manufactured home industry drop in the 21st century?

For several reasons, therefore, this video and transcript are provided as part of the 2022 manufactured housing year in review. As MHProNews has reported, there is anecdotal evidence that more legal research into the manufactured housing field is occurring. Few items have had more impact on modern manufactured housing than this troubling and seemingly illegal episode when capital access was cut off to large swatches of manufactured housing. A range of failures followed. That has direct and indirect impacts on all housing, on taxpayers, on affordable housing seekers, investors, and others. Following this letter will be additional information with more MHProNews analysis, additional linked reports, and an MHProNews expert commentary in brief. Note that this video is from 2011, and facts have obviously changed. But the value of this video is precisely because it is a snapshot of that moment in time as told by Kevin Clayton. The case can be made that this video has more meaning today than when it was first broadcast, streamed, or posted on YouTube.

Warren Buffett CEO: Kevin Clayton with Robert Miles Video Interview Transcript

Robert “Bob” Miles:

Kevin Clayton:

Thank you, Bob. It’s nice to be here.

Robert Miles:

I’m wondering if you can describe just what Clayton Homes is.

Kevin Clayton:

We are a very large affordable housing producer. We currently have 36 manufacturing plants and each of those terrific general managers runs their operation. They’re scattered across the whole US from coast to coast. Between all of those plants, we’ll build almost 200 houses each and every day. We have 450 retail stores that we own and in addition to that, we have about 1,200 wonderful independent retailers that buy product as well from us. Then the finance company, around 450,000 customers paying monthly. We try to earn their mortgage business on each sale that we make out there. Then we write insurance as well. Being a Warren Buffet company, he particularly like the insurance and of course the financing.

So, it’s five businesses in one.

Robert Miles:

It is.

How did you happen to get into the business?

Kevin Clayton:

Fortunately for me, my father was raised on a cotton farm in west Tennessee. They picked cotton every day, and his father had a dream for my dad, and that was to carve out five or ten acres. Dad would have his own land there and continue to be a sharecropper. My dad had some different plans, and fortunately for us, he moved to Knoxville, Tennessee and started selling multiple jobs, as you can imagine. Literally had three jobs at all times, got into the radio and broadcasting business. Started running some line ads while he was in the fraternity selling used cars and shortly thereafter, he had a used car lot and not too much longer after that, took a trade in of a manufactured home for a used car. Made more on the trade in of the mobile home and the story starts going from there. It wasn’t long we were driving to Elkhart, Indiana buying new manufactured housing and started that segment of the business.

Robert Miles:

But how did you get into the business?

Kevin Clayton:

That was the question, right. I really grew up working around my dad night and day. All of my brothers and sisters too, we all contributed from setting up installing manufactured homes. It was a lot of fun growing up around that and watching the company grow. My mom and all of us worked to try to make it happen.

Robert Miles:

You sold the business to Warren Buffett, and it started after Warren was visited by students from the University of Tennessee. They gave him a book.

Kevin Clayton:

Correct. He fortunately read the book and placed a call into us. He called my father and dad was out snow skiing. My dad retired in 1999 so this was late ’02 or 2003. My dad passed the call along to me and what an honor it was to, of course, call Warren. We talked for several minutes and before I knew it, he became very interested in our company. I sent a small package to him. Of course, I’ve heard that story from other people. You send a small package to Warren and he lets you know very quickly what interest he has.

Robert Miles:

Possibly for the first time in history, somebody’s been phoned by Warren Buffet and he didn’t call him back.

Kevin Clayton:

That’s right.

Robert Miles:

Your dad instead gave the phone call to you because you were managing the business.

Kevin Clayton:

Correct.

Robert Miles:

Pretty amazing. Even the Bank of England calls Warren, but your dad knew that you were running the business and let you handle the call.

Kevin Clayton:

Yeah.

Robert Miles:

Selling your business to Warren, you sent him a package of three years’ financials?

Kevin Clayton:

No, it was very … Being a publicly traded company, we had a current road show, which is 15-20 slides. Basically that and then any public information, a very small package. As you’ve heard, Warren keeps up with almost every publicly traded company out there and all the connections and contacts he has, it didn’t take him long to size our company up.

Robert Miles:

Why sell the business?

Kevin Clayton:

At that time in our industry, financing … Many of our competitors had really tapped into this Wall Street asset backed securitization process and some of those people’s loan performances were terrible. The industry was plagued with foreclosures so we looked out, talked to the board, and ultimately the board came to a consensus. $12.50 a share was the best thing for our current shareholders.

Robert Miles:

Which should be about a billion seven?

Kevin Clayton:

That’s correct. We went through the process of getting a fairness opinion and looking at what other alternatives were out there and ultimately the board believes and it was in the shareholders’ best interest. Certainly history now since then has shown that was a very wise decision because financing has literally dried up and changed forever for this industry.

Robert Miles:

Did it take you any time at all to realize that it would be a good thing to sell the business? Was there any hesitation on your part?

Kevin Clayton:

Absolutely hesitation. My father and I worked all of our lives building the company, and we knew we were owned by shareholders. We had to have their interest at heart. Of course, my father owned I guess between the family and my father, there’s roughly 47% of the company so we had a strong vested interest into make sure that if we were going to sell the company to get as much for it as possible. Later as you know, the company was ultimately … We had [inaudible 00:07:04] Blackstone, Cerberus. A group of people came in to pay more and ultimately decided that it wasn’t worth more than $12.50. There again was another check to see … Ultimately, the board made the right decision.

Robert Miles:

What has changed since you sold the business?

Kevin Clayton:

I would tell you that nothing has changed. Certainly, some things have and every one of those are absolutely wonderful positive changes. Of course, my life is much more fun now to not be begging for capital. We were needing over $1.2 billion in capital for mortgages each year. The cost of capital had continued to rise and rise. Not be doing that and not having the public company pressures has given us all more time to spend on the business. The best thing, of course, is that having capital in an industry has opened up many more opportunities for us.

I love to tell this story, and people don’t believe it, but we’ve made a lot of acquisitions over the last 24-36 months. Literally every time when I would talk to Warren he would say, Kevin, you and the team need to make that decision. Just rest assured you have plenty of capital to do so. It doesn’t get much better than that.

Robert Miles:

It’s been rumored that when Warren makes an acquisition, he doesn’t visit. Some people think that he doesn’t do his due diligence because he doesn’t visit. What’s your take on … Is it true that he did not visit you before he acquired you?

Kevin Clayton:

That’s exactly right. We sold the company. Of course, my father being the chairman, having built this company, sold the company without ever talking to Warren or certainly Warren ever visiting us, we were fortunate enough to have him come afterwards. What a great experience that was. He’s so intelligent that it doesn’t take him long to do due diligence. He literally stays current, I think, with most companies out there in most industries. With all the contacts he has, he sized up our industry very quickly.

Robert Miles:

How long did it take you to realize how much of a knowledge base Warren had about your particular industry?

Kevin Clayton:

Instantly. I’ve never been around anybody that … For instance, he sized up our industry problems that you could write a book about easily, he sized it all up in one sentence. He says, Kevin, it seems like the problem with your industry is resale. Every part of our problem at that time in the industry stems right back to that. We’re doing a lot of things to address that now.

Robert Miles:

Then on the time you sold the business, you had about $100 million in earnings and now about five times that?

Kevin Clayton:

That’s right. We had definitely a triple back in I think ’98 was our most profitable. We were 200 plus pre-tax and we looked to zero in on 500, north of 500 this year.

Robert Miles:

Wow. Congratulations.

Kevin Clayton:

Well thank you. Of course, Warren has invested billions of dollars in our company since he spent $1.7 billion. I take great pride in telling that story because here’s a company paid $1.7 billion for and within 12 months, he was investing north of $2-3 billion annually. Since the purchase, it’s north of $7 billion. The confidence and faith he has in our team and the faith he has in this industry is so obvious from that.

Robert Miles:

That money is being used for you to buy up other people’s mortgages?

Kevin Clayton:

That’s correct. The majority of that capital was used to buy … We’ve literally bought most manufactured housing loans out there at nice discounts. We have such a fine team of people that service those loans well. We’re great collectors of the mortgages and then we have the ability to bring the homes back in the event of a foreclosure. Order the materials from our plants at wholesale, recondition the home, and resell it, and have the refinancing to resell the home. In addition to that, we’ve got a great team that we purchase the Oakwood, Fleetwood Retail, Karsten Manufacturing recently.

Robert Miles:

I think in your dad’s book he talked about one of the best things about joining up with Warren was that he got you a front row seat at many of these auctions as well as a AAA credit rating.

Kevin Clayton:

Yeah, there’s not many companies that have a AAA credit rating, as you know. When you do talk to a potential seller and they know that there’s no financing contingency and AAA rated, the capital that we have, it absolutely opens up doors that we would’ve never had otherwise.

Robert Miles:

Your dad started the business in 1966, if I read right, and ran it for about 50 years. He actually started the business about one year after Warren took control of Berkshire Hathaway, which I believe was 1965. In those years, and I realize you haven’t been around for all those years, what do you think was the most pivotal moment in Clayton’s history that was a tipping point? Can you point to one?

Kevin Clayton:

There’s several. It was actually 1956. You said 50 years and that’s right. This year we celebrate our 50-year anniversary. Started selling automobiles in ’56 and shortly thereafter manufactured housing. There’s been so many lessons along the way. I think that’s what’s special about Warren looks for companies with great cultures. My father started the company. We did go bankrupt in the early 60s, and that taught us some valuable lessons. We never really had any debt to speak of after that.

The lenders just decided to get out of the industry, pay everybody back in full, but also told us to have our own finance company. I really give a lot of credit to that happening because we created our own finance company in 1972 because we saw lenders continue … It would come in to manufactured housing and lend money too easy, trying to buy market share, and then they would over collect loans and literally move people out of their homes when they shouldn’t have. That forced us to have this finance company, and that has served us very well. Most years after that, over half of our income generally is from financing.

Robert Miles:

Let’s talk a little bit more about the business. The economics of a site-built home versus a factory-built home, what’s the cost per square foot difference?

Kevin Clayton:

It depends on where we’re talking about geographically. I’d love to use the example right here in Omaha. I just left the Berkshire shareholder meeting over here where we’re setting up two manufactured housing units. One’s $89,000, one’s $79,000. By the way, we call one of them Charlie’s Crib and Warren’s Pad on the other one. We just sold Charlie’s Crib before we got it set up. That was a lovely couple that had been saving money. Their plan was to save money for another three years and build up to have a sizable down payment and purchase a home. They were planning on spending well north of $130 a square foot. They just bought this home that was equal in square footage size, and they really think it was aesthetically on par or better, and they paid $50 a square foot, and they’re gonna go ahead and buy it today. The home will literally be set up and installed within the matter of two or three weeks from now.

We’re also in the fast housing business, particularly in parts of the country where weather is an issue. Many developers are using factory-built housing now to do more homes, tie their cash up for less time, and now that the homes are on par with site-built housing aesthetically, and they’ve always been built very well. Most people don’t realize this, but since 1994 when we made the wind zone standard changes, there literally has not been one home found that has been severely hurt after all the hurricanes that have happened. That’s a message that we’ve got to do a better job as an industry getting out there.

We now have JD Powers in the industry measuring customer satisfaction. We’re doing a very good job with that. These are the things that are propelling factory-built housing to be a much larger player in the overall housing market. That couple is a great example. There still is a great shortage of affordable housing in America right now, and we hope to continue to get better to serving it.

Robert Miles:

What percentage of the overall market, Kevin, is manufactured in the factory versus site-built?

Kevin Clayton:

It’s around 10% today.

Robert Miles:

Factory built?

Kevin Clayton:

Factory built. We use the work terminology “factory built” which would include everything, mobile home, manufactured housing, and modular. We do all of the above, manufactured housing and modular units.

Robert Miles:

I was gonna ask you what you’ve done with the image. There’s many jokes about trailers and hillbillies. Is there anything that Clayton homes is doing in terms of the image?

Kevin Clayton:

As an industry, we’re ready to launch a national campaign to dispel those myths. As I mentioned, hurricanes, that’s not an issue anymore. Now every home has to be inspected by a licensed installer, an inspection process. The tie down systems and all that are very adequate as evidenced by the hurricane issues. JD Power, CSI, all those things now give us a great message to go public with. There’s plans for that underway now.

Robert Miles:

Where do you see Clayton Homes, say, 20 years from now?

Kevin Clayton:

It’s gonna be a lot of fun being a part of that. It’s exciting to see our product now. We build homes as large as 5,000-6,000 square feet. In downtown Detroit, I was in a home recently, a large colonial home there. We build multi-story homes, we build some multi-family units. The potential is enormous and with the capital that Warren provides, we should be able to do on par financing. I think we’ll excel site-built housing from a quality standpoint. Every one of our homes is inspected by federal inspection through HUD all throughout the building process. That’s not done with site-built housing. Particularly, material costs have gone up and land costs. It really makes us even much more compelling.

Robert Miles:

It seems to me that it’s not an industry where you have to worry about outsourcing where some other country might be able to manufacture homes cheaper and then ship them.

Kevin Clayton:

That’s very accurate. We’re very fortunate. Of course, Warren looks for companies that have that enduring competitive advantage. That’s part of our moat, and we intend to deepen and widen that part of our moat. We’ve shipped units overseas before, we continue to look at opportunities overseas, but it would be very difficult for someone to compete. People don’t realize in America with the availability of lumber and raw materials is terrific here compared to most places overseas.

Robert Miles:

Just as foreign competition is not likely to manufacture offshore and import, is Clayton homes not very likely to manufacture here and export for the same reason?

Kevin Clayton:

We have shipped some units, but more likely it would be us taking our expertise and lending it overseas and building over there. That’s a possibility, but such opportunity here domestically, I think that’s a ways off.

Robert Miles:

Warren likes to say that there’s two types of competition that he doesn’t …

Kevin Clayton:

Well, Warren likes to say that there’s two kinds of competition that he doesn’t like, foreign and domestic.

Robert Miles:

Right, and it seems like you’ve eliminated the foreign. What about your domestic competitors? How are they holding up?

Kevin Clayton:

We have some good competitors. I mean, everybody’s trying to carve out their niche, and Warren is very competitive. It’s just amazing, his personality, to be such a genius. He’s also the greatest leader I have ever worked for, the greatest people skills, but again, he paints such an image in each of our manager’s minds about this moat, this competitive moat, and our job is very simple and we share this. It’s so fun sharing some of the things that he passes along throughout our organization, and we challenge every one of our team members, every department. Who is your customer? Deepen and widen your moat to keep out the competition, whether it’s the next department over. How can you serve them better?

But some of our competitors do a good job, but our plans are to make that difficult for them.

But ultimately, it’s providing very affordable and the highest quality of affordable housing. If we do that and we get better every day, we should have a very bright future.

Robert Miles:

And you’re currently the leader in sales and in earnings in the industry?

Kevin Clayton:

That’s correct.

Robert Miles:

What percentage of the manufactured home market does Clayton own?

Kevin Clayton:

Of units shipped, we’re closing in on 25% of … shipped meaning built. We are the largest retailer of factory-built housing also through the 450 company owned stores. But the mom-and-pop operator out there, and there’s plenty of those, they will always be the dominant selling organization, and we rely on, again, almost 2,000 of those independent retailers to sell our product. They’re very, very competitive and do a great job for us.

Robert Miles:

I wanted to talk about your management style, philosophies, the culture at Clayton. How would you define your core philosophies or your core values at Clayton Homes?

Kevin Clayton:

Well, we have a leadership model in our company and it’s the inverted triangle. We call it the servant leadership model, and it’s become more popular recently. But we ask every manager to take that servant mentality which just clearly says that their job is to make sure every team member has every tool and resource on their team to be successful, and that’s each of our jobs. If we do that and make sure they have everything they need, then it takes a lot of a pressure off the manager. Their job is not to have every answer, but to team with everybody else in the company and find the right answer.

So that gets into this self-awareness and self-confidence and each of those leadership characteristics that helps create our culture. Our culture was created from Jim Clayton, day one. That’s the work ethic, results oriented, no matter where we are today, there’s a better way to do it tomorrow, so we’re challenging every process throughout the organization, and that’s what keeps it fun. That’s why my job will always be fun. I’m so excited. At this moment, I realize we’ve got a long ways to go, and that’s what keeps it so fun.

Robert Miles:

So, the culture from Jim Clayton to Kevin Clayton, has it changed?

Kevin Clayton:

My father created the company and took it to one level. He was able to literally be hands on with every process and know every person in the company intimately well. The company grew to a size where, and I was fortunate ’cause my leadership style really wants to encourage team members to make sure they have every tool, again, and resource they can to make good decisions and then to ask for support and help, and also won’t hesitate to jump in and help micromanage when the process needs it. But at the size the company grew to, I have had to absolutely rely on the team, and what a team we have.

Robert Miles:

How many employees, you call them team members?

Kevin Clayton:

Correct.

Robert Miles:

How many?

Kevin Clayton:

We’re 15,000 now.

Robert Miles:

Wow. Wow.

Kevin Clayton:

Yeah.

Robert Miles:

Now, in your father’s book, he talked about the difference between ego and confidence, and he also talked about you having a lot of confidence. Can you comment on your dad’s perception of those two personality traits?

Kevin Clayton:

Dad had created so many good analogies for us, one of which is this 90-10 rule, and all of us have these great core competencies, and we’re very comfortable making 90% of the decisions that come at us. But we ask our team members to realize, chances are they’re going to have some things that they have not had a lot of experience in, which is those 10 percenters, if you will. So, create an environment where your team members are comfortable coming and asking for help on those 10 percenters, and then all of us, no matter what position we’re in, including me, should be very comfortable asking for help on those decisions.

We always talk about always play for the name on the front of the jersey and not the back of the jersey. It’s this keeping the ego totally out of it, attack the process rather than the person. These are all these cultural things of what makes Clayton Homes so great today, and we work smart. We work hard, smart, and together. We’ve got acronyms. Our lives work only to the extent we’re willing to keep our agreements. I love that one that my father started, and then something that I kind of take from that to another level is that really there’s four major areas of all of our lives that we need to keep our agreements in, and our lives work only to the extent we’re willing to keep those agreements, but that’s work, health, spiritual, and family. We really promote that throughout the company.

We closed all of our locations on Sundays a year ago, and we did it for all four of those important areas of our lives, and often you’ll find team members that are overdosing in particularly that work quadrant, because literally, when you’re on one of our sales centers selling homes to families that never dreamed they would have a home of their own and they’re crying across the table, it’s easy to overdose at work. Our lives work best when we pay some attention to all those other areas.

Robert Miles:

I also thought it was pretty interesting on your headquarters and how that may be different than most headquarters?

Kevin Clayton:

Well, was very pleased to have the opportunity to build a new office. We did that in 1998, and we built it with no offices, so it’s a totally open atmosphere, and we always promoted this open book concept. It’s served us so well. I mean, the only offices that … there’s no offices, but there’s some private rooms for teaming rooms, but everybody, including me, we’re same sized desks.

So, the good news is we don’t have to move desks around anymore. We just move around as we grow different areas of the company. But that’s, again, a cultural thing that makes us a little bit different.

Robert Miles:

So, you have a cubicle just like everyone else?

Kevin Clayton:

Absolutely, yeah.

Robert Miles:

Your management style, how do you spend your time?

Kevin Clayton:

I spend it working on people, supporting the troops. I have an all-star management team that run each of those five businesses, and they’re dynamite. They’re the best in the industry in each of those areas, so I’m often amazed at how little they need me, and that tells me we’re doing a better job. But seeing where the industry’s going and making sure that we’re doing the very best job we can in each of those areas, that’s … We open communication frequently and often with that leadership team.

Robert Miles:

You’ve got five businesses in one. How do you balance the different, unique demands of each one of those businesses?

Kevin Clayton:

Well, my father started this discipline in our organization, and it has led probably to more of our success than any one other thing, and that is we always said we would never allow one part of the company to prop up another one, which would make ultimately that entity weak. So, we’re never going to give away financing to sell more homes at retail. We’re never going to make our [retail] store managers buy Clayton [Homes, CMH] products. See, those store managers can buy from lots of other manufacturers, and they do, and that keeps our plant managers, and if they’re not the best on value, cost quality, and style, then our stores and certainly those independents will buy from other people.

So having that discipline, which is really what led to a lot of the failures of the other companies in our industry, we’ll never compromise that, and I think that will continue to make us a stronger company. Make sure every one of those have to compete independently.

Robert Miles:

What about people and your selection of people, Kevin? It seems as though that’s got to be the key of your business as well as any other business.

Kevin Clayton:

Absolutely. We have great [retail] stores and great [factory building center] plants. What Clayton Homes really has is the very best people in the industry, and we just keep trying to raise that bar. Retention, our turn over is low as it’s ever been in the history of the company. We keep trying to drive that down further. Again, and great cultures attract great people and retain people. We try to put the great incentive programs in place where the performers make a lot of money, and they stay with us. So that’s the thing I’m most proud of, of course, is the people that we have.

Robert Miles:

Now I understand through my research that you’ve adopted some Japanese management philosophies, a word I’m not sure how to pronounce, kaizen? Kaizen?

Kevin Clayton:

Kaizen, yeah.

Robert Miles:

Kaizen. What the heck’s kaizen?

Kevin Clayton:

Well, Deming, statistical process control, these are things of course the Japanese learn very well, and many companies in the U.S., too, now deploy those. But I was fortunate enough to the University of Tennessee in the graduate school there, and I was so anxious to get back into work and try to put some of those in place.

Well, it took a long time, and not until I did one thing that really propelled it along, and that was I changed the pay program within our manufacturing plants. When I was in Waco, Texas, a great place to live. I’m not sure what I did to deserve to get shipped off there, but no, it was a great experience. We started up our first plant there in Texas, and it became obvious to me that most people, the management in the plant was incentivized on total profitability, and whereas the line worker who had all the information about how to make a better home and was really ultimately the best person there to … Then they were paid on how many units they shove out the door, which is how a lot of production people pay.

Well, we started including our team members and we pay our team members now 20 plus percent of the pre-tax profit at that plant. So, we get together monthly and talk about the good and the bad. The walls are covered with all the profit loss and the information that they need to know how to build a higher quality home, ’cause every scrap and waste comes right out of their pocket now. Every quality item defect, scrap waste, so they’re incentivized now for the same thing that management is, and that’s to build the best house possible.

No longer is, number one, it’s not important how many units you build, so that, we literally build wiring harnesses now so there’s not two inches of extra wire laying around, because 20 plus percent of that is the team members. It’s those kinds of things that really have propelled quality throughout the company.

Robert Miles:

Have the Japanese taught you anything else in terms of managing your business?

Kevin Clayton:

Well, this whole open book and sharing of information and measuring every process, step along the way, and improving it all the time. That’s the basics of what most of those philosophies come back to.

Robert Miles:

So, you’re not only team member centric, but you’re also customer centric. Can you explain that?

Kevin Clayton:

Well, we rely so much on repetitive business and reputation. Reputation, to my father and this company, was always number one. Warren Buffett, of course, takes it to a whole ‘nother level, and taking again some of what he continues … There’s not a lot of things that Warren is constantly communicating to us managers, but there are a couple. The moat and the competitiveness, but reputation. I honestly believe what he says is true. We could lose hundreds of millions of dollars tomorrow and that would be fine. Don’t lose a shred of reputation. Never contemplate any act, and we share this, have so much fun with our team members because it … Again, protect our reputation every day. Never even contemplate an act unless you’re totally comfortable with it appearing on the front page of the paper written by an informed reporter.

You’re heard all of these so many times, but it paints that image about how serious we are about taking care of every customer. And then we’ve always, we call every customer if they’re lived in the home six months and ask them, “Would you buy from us again?” So, we incentivize and measure every aspect of the business based on what the customer is telling us.

Robert Miles:

Is your management style, Kevin, much different than the management style you and your father had?

Kevin Clayton:

Not really, because we’re both very driven to do better and make it a better company every day. I think that the main things, again, are just the size of the organization. It requires a different skill set and to depend much more so on your successful people out there.

Robert Miles:

To your childhood, when you were growing up, what was your dream? Was your dream to run Clayton Homes?

Kevin Clayton:

No, it never was, and I’m glad you mentioned that, because I am forever grateful to my father for never insinuating at all that I want you to run this company. He had the intelligence to never do that. There’s no telling how it would have turned out, I’m afraid, if he would have kept hitting me with that, or maybe more importantly, kept telling people that that was important to him. We always knew that we wanted the best person to run Clayton Homes that we could find, and that left all my options open, and had a dad nice enough, too, to leave me in each position a long time to make sure I could make it and to get promoted and learn each of the areas.

Robert Miles:

But what was your boyhood dream?

Kevin Clayton:

Well, I like to fly airplanes, as you do.

Robert Miles:

Right.

Kevin Clayton:

So, there’s many times when my dad and I are flying around opening up a mobile home lot. At that time, he would take a catnap, ’cause he was working around the clock, and tell me to hold that heading and that altitude. So, I’ve always enjoyed flying, but beyond that, it doesn’t get any better than selling a home to somebody that never dreamed that they could have a home, in many cases. So, I was always very interested and wanted to stay in a business. Worked a couple of places, but not for very many years, and always came back.

Robert Miles:

Beside your father, who was one of your boyhood influences? Who did you really admire? Who were some of your heroes?

Kevin Clayton:

I would say my mother. Mother has a great sense of humor, values. She is a very hard-working person just like my father, and I’m very blessed. The two of them were an incredible influence on me and encouraged me to school. We worked after school every day, and they were both there for many of the sports activities as well along the way.

Kevin Clayton:

Anyone non-family related? Superman?

Robert Miles:

No, no. Nobody jumps out at me really. All along life I just tried to take advantage of every opportunity that came along.

Robert Miles:

And your first job at Clayton Homes, 75 cents an hour, what were you doing?

Kevin Clayton:

That would have been on one of the sales centers, cleaning the sales center, working on homes, installing homes. It was a lot of fun. It really was.

Robert Miles:

What was the worst job you’ve had at Clayton Homes?

Kevin Clayton:

Often, I had the opportunity to go in behind some managers where we had locations that were in tough markets. I know I got shipped off down to Georgia after we bought a distressed mobile home loan portfolio of loans that I was charged with cleaning up, and running multiple sales centers down in that area, traveling six days a week. Those were some tough times, but those were lessons that I wouldn’t trade for anything.

Robert Miles:

And the hardest thing you have to do now?

Kevin Clayton:

That’s a good question. There’s not a lot that I don’t really enjoy right now. Seeing a plant or a facility that’s not taking advantage of all the programs that we have to offer, those are painful to see, and I try to encourage those people along.

Robert Miles:

I thought you would say possibly firing somebody might be the hardest thing you have to do.

Kevin Clayton:

It always is. It always is. My father shared a lesson with me that we share throughout the organization that’s, again, a piece of that culture. We never let a team member go in our company in such a manner that they wouldn’t still recommend we’re a good place to work and that we’re a good place to buy a home from. What that makes us all do is it shouldn’t ever be a surprise to you if you’re not a fit with our company any longer, and we’re always going to do it in such a manner that we can part friends

Robert Miles:

In terms of succeeding your father, what kind of preparation did you put yourself through?

Kevin Clayton:

Again, Dad was smart enough to leave me in different roles in the company for a long time, and I’ve worked in the factory floor, ultimately ran a region of our manufactured housing retail locations, and then a plant, and got to run each of the different five business units before 1999, when I became the manager. So that was good preparation, because again, back to each one of our companies, if we’ve lost control or gave away one part of the company, it could benefit another, well. So it’s important for who leads this company in the future to have the knowledge of each of those organizations because each are important to each other, but they do have to stand on their own and compete.

The challenges of being the son of the founder, the son of the leader of the business, I think Don Graham at the Washington …

[About 00:40:04 time mark]

…Post, who succeeded his mother, said that most people didn’t think he was quite as smart as he really is, and he kind of liked that.

Robert Miles:

What are your thoughts or what do you wish more people understood about being the son of such a dynamic entrepreneur like your father?

Kevin Clayton:

There’s days where you could let that bother you that someone assumes that you were propelled into this position. That’s back to what I said. I was so fortunate that my father never told people that he wanted me to run it. People that have been around a long time understand that hopefully that I was able to work through the organization and earned each of the different positions. I wouldn’t want it any other way. You always wish that, but I would agree. I’d rather have it where people underestimate you. My father always said, and I believe it to be true, the most dangerous people are people that don’t know how much they don’t know. We really encourage a very humble style because that’s the dangerous person that thinks they have all the answers.

Robert Miles:

You’ve gone through several transitions from a family business to a publicly traded business, and now from a publicly traded business to being a subsidiary of a very large conglomerate. What are some of the advantages to being a subsidiary of a very large company?

Kevin Clayton:

To have a mentor and a boss, that it doesn’t get any better than the example that he sets from all aspects of life. It’s true that nobody believes this, but he literally says, “Don’t send me anything monthly except stuff you would produce normally.” We literally don’t package up anything. Ultimately, Berkshire Hathaway consolidates the numbers, but it’s the normal financial package we would’ve prepared anyway. People don’t believe it’s fun sharing. The common question is, “What’s it like working with Warren?” We talk. Fortunately, we’re still averaging about once every two weeks. We’re usually talking about an acquisition. Those are wonderful questions. He’s always there. He answers the phone, normally on the first ring or two. He always talks about that most people find him a lot more boring of a person because he really sits around like a professor and studies. To have a person like that you could bounce things off is wonderful. Not having to worry about capital and the public markets provides a lot of extra time to work on building a better home.

Robert Miles:

One CEO told me that he used to be publicly traded, Ralph Schey of Scott Fetzer. After he sold the business to Warren, he reported to me that there were 50 days a year that he now had to spend inside the business and no longer had to meet with analysts, no longer had to meet with bankers.

Kevin Clayton:

Without question, that’s true.

Robert Miles:

Can’t you quantify?

Kevin Clayton:

That is a good number. I’ve tried to quantify it, and it would certainly be around that number. You could add to that, even though you may not be spending any time on it at that moment, it’s certainly in your mind and a big part of your thinking process all the time. Warren is an absolutely the way it should be, very, very long-term horizon. You’re able to make investments that are going to yield rewards. Even if they don’t yield a reward for the first five years, it doesn’t matter. Next quarter never matters. Really, if you’re preparing for five years out and you’re going to compromise the next two years to do it, that’s a good decision.

Robert Miles:

Warren likes to say that he requires no meetings of you as a CEO. He requires no budgets. What is his standing order to you? What does he want you to do?

Kevin Clayton:

Everything you just said is exactly true.

Robert Miles:

No meetings?

Kevin Clayton:

No. Once a year there’s an optional invitation. I was fortunate enough to get invited to come and actually be around the board at a recent board meeting. That just even gelled my thinking. The culture of Warren and what’s he’s created, I think, will go on a long, long time after Warren as well. Everything’s optional, and there’s nothing mandated whatsoever.

Robert Miles:

You send financials monthly to headquarters.

Kevin Clayton:

Correct.

Robert Miles:

You call Warren whenever you would like to, but does he ever call you?

Kevin Clayton:

Occasionally. It’s something he’s heard or has an inquiry about. There’s never directing the business.

Robert Miles:

Warren doesn’t like to talk about synergy, but what have been some of the Warren Buffett effects or the Berkshire Hathaway effects of joining a large conglomerate?

Kevin Clayton:

People find it hard to believe that we’re not mandated to buy Johns Manville insulation for our homes, MiTek gang nails, Shaw carpet. The list goes on and on. We’re not whatsoever. Circling back to what I said earlier, not making one of our businesses prop up another one, it’s the same philosophy. If we’re mandated to start buying those materials, they could not be as competitive as we could get on our own. Really, management would lose some accountability if Warren is dictating these things down. I think he’s very, very wise in the way that he does things. The synergies that are there, of course, is that each of the managers, all things being equal, we would rather sell to a sister Berkshire company, and we look for those. One example that I just spent some time on recently, Home Services of America is the large brokerage-

Robert Miles:

Second largest home brokerage company in the United States.

Kevin Clayton:

…In the country. You can certainly paint a picture how five years from now these subdivisions that we’re building with beautiful factory-built housing could be part of their supply of housing ultimately and handling of the remarketing of some of those. There’s things like that that will certainly come to fruition.

Robert Miles:

Kevin, when I think of Clayton Homes, I think of home manufacturing, but Warren lists Clayton Homes as a financial subsidiary or a financial services. Why do you think you’re classified in that category in the annual report?

Kevin Clayton:

When Warren purchased us, I think financial services was north of 60% of our income. Today it’s 70%, total income, having purchased those portfolios. It certainly is a wonderful recurring income aspect. We deploy a lot of capital in financial services. That is the capital requirement. The rest of the businesses typically generate cash. We’re very fortunate to be in that part of the business, particularly because lending comes and goes in this industry and site-built housing.

Robert Miles:

On to succession. It seems like the Clayton Home model of how your dad selected you as the successor, and prepared you, and then gave the reins to you is a model that other companies should possibly consider. Your thoughts on Berkshire Hathaway and Warren’s succession plan, different than Clayton’s, but do you have any thoughts?

Kevin Clayton:

Total comfort with that because you’ve heard Warren say too that the person who is managing the companies of Berkshire Hathaway, their job will be to primarily stay out of their way and to keep letting them manage their businesses. That’s the message that Warren has shared with the board, and I have total confidence in them. I think there will be a great succession plan. Certainly, the people that I see Warren surrounding himself with are very, very capable people.

Robert Miles:

Berkshire post-Warren, will it look much different than what it looks like today?

Kevin Clayton:

I don’t think it does look any different. I think it’s an amazing machine that Warren has created that will outlive us all.

Robert Miles:

In analyzing some of the CEOs that make the Berkshire Hathaway team, it seems as though they’re going to look for somebody in their 40s, somebody who’s already running a very successful subsidiary, somebody already in the business, not bringing anyone in from the outside. It seems as though Kevin Clayton would be a candidate of three or four CEOs that I could think of that would fit that role. If the board selected you as a successor to Warren, what would you do?

Kevin Clayton:

That’s quite a pipe dream that you’ve painted there. I would jump for joy. Any way that you could be associated with Berkshire Hathaway would be an incredible honor. Again, just as I was growing up in my father’s business, I would want to make sure they chose the best person. That’s the most important thing beyond who it is.

Robert Miles:

How would you manage the other CEOs?

Kevin Clayton:

The same that Warren does, understanding that philosophy of there’s certain obviously … He says the right thing. It’s reputation, protect the company and the entities that we have, be as competitive as you possibly can be. Deepen and widen that moat every day, but not dictating down to managers how to accomplish the results that they need to because I genuinely believe they start losing accountability when you do that. It is real clear that if I mess this company up, if it gets messed up, it’s clearly my doing and not his.

Robert Miles:

In terms of corporate responsibility, corporate charity, and your own personal philanthropy, I’ve found that most successful, if not all successful business people that I’ve interviewed all have a mission outside of their own business. What’s the Clayton Home corporate charity?

Kevin Clayton:

Twofold. We try to be very active philanthropically in a lot of areas, but the two primary focuses that we have, one is we think in the future that factory-built housing will play a larger role working through non-profits, providing housing to particularly in urban infill and in housing of all types to people that couldn’t afford it otherwise, rebuilding some downtown areas, all that. We really have a great product for that, and we’re getting better at that. Ford Foundation right now is spending $10 million showing the non-profits how to use factory-built housing for that. We’re following their lead in that area. We’ve got a ways to go.

Second of all is education and working with schools. We’re watching Bill Gates and the lead that he’s taking there, he and Melinda and that [Gates] foundation. They work through a lot of organizations, one of those which, Daggett, does this model school conference and symposium.

We’re working with several high schools in our area and middle schools, sending them to that conference, getting them involved in that network. It’s really sharing best practices and trying to start teaching more of what’s relevant, having people come out of high school that are ready to go to work at Clayton Homes and many other jobs, and keep them in those towns where they were raised, make sure there’s good jobs there because ultimately all the data shows that to build a great community, they have great schools. If you’ve got great schools, the rest of the things usually come right behind that. We’re having a lot of fun being involved in that.

Robert Miles:

What about the Clayton Family Foundation?

Kevin Clayton:

Very similar, too. They support both to of the initiatives that I just mentioned. My father has control of that foundation, and it’s getting quite large. He’s tended to give money where we, Clayton Homes, have been successful and have team members. We hope some of these initiatives we’re working on we’ll be able to take out to the communities where we do business in other places.

Robert Miles:

Your father’s book, First a Dream, the proceeds go to the Tennessee Theatre restoration.

Kevin Clayton:

That’s right, great project. It’s really complete now, and they need to pay down a little more of the debt. Ever since the book was introduced, every dollar out of the purchase price, every dollar of it goes towards that and some other philanthropic initiatives. Particularly the new eight chapters that were added recently, they’re wonderful and go through the whole merger and the litigation, which Warren described as one of the ugliest litigation being around one of his mergers. That was a tough process that took almost a year.

Robert Miles:

What do you like to do for fun? I know you like to pilot airplanes. You flew yourself here today to the University of Nebraska at Omaha.

Kevin Clayton:

Yes, I like that. I take it very seriously, go through the simulator training several times a year.

Robert Miles:

Flight Safety, I hope?

Kevin Clayton:

Flight Safety, absolutely. What a great company that that is. Fortunately, we put enough hours on our planes annually that we don’t use NetJets, but we would if we weren’t putting the kind of hours we were trying to grow the business. I’m very blessed to have a new three-year-old in our life, our only child. She is a ton of fun. My wife and I like to snow ski occasionally. We have a lot of fun. I’m very blessed.

Robert Miles:

If you had anything to do over again, what would you do over?

Kevin Clayton:

No, to have a beautiful, wonderful wife, and a three-year-old, and work for Warren Buffett, it doesn’t get much better than that.

Robert Miles:

We’re on campus here, and wondered if you had any other advice to college students, young people in general.

Kevin Clayton:

Don’t sweat. A lot of people think coming out of school that, “How will I ever be at a level where I’m able to compete and have a job like many other people out there?” Don’t worry about it too much. We’re not near as smart as some of you make us out to be. I can assure you, it’s just taking advantage of every opportunity to gain experience. Gain all the experience you can along the way, and you will be shocked at the doors that will open and the opportunities out there.

Robert Miles:

Kevin, thanks for sharing your time, your business success, your insights into what it is like to manage a family business, a publicly traded company, and to sell to one of the world’s most famous and successful financiers, and now what it is like to manage a subsidiary within a large conglomerate. Thank you very much, Kevin, for your time.

Kevin Clayton:

Bob, thank you. Enjoyed it.

To learn more about Clayton Homes and all of its five businesses, and to order Jim Clayton’s book, First a Dream, visit clayton.net. I’m Bob Miles, and thank you for joining us.” ##

Additional Information with More MHProNews Analysis and Commentary in Brief

There are times MHProNews highlights a transcript in yellow and/or aqua to call attention to some remarks, for example, in a corporate earnings call transcript. For those who truly understand the big picture and the nuances of manufactured housing, there is so much in the above it might look like a colorful Tijuana taxi and thus the usefulness of such highlighting might be diminished as a result.

That said, consider the following broad topics. In no particular order of importance are the following themes.

- 1) Manufactured housing is misunderstood. Those misunderstandings include, but are not limited to, terminology. Is it a mobile home? Trailer house? Manufactured housing or manufactured home? At the time Kevin cut this video, an alternative term used that included manufactured homes, modular homes and other kinds of prefabricated home building was “factory-built housing.” Since then, Clayton has opted to use “off site built” housing. Where is the educational and informational marketing effort that might mirror the growth that the RV industry experienced with their GoRVing campaign? Clayton spoke about it above, but there is no evidence of anything akin to that, despite periodic talk about doing it.

- 2) Manufactured housing still has a lack of competitive lending. That has ripple effects that Pew and the Urban Institute, among others, has explored. The argument can be made that this is intentional, not accidental. The Williams/21st ‘tying’ letter is not, in that view, a one and done scheme. Pro-Berkshire author Bud Labitan in his book “Moats” specifically explores the financing moat that Clayton enjoys which means that others are harmed.

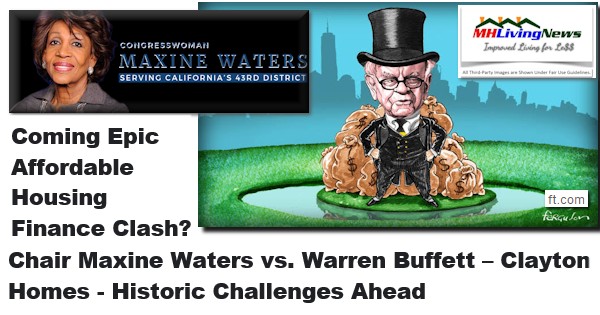

- 3) The Manufactured Housing Improvement Act (MHIA) of 2000 was enacted at about the same time as the Government Sponsored Enterprises (GSEs) of Fannie Mae and Freddie Mac pulled their support for manufactured housing around the turn of the century. Clayton mentions that manufactured home lenders left the industry, but he doesn’t directly connect the dots to the GSEs withdrawing the path to the secondary market for manufactured homes. The MHIA and its reforms and consumer guarantees also included what is commonly called “enhanced preemption” of local zoning. Why hasn’t Clayton-Berkshire-their lenders pressed through litigation the full and proper enforcement of the MHIA? After all, Buffett told Clayton there is ‘plenty of capital’ for Kevin to do what he wants. That implies that Kevin and ‘the team’ do not seriously want the MHIA’s enhanced preemption clause enforced.

- 4) The use of nonprofits in a philanthro-feudalism (a.k.a. philanthro-capitalism or philanthropic industrial complex) fashion in MHVille. One example is the indirect funding of MHAction by a Warren Buffett funded foundation through the Tides.

- 5) There are fewer manufactured home street retailers now then in 2000 or the start of 2009. Even Clayton Homes has fewer retail centers today, per their own annual report, than what Kevin said they had at the time of this video. Fewer retailers implies fewer manufactured homes sold.

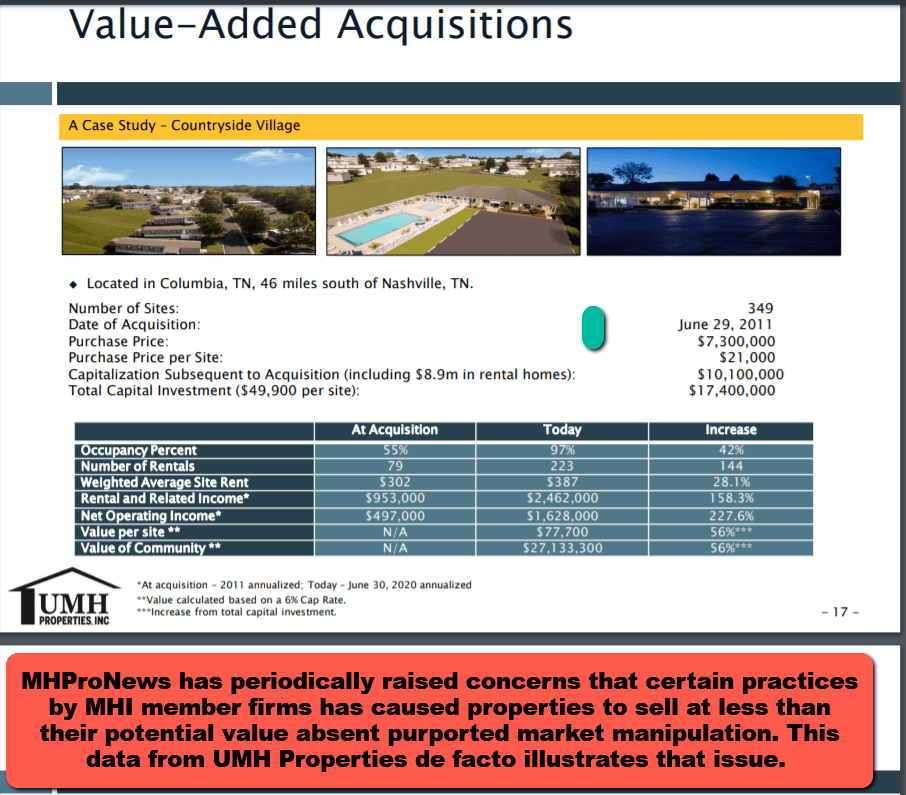

- 6) The loss of street retailers led to the inevitable impacts on thousands of manufactured home land-lease communities. Untold hundreds if not thousands of older ‘mobile home parks’ or newer manufactured home communities were sold for less than their intrinsic value. UMH Properties, via their periodic ‘case study’ reports provided to investors, illustrates the apparent harm caused to former “mom and pop” or independently owned manufactured home communities. A lack of capital and a lack of retailers filling vacant sites has ripple effects that benefit those with deeper pockets while harming those with less robust capital access.

Each of the above are Manufactured Housing Institute (MHI) members. Coincidence? Or is it a coincidence that virtually every firm that HBO’s viral hit on the industry misnamed Mobile Homes by Last Week Tonight with John Oliver have apparent ties to MHI? Additionally, numbers of those firms buy Clayton product. Those who retail homes now, because of the lack of street retailers today, may offer 21st Mortgage Corporation lending.

- 7) It is not necessarily a hit on the Biden Administration to note that despite the hoopla, first time homebuying is reportedly near or at all-time lows. As MHLivingNews detailed in the first linked report below, Democrats and Republican administrations alike have for years made housing promises that the elapse of time revealed were illusory. That noted, Berkshire has rare air level of access to movers and shakers in the federal government, Congress, or even the White House. Why hasn’t Berkhsire-Clayton either used that access to fix what is limiting manufactured housing? Or in the alternative, why hasn’t manufactured housing giant Clayton led the charge for funding legal action to get the industry’s rights under federal law enforced? Why didn’t MHI, under Tom Hodges or Tim Williams respective chairmanships – given that both men were Berkshire unit leaders in manufactured housing – to press MHI to use its millions to sue as needed to get the industry’s rights enforced?

The above is not exhaustive. But it is enough to make this point. Each of these could be a chapter in a digital book with hyperlinks to more research that explores each of these issues and how they overlap. All of these observations are fact-backed, evidence-based, and utilize common sense or ‘logic.’ Are manufactured housing professionals, related business owners, managers, investors, public officials, media and others to simply presume that highly seasoned and successful business and nonprofit leaders somehow missed what this report highlighted? Isn’t it more likely that MHI and their corporate backers want the status quo, because it leads to consolidation and acts as a moat to keep potential new competitors out of manufactured housing?

That was an observation made by faithful MHI member Andy Gedo in his public ‘debate’ with this writer for MHProNews.

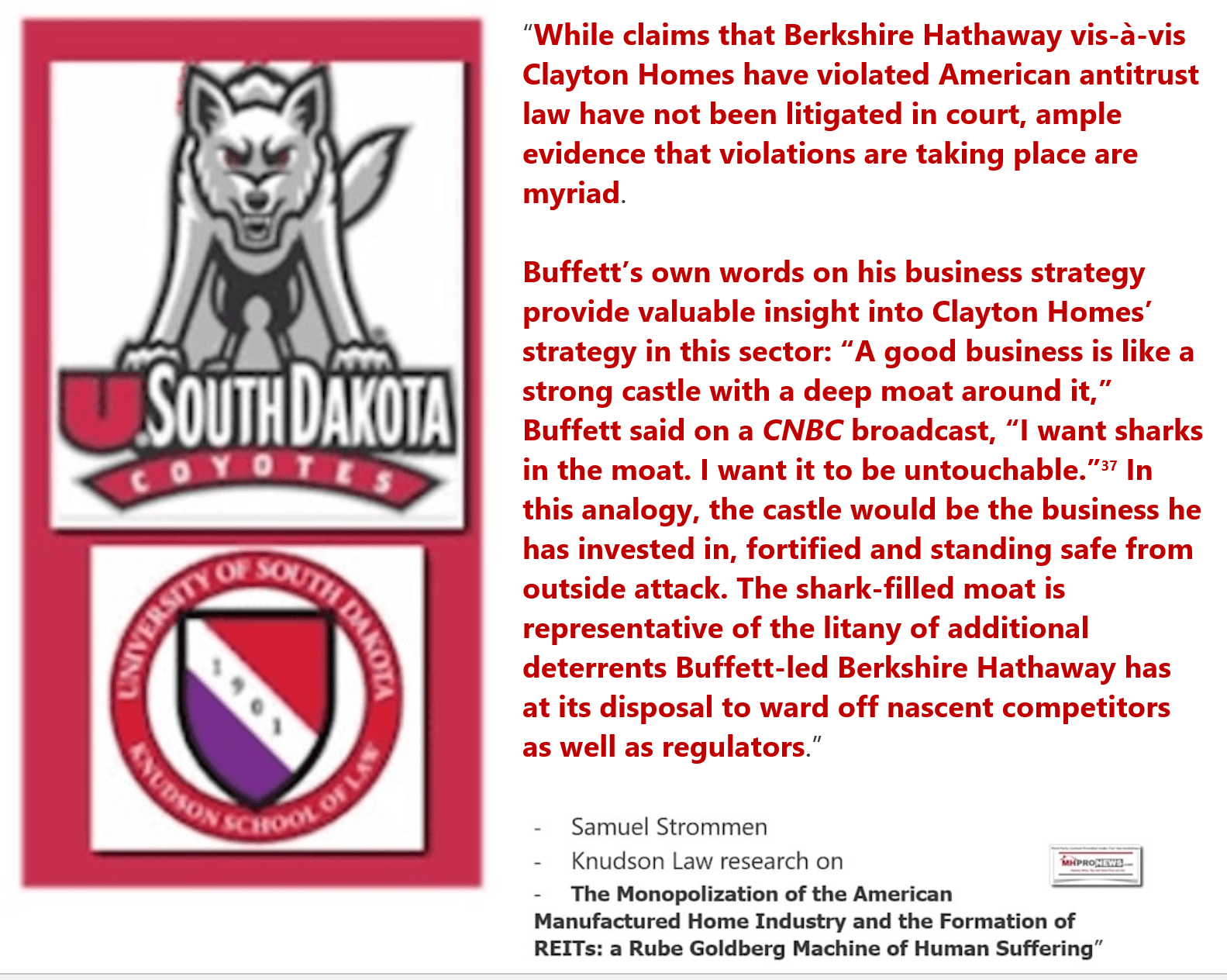

Outsider looking in and legal researcher Samuel “Sam” Strommen with Knudson Law bluntly observed that MHI appears to be part of a market manipulation scheme being executed by Clayton in conjunction with apparent allies Skyline Champion and Cavco Industries.

Researcher Donna Feir, Ph.D., after citing the Seattle Times report on troubling practices in Clayton Homes affiliated lending said that the issue begs more research.

House Democratic lawmakers cited below referred these vexing issues to federal officials. What happened to those referrals?

Democratic lawmakers cited below asked then Bush-era HUD Secretary Mel Martinez to enforce the MHIA’s enhanced preemption provision. MHI claims to want the MHIA enforced. But if so, why the lack of legal action to enforce the matter? The Manufactured Housing Association for Regulatory Reform (MHARR), which represents independent producers of HUD Code manufactured homes that authentically do want to grow the industry, has highlighted these issues on their own platform and in interviews with MHProNews.

Silver Lining?

MHProNews has noted that manufactured housing has become a target rich environment for legal action.

The recent arrest of accused mega-scamster Sam Bankman-Fried (SBF) and his associated FTX followed on the heels of the felony convictions of two Theranos corporate leaders.

Restated, it should not be thought that the status quo in MHVille will always be like it is today.

Massive Investment Opportunities for “White Hat” Investors

A case can be made that visionary investors with chutzpah, sufficient capital, who are willing to employ legal, marketing, sales, and construction expertise as needed could quickly ramp up and surpass some of the staid companies that currently dominate MHI. Perhaps some outside investors with guts and vision who want to make a healthy and honest profit providing millions of affordable housing seekers with an affordable home could team up with existing independent(s). They could create a post-production trade group. They could deploy legal efforts to enforce the MHIA’s enhanced preemption or get other federal laws such as the Duty to Serve (DTS) properly enforced. They could use attorneys to thwart the looming DOE energy rule. To illustrate the potential for white hat investors, the modular builder’s announced plan ought to be of interest. The point or the report below isn’t that investors should put their money into modulars. Rather, the point is if a modular builder crafted a business plan to open dozens of factories in a few years, where is the manufactured housing equivalent of that bold vision?

Some of this has not yet occurred, but that doesn’t mean that it won’t. Nature abhors a vacuum. The lure of tens to hundreds of billions of dollars in market share possible in providing affordable housing to Americans could prove to be enough to attract the money and mentality needed to transform the now underperforming industry into a roaring giant that could surpass conventional housing.

It should be noted that among the most accessed articles on MHProNews and MHLivingNews are reports that explore the legal issues raised herein. For well over a year the article linked below was the runaway most read on either MHProNews and MHLivingNews.

Other related reports include, but are not limited to, those that follow, or which were previously linked above.

As a closing note, an observation should be made the Berkshire owned dozens of local and regional newspapers. Among those was the Omaha World Hearld, see the photo at the top, was one of those newspapers. If Buffett and Clayton wanted to create an educational campaign, one article a week in each of those publications could have in a year generated serious interest in the value of modern manufactured housing. That didn’t occur. It is one more indirect piece of evidence that Gates was correct. Buffett has found weaknesses in markets – including manufactured housing. As Gates mused, Buffett and his henchmen apparently exploit those weaknesses in ways that are not value added. ##

![DidntWantToMeetWarren[Buffett]BecauseGuyBuysSellsFoundImperfectMarketNotValueAddSocietyZeroSumGameParasiticBillGatesPhotoMicrosoftLogoGatesFoundationLogoQuoteQuotableQuoteMHproNews](http://www.manufacturedhomepronews.com/wp-content/uploads/2020/07/DidntWantToMeetWarrenBuffettBecauseGuyBuysSellsFoundImperfectMarketNotValueAddSocietyZeroSumGameParasiticBillGatesPhotoMicrosoftLogoGatesFoundationLogoQuoteQuotableQuoteMHproNews.jpg)

need to wait years for legislation that in the past has often led to little or no discernable benefit. https://www.wnd.com/2021/05/solution-big-tech-oligarchs/

Again, our thanks to free email subscribers, all readers like you, our tipsters/sources, sponsors and God for making and keeping us the runaway number one source for authentic “News through the lens of manufactured homes and factory-built housing” © where “We Provide, You Decide.” © ## (Affordable housing, manufactured homes, reports, fact-checks, analysis, and commentary. Third-party images or content are provided under fair use guidelines for media.) (See Related Reports, further below. Text/image boxes often are hot-linked to other reports that can be access by clicking on them.)

By L.A. “Tony” Kovach – for MHProNews.com.

Tony earned a journalism scholarship and earned numerous awards in history and in manufactured housing.

For example, he earned the prestigious Lottinville Award in history from the University of Oklahoma, where he studied history and business management. He’s a managing member and co-founder of LifeStyle Factory Homes, LLC, the parent company to MHProNews, and MHLivingNews.com.

This article reflects the LLC’s and/or the writer’s position, and may or may not reflect the views of sponsors or supporters.

Connect on LinkedIn: http://www.linkedin.com/in/latonykovach

Related References:

The text/image boxes below are linked to other reports, which can be accessed by clicking on them.